Dollar shrugs off worse than expected Q1 GDP data and recovers against European majors in early US session. But momentum is so far weak except versus Swiss Franc, which happens to be the worst performer for the day. Australian Dollar and other commodity currencies turned into consolidation, digesting this week’s losses. Meanwhile, Euro and Sterling are losing much momentum for now, and turned mixed. Yen is also engaging in range trading, awaiting tomorrow’s first BoJ announcement by new governor Kazuo Ueda.

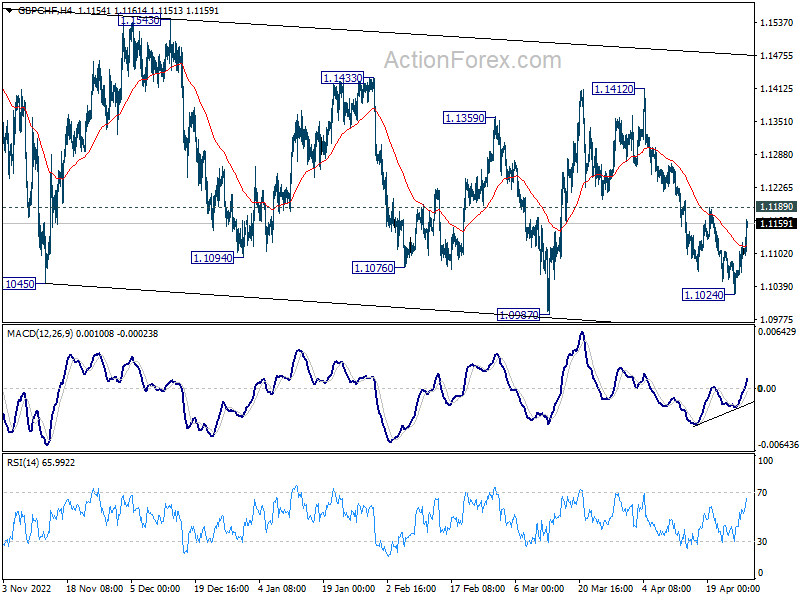

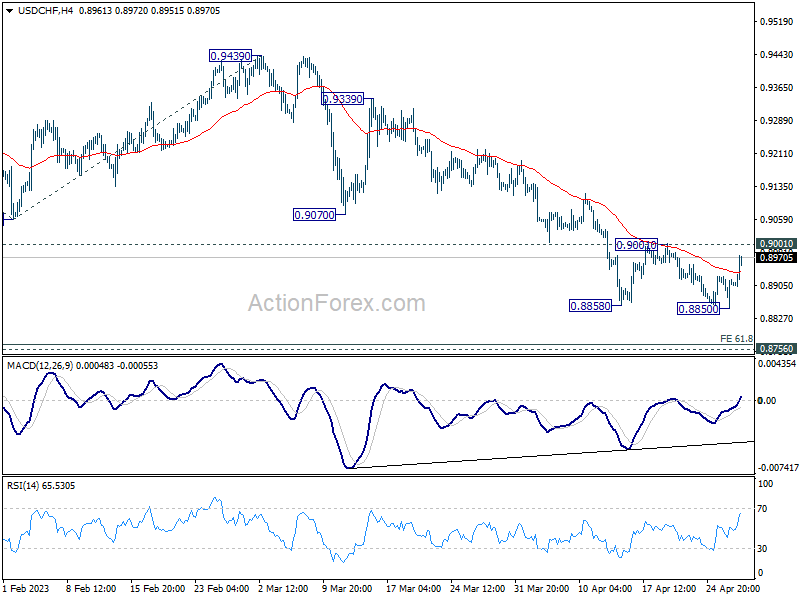

Technically, EUR/CHF’s break of 0.9846 resistance argues that near term pull back form 0.9995 has completed at 0.9774 already. Stronger rally is now in favor back towards 0.9995. One focus is now on USD/CHF, as firm break of 0.9001 should confirm short term bottoming, and bring stronger rebound. Another focus is 1.1189 resistance in GBP/CHF. Firm break there will indicate that fall from 1.1412 has completed at 1.1412. The sideway pattern from 1.1574 (Oct high) should have then started another rising leg.

