Dollar weakened broadly during Asian session, as relatively upbeat sentiment in stock markets took hold. Despite Japan’s Nikkei being down after holidays, stocks in Hong Kong and China are both making gains. Australian and New Zealand dollars emerged as the stronger performers for now, followed by Euro. Meanwhile, Canadian Dollar lagged once again, digesting some of last week’s gains. British Pound is mixed, with traders awaiting BoE rate hike and guidance later in the week.

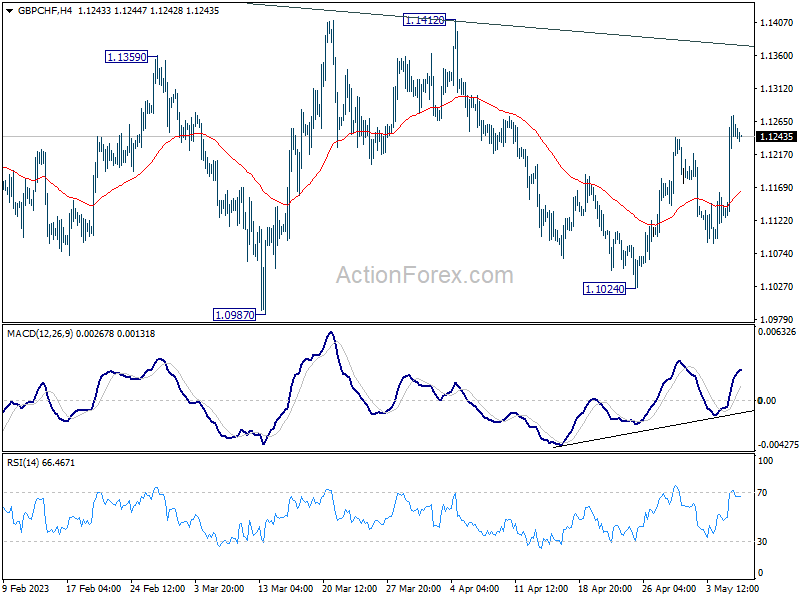

Technically, GBP/CHF made progress last week by extending its rebound from 1.1024. It remains uncertain whether this rebound is merely a part of a medium-term corrective pattern from 2022’s high of 1.1574. However, as long as the 55 4H EMA now at 1.1166) holds, further gains towards 1.1412 resistance level are likely. Decisive break of 1.1412 in GBP/CHF may require some assistance from either break of 0.9878 resistance in EUR/CHF or downside acceleration in EUR/GBP towards 0.8545 support.

In Asia, at the time o writing, Nikkei is down -0.66%. Hong Kong HSI is up 0.75%. China Shanghai SSE is up 1.56%. Singapore Strait Times is down -0.15%. Japan 10-year JGB yield is down -0.0052 at 0.418.

Japan’s PMI services reaches record high in April, record optimism too

Japan PMI Services rose to 55.4 in April, up from 55.0 in March, marking the eighth consecutive month in growth territory. This represents the highest reading since records began in 2007, surpassing the previous record set in 2013. S&P Global also noted that year-ahead business expectations reached an all-time high, while prices charged increased at the steepest pace in nine years. Meanwhile, the PMI Composite remained unchanged at 52.9, as stronger services growth offset a sharper reduction in manufacturing production.

Tim Moore, Economics Director at S&P Global Market Intelligence attributed the record rise in service sector output to a rebound in demand for face-to-face consumer services, recovery in international tourist arrivals, and improvement in new business from abroad.

Moore also emphasized the high level of business confidence, with around four times as many service providers expecting an increase in activity as those forecasting a decline. This optimism marked the highest level in more than 15 years of data collection.

Furthermore, service providers increasingly passed on higher business expenses to customers to alleviate pressure on margins from rising wages and transportation costs. This resulted in the steepest increase in service sector output charges since the sales tax hike in April 2014.

BoJ minutes: Few members saw positive signs towards price target

Minutes of BoJ’s meeting on March 9 and 10 show a continued commitment to monetary easing, with the aim of achieving price stability in a sustainable and stable manner, accompanied by wage increases. Nevertheless, a few members noted emerging “positive signs” toward reaching the price stability target, indicating a changing price environment.

