The financial markets remain firmly entrenched in a risk-on stance as signs increasingly point towards Fed “skipping” tightening at today’s rate decision. As a result, Yen, Swiss Franc, and Dollar are this week’s worst performers, exhibiting no clear indications of a resilient bounce. On the other end of the spectrum, Australian and New Zealand Dollar are emerging as the frontrunners, followed by Euro and Sterling.

This current wave of positive sentiment is expected to sustain in the near term. However, market participants should brace for a potential brief pullback once Fed’s decision to hold rates steady materializes. Furthermore, the release of new economic projections may incite some market volatility.

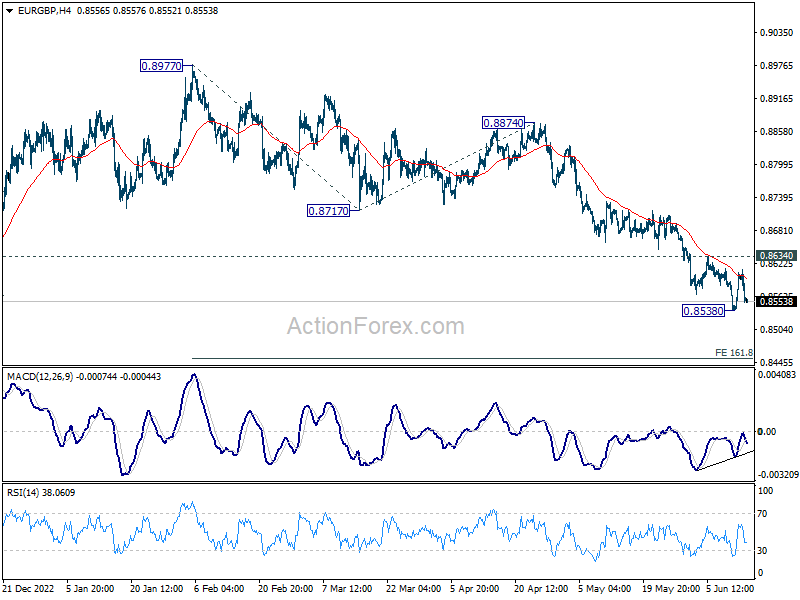

Technically, EUR/GBP is worth some attention in European session today. This week’s recovery was rather brief, and capped well below 0.8634 near term resistance. Outlook stays bearish in the cross. Break of 0.8538 will resume the whole decline from 0.8997 to 161.8% projection of 0.8977 to 0.8717 from 0.8874 at 0.8453. Today’s UK data might be a trigger for the move.

In Asia, at the time of writing, Nikkei is up 1.18%. Hong Kong HSI is down -0.05%. China Shanghai SSE is up 0.24%. Singapore Strait Times is up 0.70%. Japan 10-year JGB yield is up 0.0118 at 0.433. Overnight, DOW rose 0.43%. S&P 500 rose 0.69%. NASDAQ rose 0.83%. 10-year yield rose 0.074 to 3.839.

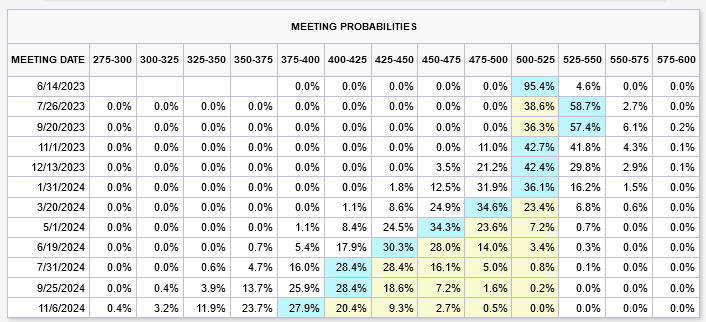

FOMC preview: 95% chance of a skip today, 60% chance of another hike in Jul

Yesterday’s cooling US consumer inflation data in May provided further solid ground for Fed to bypass tightening at today’s rate announcement. Fed funds futures now suggest a 95.4% probability of Fed maintaining status quo, holding rates steady at 5.00-5.25%. However, market sentiment leans towards the likelihood of another 25 bps to 5.25-5.50% in July, with over 60% chance.

