Asian stock markets commenced the week with divergent performances. While Japan’s Nikkei showed resilience, bouncing back after enduring its most challenging week this year, Hong Kong’s stocks weren’t as fortunate. The uncertainty surrounding China Evergrande Group’s protracted debt restructuring initiative ignited a fresh wave of selling, impacting not just Evergrande but also its contemporaries. Consequently, apprehensions around the beleaguered property sector have once again come to the fore.

In the currency markets, mixed market sentiments have cast a shadow Australian and New Zealand Dollar, making them a tad softer. Swiss Franc seems eager to further its selloff from last week. Meanwhile, both Dollar and Euro, along with Canadian Dollar, show signs of firmness. British Pound is making an attempt at a comeback, but the momentum remains tepid. Meanwhile, the Yen is leaning on the softer end of the spectrum. As the week progresses, eyes will be keenly set on inflation data releases from Australia, Eurozone, and US, potentially guiding the subsequent moves in currency markets.

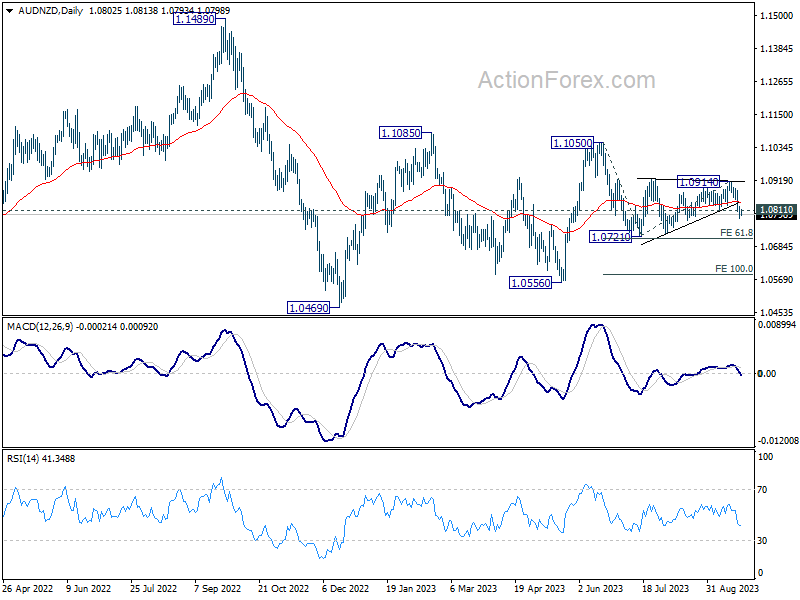

On the technical front, AUD/NZD’s break of 1.0811 support last week argues that the consolidation pattern from 1.0721 has completed at 1.0914. That is fall from 1.1050 is ready to resume. Near term risk will stay on the downside as long as 55 D EMA (now at 1.0839) holds. Next target is 61.8% projection of 1.1050 to 1.0721 from 1.0914 at 1.0711.

In Asia, at the time of writing, Nikkei is up 0.84%. Hong Kong HSI is down -1.24%. China Shanghai SSE is down -0.39% Singapore Strait Times is up 0.22%. Japan 10-year JGB yield is down -0.0142 at 0.735.

ECB’s Villeroy: Patience is more important now

ECB Governing Council member Francois Villeroy de Galhau spoke about the current monetary policy outlook in an interview with France Inter radio on Saturday. Emphasizing the need for a patient approach, Villeroy stated, “From today’s perspective, patience is more important than raising rates further.”

He highlighted the current deposit rate, which stands at a record 4%. According to Villeroy, this level should be held steady as it plays a crucial role in controlling inflation within Eurozone.

Amid concerns over the potential inflationary impact of rising oil prices on the global economy, Villeroy remained steadfast in the ECB’s commitment to its objectives.

“The recent increase in oil prices won’t derail the European Central Bank’s fight to tame inflation,” he asserted. Elaborating further on this, he said, “We’re very attentive, but [this] doesn’t put into doubt the underlying disinflation.”

Villeroy reiterated ECB’s target: “Our outlook and engagement is to bring inflation to around 2% in 2025.”

