Market sentiment received a significant boost following upbeat news about US debt ceiling negotiations, and yet, Dollar remains resilient, showcasing an impressive strength. US President Joe Biden, following a meeting with Republican House Speaker Kevin McCarthy, presented an air of optimism as discussions continue. “Now we have a structure to find a way to come to a conclusion,” said McCarthy, adding “I think at the end of the day we do not have a debt default. I think we finally got the president to agree to negotiate.” Biden shared this confidence, stating, “I’m confident that we’ll get the agreement on the budget, that America will not default.”

Stocks in the US closed the day in a broad rally, with NASDAQ’s performance standing out as the index managed to close above 38.2% retracement of 16212.22 to 10088.82 at 12436.48. This significant bullish development forecasts further rallies as long the 12209.57 support level holds. The index should now aims for 13181.08 cluster resistance, 50% retracement at 13157.41. The burning question is whether Dollar could keep pace with the risk-on trend reflected in the stock market, or revert back to an inverse relationship.

Shifting focus back to the currency markets, Yen retains its position as the week’s weakest performer, dragged down by ongoing rallies in US and European benchmark yields. In addition, strong Nikkei index performance seems to amplify Yen’s inverse movement. Swiss Franc and Euro are also trailing in performance. Meanwhile, Kiwi and Loonie are faring well, but Aussie is being hampered by disappointing job data. Dollar, on the other hand, is extending its gains against Euro, Swiss Franc, and Yen, while remaining within range against Aussie, Loonie, and Sterling.

In Asia, Nikkei rose 1.60%. Japan 10-year JGB yield rose 0.0207 to 0.390. At the time of writing, Hong Kong HSI is up 0.41%. China Shanghai SSE is up 0.40%. Singapore Strait Times is up 0.40%. Overnight, DOW rose 1.24%. S&P 500 rose 1.19%. NASDAQ rose 1.28%. 10-year yield rose 0.032 to 3.581.

Australia employment down -4.3k in Apr, unemployment rate up to 3.7%

Australia employment contracted -4.3k in April, much worse than expectation of 25k growth. Full time job decreased -27.1k while part-time jobs rose 22.8k. Unemployment rate rose from 3.5% to 3.7%, above expectation of being unchanged at 3.5%. Participation rate dropped -0.1% to 66.7%. Employment-to-population ratio fell -0.2% to 64.2%. Monthly hours worked rose 2.6% mom or 49m hours.

Bjorn Jarvis, ABS head of labour statistics, said: “The small fall in employment followed an average monthly increase of around 39,000 people during the first quarter of this year.” Meanwhile, both employment-to-population ratio and participation rate “were still well above pre-COVID-19 pandemic levels and close to their historical highs in 2022”.

Japan’s exports grow at slowest pace since Feb 2021 despite setting record high for Apr

Japan’s exports grew by a modest 2.6% yoy to JPY 8288B in April. Although this represented the lowest growth in exports since February 2021, it still marked the largest export figure for April on record.

A closer examination of the data reveals a shift in trading dynamics. Exports to China fell by -2.9% yoy, marking the fifth consecutive month of decline. The decrease was driven by downturns in shipments of cars, car parts, and steel. Similarly, exports to Asia overall declined by -6.6% yoy, continuing a contraction trend for the fourth month in a row.

However, things looked rosier elsewhere. Exports to the US and EU showed robust growth, rising by 10.5% yoy and 11.7% yoy respectively. This uptick was led by a rebound in exports of cars and car parts, which have seen easing supply constraints.

Contrasting with export trends, imports fell by -2.3% yoy to JPY 8721B, the first annual decline witnessed in 27 months. This decrease was largely attributed to a slump in imports of crude oil and liquefied natural gas. Consequently, Japan recorded a trade deficit of JPY -432B for the 21st month running.

In seasonally adjusted term, the situation presents a slightly different picture. Exports rose by 2.5% mom to JPY 8259B, while imports inched up by 0.1% mom to JPY 9276B. In light of this, trade deficit narrowed to JPY -1017B.

Looking ahead

Canada new housing price index will be released in European session. US will release jobless claims, Philly Fed survey and existing home sales.