In Europe, at the time of writing, FTSE is up 0.04%. DAX is up 0.28%. CAC is up 0.45%. Germany 10-year yield is up 0.0288 at 2.430. Earlier in Asia, Nikkei rose 0.15%. Hong Kong HSI rose 0.42%. China Shanghai SSE rose 0.67%. Singapore Strait Times dropped -0.36%. Japan 10-year JGB yield dropped -0.0027 to 0.460.

US GDP grew only 1.1% annualized in Q1, well below expectations

US GDP growth for Q1 2023 came in at a mere 1.1% annualized, significantly below the expected 2.0%.

The increase in real GDP can be attributed to rises in consumer spending, exports, federal government spending, state and local government spending, and nonresidential fixed investment.

However, these increases were partially offset by declines in private inventory investment and residential fixed investment. Meanwhile, imports, which are subtracted when calculating GDP, also increased.

Price index for gross domestic purchases rose by 3.8% in Q1, compared to the 3.6% increase recorded in Q4. Personal Consumption Expenditures price index saw a 4.2% increase, up from the previous quarter’s 3.7% increase. Excluding food and energy prices, PCE price index climbed by 4.9%, compared to 4.4% increase in the previous quarter.

US initial jobless claims down -16k to 230k

US initial jobless claims dropped -16k to 230k in the week ending April 22, better than expectation of 245k. Four-week moving average of initial claims dropped -4k to 236k.

Continuing claims dropped -3k to 1858k in the wee ending April 15. Four-week moving average of continuing claims rose 10k to 1837k, highest since December 18, 2021.

Eurozone economic sentiment up slightly to 99.3, third month of sideways movement

Eurozone Economic Sentiment Indicator ticked up from 99.2 to 99.3 in April, below expectation of 99.9. This is the third month of a general sideways movement of the indicator. Industry confidence dropped from -0.5 to -2.6. Services confidence rose from 9.6 to 10.5. Consumer confidence rose from -19.1 to -17.5. Retail trade confidence rose from -1.5 to -1.0. Construction confidence was unchanged at 1.0. Employment Expectation Indicator dropped from 108.9 to 107.4. Economic Uncertainty Indicator dropped from 22.4 to 22.2.

EU ESI was unchanged at 97.3. Employment Expectation Indicator dropped from 107.5 to 106.1. Economic Uncertainty Indicator dropped from 22.1 to 21.8. Amongst the largest EU economies, the ESI improved in Spain (+3.7) and, to a lesser extent, in Poland (+1.1) and Germany (+0.8). While sentiment edged up also in Italy (+0.3), it deteriorated in the Netherlands (-1.6) and, particularly, in France (-4.2).

NZ ANZ business confidence dropped slightly, inflation expectation lowest since Mar 2022

New Zealand ANZ Business Confidence index decrease slightly in April, dipping from -43.4 to -43.8. On the other hand, Own Activity Outlook improved from -8.5 to -7.6. A closer look at the details reveals that export intentions jumped from -8.9 to -1.5, while investment intentions remained unchanged at -6.8. Employment intentions rose from -4.6 to -2.4, and pricing intentions fell from 56.8 to 53.7. Cost expectations dropped from 86.4 to 84.2, and profit expectations declined from -33.9 to -37.7.

Inflation expectations decreased from 5.82 to 5.70, reaching the lowest level since March 2022. ANZ observed that the overall decline in inflation signals is consistent with RBNZ gradually gaining traction. However, the situation is far from resolved, as the proportion of firms experiencing high costs and intending to raise prices remains “problematically high”.

ANZ added: “The RBNZ will be encouraged to see the ongoing fall in the inflation indicators in the survey. While there’s still a way to go, inflation is set to continue easing over the year ahead, as they and we are forecasting.

“It’s important to note that the data does not represent a ‘surprise’ for the RBNZ; rather, it’s what they will be expecting to see if their forecasts are to come to fruition, with the OCR able to top out shortly.