With respect to yield curve control, some members emphasized the need to examine the effects of various implemented measures aimed at improving market functioning. They acknowledged that JGB yield curve appeared smoother than before. One member explained that if observed CPI inflation declined and market projections of interest rates calmed down, distortions in the yield curve would likely be corrected.

In terms of the 2% price stability target, several members underscored the importance of maintaining its commitment. One member added that the central bank should anchor inflation expectations to 2% by committing to achieve the target.

Meanwhile, another member expressed concern that discussing the target might lead to “unnecessary speculation” on monetary policy conduct, especially given the growing possibility of achieving the price stability target. This member also argued against revising the joint statement of the government and BoJ.

Australia NAB business confidence rose to 9, conditions down to 14

Australia NAB Business Confidence index rose from -1 to 0 in April, while Business Conditions slipped from 16 to 14. A closer look at the details reveals that trading conditions declined from 24 to 20, profitability conditions dropped from 13 to 11, and employment conditions edged up from 10 to 11.

Price and cost growth indicators were mixed, with labor cost growth holding steady at 1.9% in quarterly equivalent terms, and purchase cost growth increasing to 2.3% (up from 1.9% in March). However, overall price growth was 1.1% (down from 1.3%), and inflation in the retail sector declined to 1.4% (down from 1.7%).

NAB Chief Economist Alan Oster pointed out that business conditions, although lower, remained well above their long-run average. Confidence, although still below average, has stabilized around 0 index points in recent months. Furthermore, Oster observed some easing in price measures this month, even as cost pressures remained high. This trend may signal a gradual easing of inflation in Q2’s early stages, though inflation remains elevated.

BoE to tighten again amid high inflation, US CPI could move markets

BoE is widely anticipated to continue tightening this week, as recent data revealed that CPI remained in double-digit territory at 10.1% in March, despite slowing from February’s 10.4%. This figure is significantly higher than BoE’s own forecast of 9.2%. A majority of market participants expect the rate to peak at 4.50% following this week’s decision. However, most acknowledge that risks to BoE rates are now tilted to the upside. The new economics projections should provide insight into BoE’s view on inflation and hints on the rate path.

As is customary with all BoE rate decisions, voting will be a focal point. Dovish members, including Silvana Tenreyro and Swati Dhingra, are unlikely to change their stance given their recent comments. As a result, the decision is likely to be a 7-2 vote. Any shift in the seven hawkish members would be bearish for the Pound.

In terms of data releases, US CPI will likely be the most significant market mover this week. Other noteworthy releases include US PPI and University of Michigan consumer sentiment, Eurozone Sentix investor confidence, UK GDP, Australia NAB business confidence, and New Zealand BusinessNZ manufacturing.

Here are some highlights for the week:

- Monday: BoJ Minutes; Australia building permits, NAB business confidence; Germany industrial production; Eurozone Sentix investor confidence.

- Tuesday: Japan average cash earnings, household spending; Australia Westpac consumer sentiment, retail sales; China trade balance; France trade balance; US NFIB small business index.

- Wednesday: Japan leading indicators; Germany CPI final; Italian industrial production; Canada building permits; US CPI.

- Thursday: BoJ summary of opinions, Japan bank lending, current account; China CPI, PPI; BoE rate decision; US PPI, jobless claims.

- Friday: New Zealand BusinessNZ Manufacturing index, inflation expectations; Japan M2; UK GDP, production, trade balance; US import prices, U of Michigan consumer sentiment.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6710; (P) 0.6733; (R1) 0.6776; More…