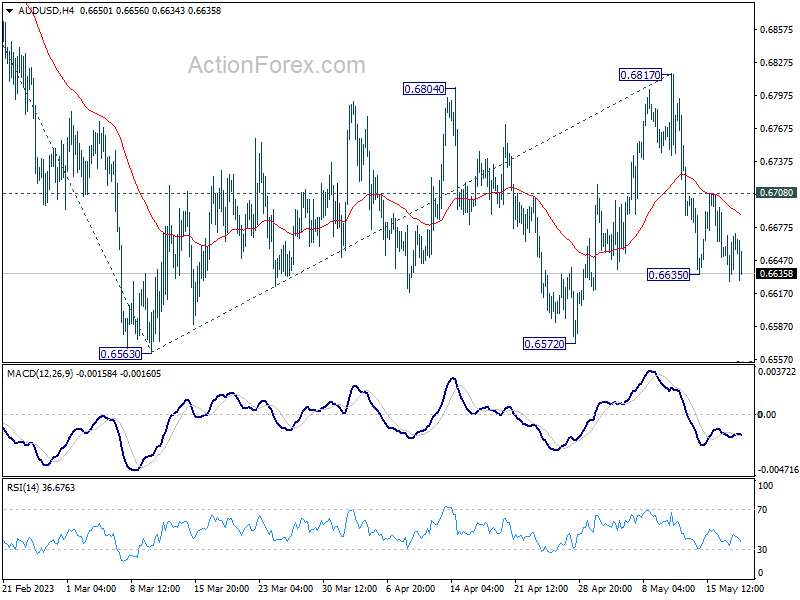

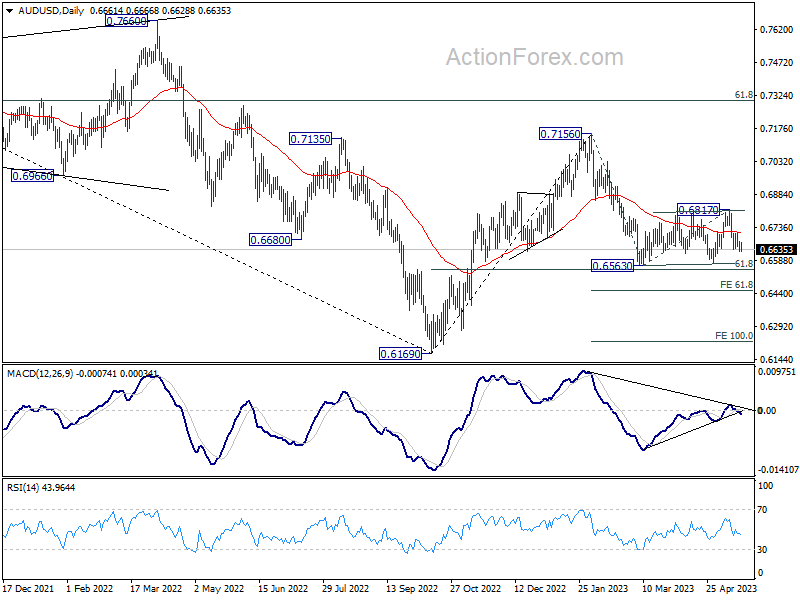

AUD/USD Daily Report

Daily Pivots: (S1) 0.6634; (P) 0.6654; (R1) 0.6678; More…

AUD/USD’s fall resumed after brief recovery and intraday bias is back on the downside for retesting 0.6563 low. As noted before, consolidation pattern from 0.6563 could have completed with three waves to 0.6817.Decisive break of 0.6563 will resume larger decline from 0.7156 to 61.8% projection of 0.7156 to 0.6563 from 0.6817 at 0.6451. On the upside, above 0.6708 minor resistance will turn intraday bias neutral again first.

In the bigger picture, the failure to break through 55 W EMA (now at 0.6822) keeps medium term outlook bearish. Firm break of 61.8% retracement of 0.6169 to 0.7156 at 0.6546 will raise the chance of long term down trend resumption through 0.6169 low. This will now be the favored case as long as 0.6817 resistance holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | PPI Input Q/Q Q1 | 0.20% | 0.50% | 0.50% | |

| 22:45 | NZD | PPI Output Q/Q Q1 | 0.30% | 0.80% | 0.90% | |

| 23:50 | JPY | Trade Balance (JPY) Apr | 0.80% | -1.08T | -1.21T | |

| 01:30 | AUD | Employment Change Apr | -4.3K | 25K | 53K | 61.1K |

| 01:30 | AUD | Unemployment Rate Apr | 3.70% | 3.50% | 3.50% | |

| 12:30 | CAD | New Housing Price Index M/M Apr | -0.10% | 0.00% | ||

| 12:30 | USD | Initial Jobless Claims (May 12) | 260K | 264K | ||

| 12:30 | USD | Philadelphia Fed Survey May | -20 | -31.3 | ||

| 14:00 | USD | Existing Home Sales Apr | 4.35M | 4.44M | ||

| 14:30 | USD | Natural Gas Storage | 109B | 78B |

{kind=link}