“There are risks on both sides: inflation could get “stuck” north of the target band, or global markets could deliver a side-swipe, for example. But the overall message from this month’s survey is “on track.”

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8869; (P) 0.8897; (R1) 0.8943; More…

Intraday bias in USD/CHF remains neutral for the moment. On the upside, decisive break of 0.9001 resistance should confirm short term bottoming at 0.8850. Intraday bias will be back on the upside 55 D EMA (now at 0.9120). Sustained break there will be a strong sign of bullish reversal. On the downside, break of 0.8850 will resume larger fall from 1.0146, to 61.8% projection of 1.0146 to 0.9058 from 0.9439 at 0.8767, which is close to 0.8756 long term support. Strong support is expected there to bring rebound, at least on first attempt.

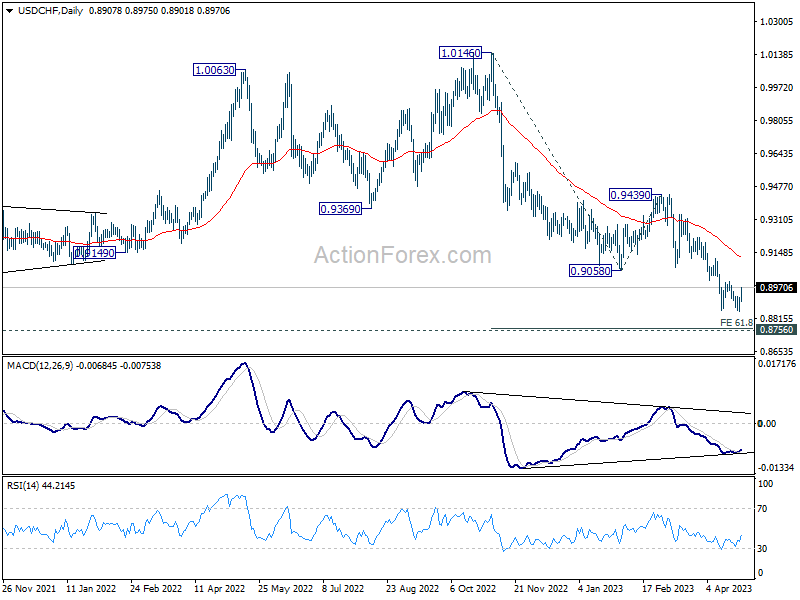

In the bigger picture, fall from 1.1046 (2022 high) is in progress for 0.8756 support (2021 low). But overall, this fall is still seen as a leg in the long term range pattern from 1.0342 (2016 high). So, downside should be contained by 0.8756 to bring reversal. Sustained break of 0.9058 support turned resistance will be the first sign of medium term bottoming. However, decisive break of 0.8756 will carry larger bearish implications.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:00 | NZD | ANZ Business Confidence Apr | -43.8 | -43.4 | ||

| 01:30 | AUD | Import Price Index Q/Q Q1 | -4.20% | 0.60% | 1.80% | |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Apr | 99.3 | 99.9 | 99.3 | 99.2 |

| 09:00 | EUR | Eurozone Services Sentiment Apr | 10.5 | 9.5 | 9.4 | 9.6 |

| 09:00 | EUR | Eurozone Industrial Confidence Apr | -2.6 | 0.2 | -0.2 | -0.5 |

| 09:00 | EUR | Eurozone Consumer Confidence Apr F | -17.5 | -17.5 | -19.1 | |

| 12:30 | USD | Initial Jobless Claims (Apr 21) | 230K | 245K | 245K | 246K |

| 12:30 | USD | GDP Annualized Q1 P | 1.10% | 2.00% | 2.60% | |

| 12:30 | USD | GDP Price Index Q1 P | 4.00% | 3.70% | 3.90% | |

| 14:00 | USD | Pending Home Sales M/M Mar | 1.00% | 0.80% | ||

| 14:30 | USD | Natural Gas Storage | 76B | 75B |

{kind=link}