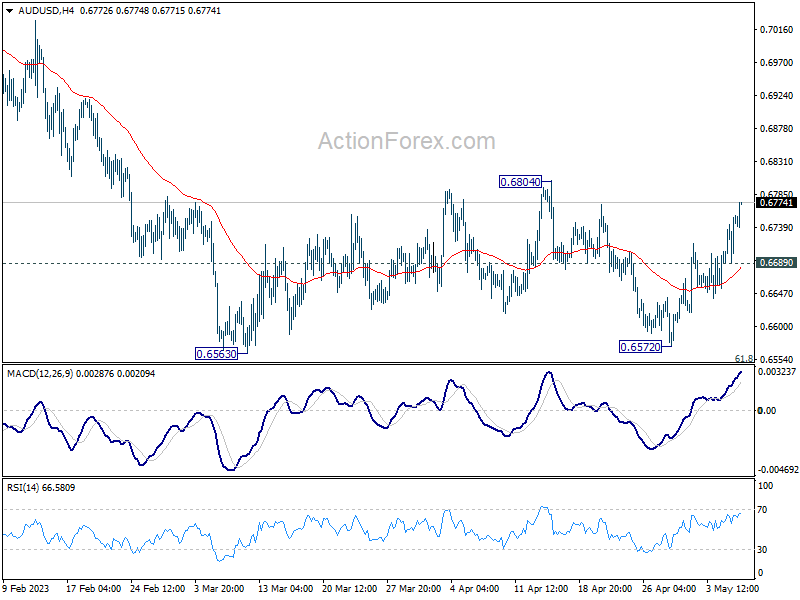

AUD/USD’s rebound from 0.6572 extends higher today, but stays below 0.6804 resistance. Intraday bias remains neutral at this point. Near term outlook also stays bearish as long as 0.6804 resistance holds, and down trend resumption through 0.6563 low is in favor at a later stage. Below 0.6689 minor support will bring retest of 0.6563 low. Nevertheless, sustained break of 0.6804 should indicate completion of whole fall from 0.7156, and turn near term outlook bullish for retesting this high instead.

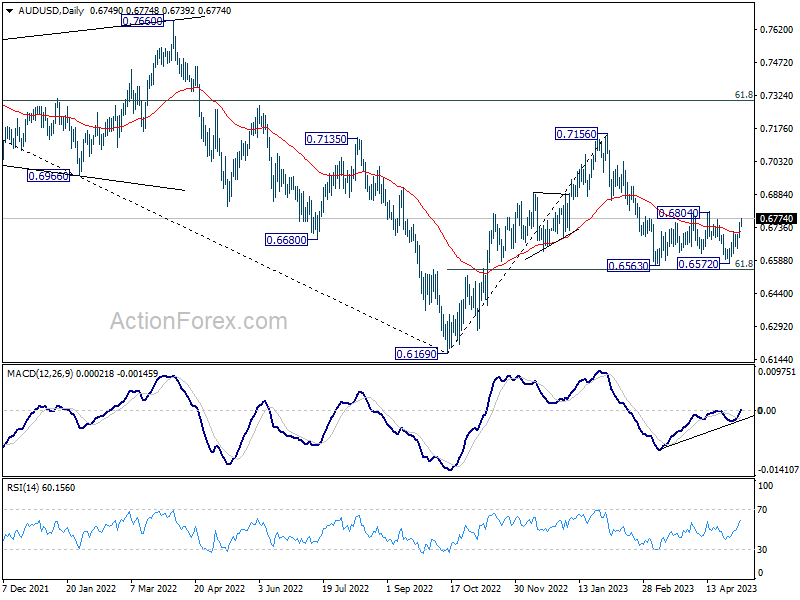

In the bigger picture, as long as 61.8% retracement of 0.6169 to 0.7156 at 0.6546 holds, the decline from 0.7156 is seen as a correction to rally from 0.6169 (2022 low) only. Another rise should still be seen through 0.7156 at a later stage. However, sustained break of 0.6546 will raise the chance of long term down trend resumption through 0.6169 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Meeting Minutes | ||||

| 01:30 | AUD | NAB Business Conditions Apr | 14 | 16 | ||

| 01:30 | AUD | NAB Business Confidence Apr | 0 | -1 | ||

| 01:30 | AUD | Building Permits M/M Mar | -0.10% | 3.00% | 4.00% | |

| 06:00 | EUR | Germany Industrial Production M/M Mar | -1.60% | 2.00% | ||

| 08:30 | EUR | Eurozone Sentix Investor Confidence May | -7.9 | -8.7 | ||

| 14:00 | USD | Wholesale Inventories Mar F | 0.10% | 0.10% |

{kind=link}