Oil’s ascension pauses as momentum exhausted, but 100 still a possibility

The financial world was abuzz last week with discussions of oil potentially breaking the 100 mark. While some pundits deem this as a stretch, the consensus is that no one can entirely dismiss the possibility.

The recent spike in oil prices brings with it a myriad of concerns, particularly about its ripple effect on the broader economy. As central banks globally grapple to suppress rising inflation, the surge in energy costs, with gasoline taking the lead, is becoming a pressing issue. Notably, August’s inflation readings surpassed expectations in several countries, with energy prices being the main instigator.

Tracing back to late June, energy prices have witnessed a consistent rise. This surge can be attributed to crude output reductions by major oil producers in OPEC+, coupled with additional cuts from Saudi Arabia. These decisions have propelled crude futures by approximately 30% over the past quarter.

With the possibility of OPEC+ announcing another surprise cut, bullish momentum could very well drive oil prices beyond 100. Contrarily, some anticipate that if prices climb above 95 per barrel, there might be a significant dip in demand, causing oil price to recalibrate and settle within a more balanced range.

From a technical perspective, WTI crude seems to have hit a near-term ceiling at 93.07 last week. Given that D MACD has already slid beneath the signal line, the prevailing bullish momentum may have been exhausted for the near term.

Nevertheless, decisive drop below 84.91 resistance turned support is essential to counteract the uptrend that began at 66.94. If this doesn’t materialize, the prospects of a continued rally remain. Break of 93.07 will put key resistance level at 50% retracement of 131.82 to 63.67 at 97.74 into focus.

Inflation data to stay in the global spotlight

Inflation continues to be the talk of global markets, as expectations and actual data often seem to dance around each other. Upcoming data from Australia, Eurozone, and US are poised to play a pivotal role in the evolving narrative.

Australia’s upcoming monthly CPI is projected to ascend from 4.9% yoy to 5.2% yoy in August. While this monthly figure doesn’t encompass the full spectrum of the CPI – given that a significant chunk of the data is disseminated quarterly – it does offer vital cues for market players to recalibrate their anticipations. Present consensus leans toward RBA maintaining its current policy in October, especially as Q3 figures will remain undisclosed. The November decision, however, remains contentious. A Bloomberg poll depicts a divide among experts, with 18 forecasting another hike by the year’s end and 17 foreseeing the status quo.

Moving to Europe, Eurozone’s CPI flash is anticipated to register a deceleration, coming in at 4.5% yoy in September, a dip from the previous 5.2%. Core CPI might also reflect a decline from 5.3% yoy to 4.8%. Following ECB recent 25bps rate increase, the bank is inclined toward a sustained pause. Philip Lane, the bank’s Chief Economist, underscored the adequacy of the current 4% deposit rate to realign inflation with 2% target within the projection horizon. This week’s figures could fortify this perspective.

Across the Atlantic, US core PCE inflation is projected to taper off to 3.9% yoy in August from the previous 4.2% yoy. Despite market skepticism, Fed’s recent communiqué underscored the possibility of another rate hike this year. With the subsequent FOMC meet slated for November 1, a slew of pertinent data remains to be assessed prior to policy determinations.

In addition to the above, markets will be tuned into several other key indicators this week, including US durable goods orders and consumer confidence, Germany’s Ifo business climate, Canada’s GDP, and Australia’s retail sales.

Here are some highlights for the week:

- Monday: Germany Ifo business climate.

- Tuesday: Japan corporate service prices; US house prices, new homes sales, consumer confidence.

- Wednesday: BoJ minutes; Australia CPI; Germany Gfk consumer sentiment; Eurozone M3; US durable goods orders.

- Thursday: New Zealand ANZ business confidence; Australia retail sales; Germany CPI flash; ECB bulletin; US Q2 GDP final, jobless claims, pending home sales.