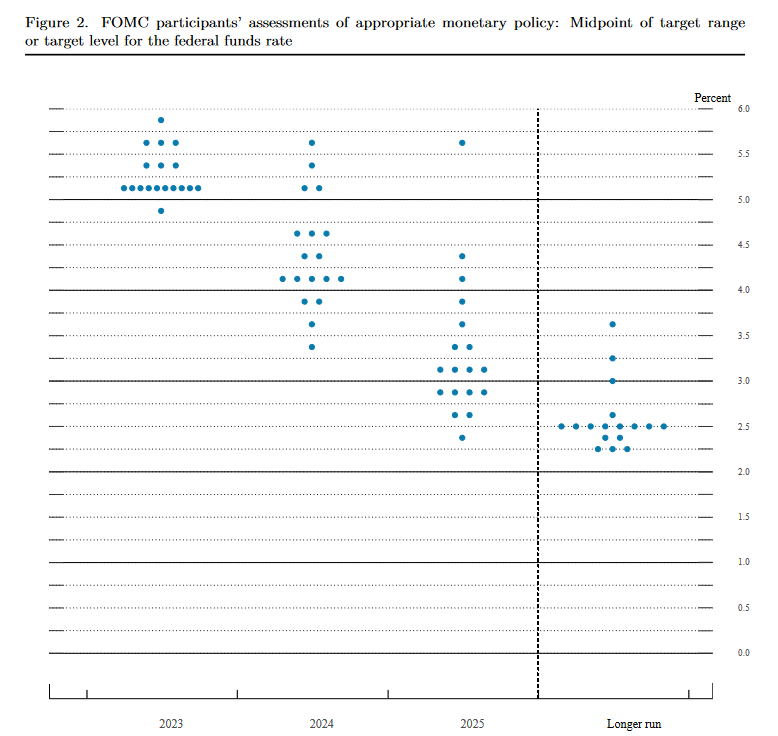

Yet, these market expectations are not set in stone and could see adjustments based on Fed’s new economic projections. Rewinding to March, the median interest rate stood at 5.1% for 2023. A perusal of the dot plot reveals that only one policymaker anticipated no additional rate hikes from the current level. In contrast, 10 policymakers forecast one more hike, while seven projected two or more. Changes in this balance could provide insights on whether the interest rate will peak at 5.25-5.50%, as currently predicted by the market.

Furthermore, median interest rate is expected to decline to 4.3% in 2024 and then to 3.1% in 2025. Any deviations from these projections could hint at the duration for which the interest rate will remain at its peak and potentially even suggest a timeline for the initial rate cut.

Some readings on Fed:

- Will Fed Pause After 10 Straight Hikes?

- Fed Preview: On Hold

- June Flashlight for the FOMC Blackout Period

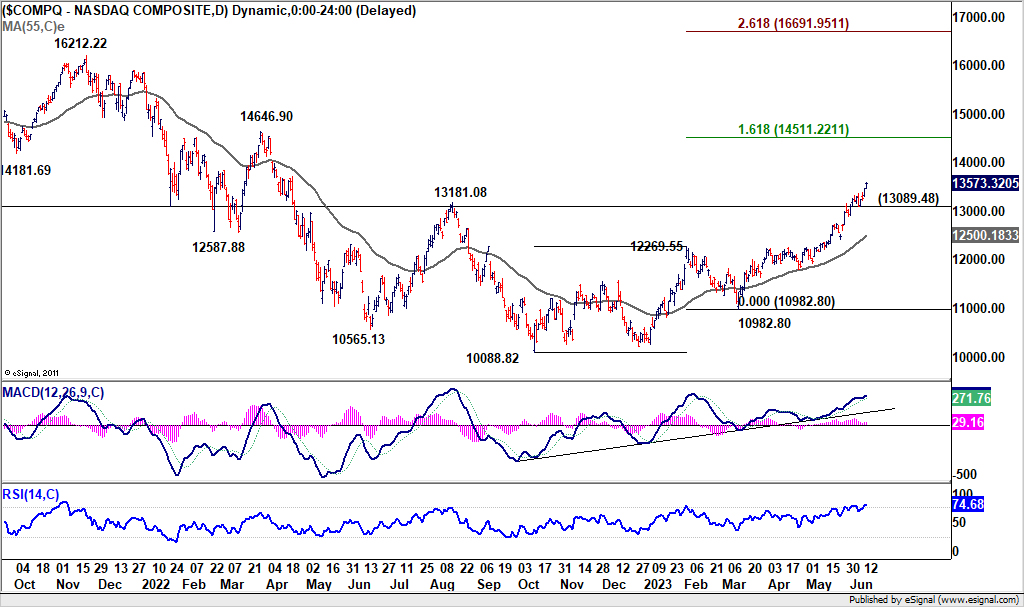

NASDAQ closed at 13-mth high, DOW broke resistance

US stocks surged broadly overnight as inflation data solidified a pause at today’s FOMC rate decision. NASDAQ extended its near term up trend to close at the highest level in 13 months. For now, near term outlook will stay bullish as long as 13089.48 support holds. Next target is 161.8% projection of 1088.82 to 12269.55 from 10982.80 at 14511.22.

DOW also made notable progress by breaking 34257.83 resistance, even though it could close above the level yet. Near term outlook will stay bullish as long as 55 D EMA (now at 33419.74) holds. Next target is 61.8% projection of 28660.94 to 34712.28 from 314289.82 at 35169.54. Sustained break there could prompt upside acceleration to retest 36952.65 record high.

Looking ahead

UK GDP, production and trade balance are the main feature in European session. Eurozone will also publish industrial production. Later in the day, US PPI will be released before FOMC rate decision and press conference.