- Friday: Japan Tokyo CPI, unemployment rate, industrial production, retail sales, consumer confidence, housing starts; Germany import prices, retail sales, unemployment; UK Q2 GDP final, M4 money supply, mortgage supply; France consumer spending; Swiss KOF economic barometer; Eurozone CPI flash; Canada GDP; US goods trade balance, personal income and spending, PCE inflation; Chicago PMI.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6408; (P) 0.6437; (R1) 0.6469; More…

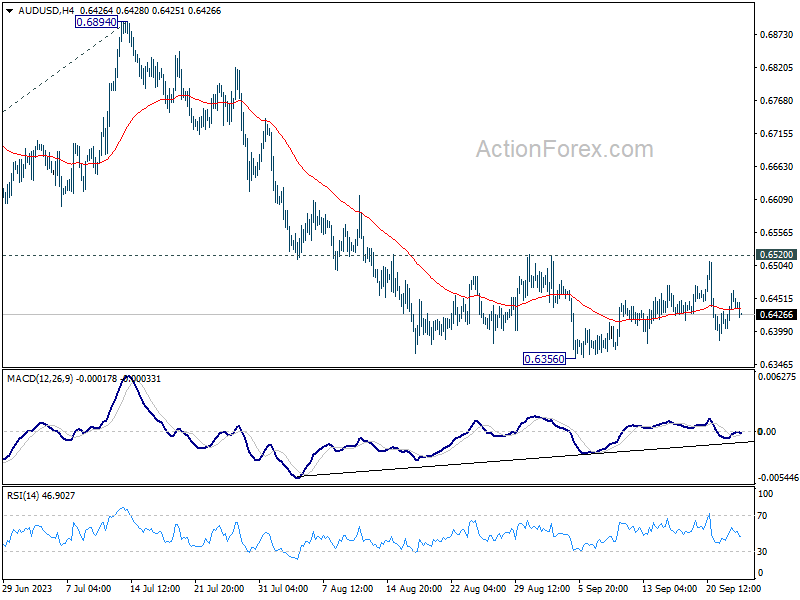

AUD/USD is staying in consolidation from 0.6356 and outlook is unchanged. Intraday bias remains neutral at this point. Further decline is expected as long as 0.6520 resistance holds. Break of 0.6356 will resume larger down trend to 100% projection of 0.7156 to 0.6457 from 0.6894 at 0.6195.

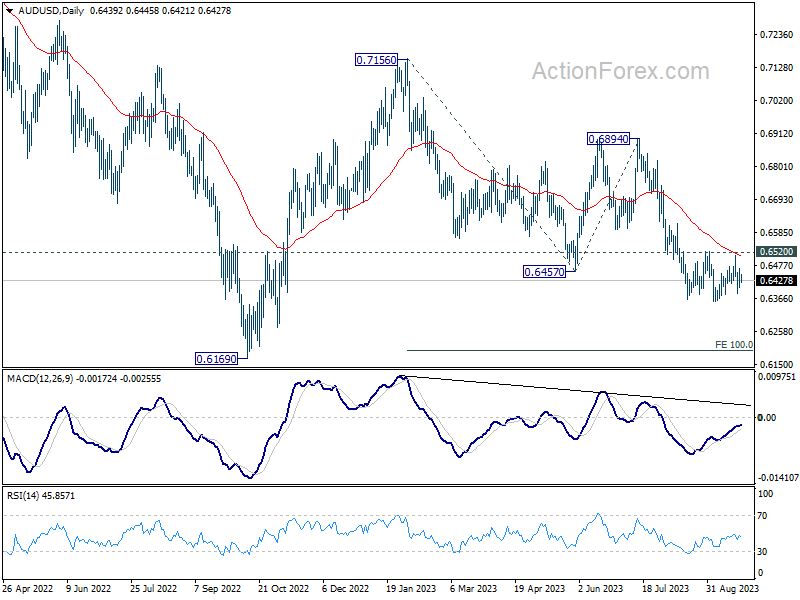

In the bigger picture, down trend from 0.8006 (2021 high) is possibly still in progress. Decisive break of 0.6169 will target 61.8% projection of 0.8006 to 0.6169 to 0.7156 at 0.6021. This will now remain the favored case as long as 0.6894, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:00 | EUR | Germany IFO Business Climate Sep | 85.2 | 85.7 | ||

| 08:00 | EUR | Germany IFO Current Assessment Sep | 88.0 | 89.0 | ||

| 08:00 | EUR | Germany IFO Expectations Sep | 82.8 | 82.6 |

{kind=link}