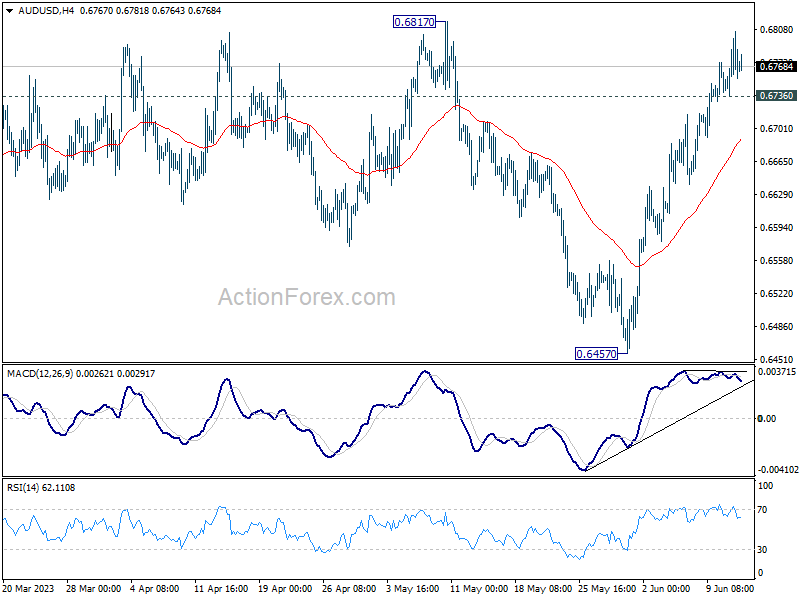

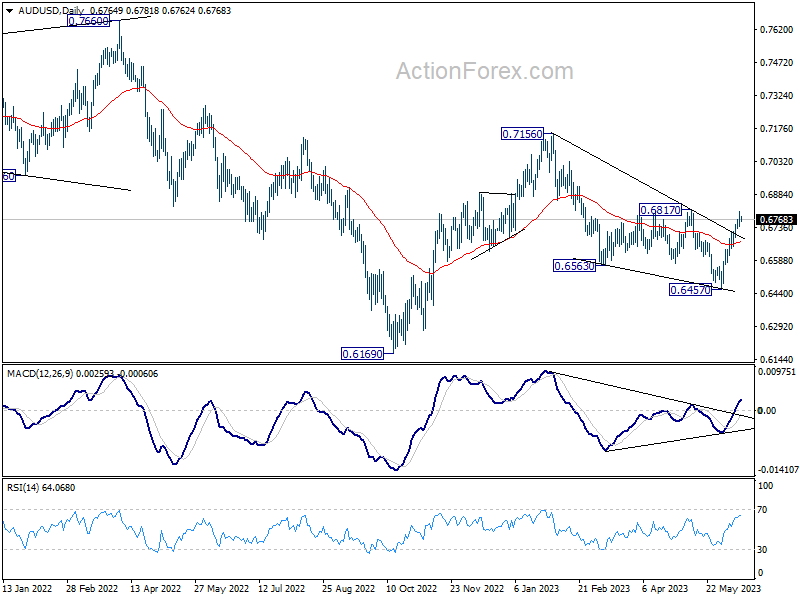

AUD/USD Daily Report

Daily Pivots: (S1) 0.6734; (P) 0.6771; (R1) 0.6803; More…

Intraday bias in AUD/USD remains on the upside as rise from 0.6457 is still in progress. Next target is 0.6817 structural resistance. Decisive break there should confirm near term bullish reversal, and pave the way to retest 0.7156 resistance next On the downside though, below 0.6736 minor support will turn intraday bias neutral first.

In the bigger picture, as long as 0.6817 resistance holds, the decline from 0.7156, as well as the down trend from 0.8006 (2021) are still in favor to continue through 0.6169 (2022 low) at a later stage. However, firm break of 0.6817 will indicate that fall from 0.7156 has completed in a three-wave corrective structure. Such development will argue that rise from 0.6169 is ready to resume through 0.7156, and add credence to the case that whole down trend from 0.8006 has completed already.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Current Account Q1 | -5.22B | -6.95B | -9.46B | |

| 06:00 | GBP | GDP M/M Apr | 0.20% | -0.30% | ||

| 06:00 | GBP | Industrial Production M/M Apr | -0.10% | 0.70% | ||

| 06:00 | GBP | Industrial Production Y/Y Apr | -2.60% | -2.00% | ||

| 06:00 | GBP | Manufacturing Production M/M Apr | -0.10% | 0.70% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Apr | -1.80% | -1.30% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Apr | -16.5B | -16.4B | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Apr | 1.20% | -4.10% | ||

| 12:30 | USD | PPI M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Y/Y May | 1.10% | 2.30% | ||

| 12:30 | USD | PPI Core M/M May | 0.20% | 0.20% | ||

| 12:30 | USD | PPI Core Y/Y May | 0.50% | 3.20% | ||

| 14:30 | USD | Crude Oil Inventories | -1.3M | -0.5M | ||

| 18:00 | USD | Fed Interest Rate Decision | 5.25% | 5.25% | ||

| 18:30 | USD | FOMC Press Conference |

{kind=link}