Financial markets are holding steady yet exhibit a sense of nervous anticipation as the new week commences. The conflicts between Israel and Hamas continues to take center stage, with concerns mounting over the potential for the violence to engulf the broader region. Volatility and unpredictability of the geopolitical situation mean that unexpected escalations could stir considerable market upheaval. While CPI and retail sales data from major economies are on this week’s radar, any significant geopolitical shifts would likely eclipse their impact.

Currency movements reflect the prevailing caution, with most major pairs and crosses operating within Friday’s range. US Dollar, Swiss Franc, and Yen are showing relative softness, indicative of the current market tranquility. New Zealand Dollar has nudged ahead, seemingly unaffected by general election results. Australian Dollar the Euro are trailing closely, while Sterling and Canadian Dollar are displaying mixed trends. However, market dynamics are fluid and rapid shifts are entirely plausible.

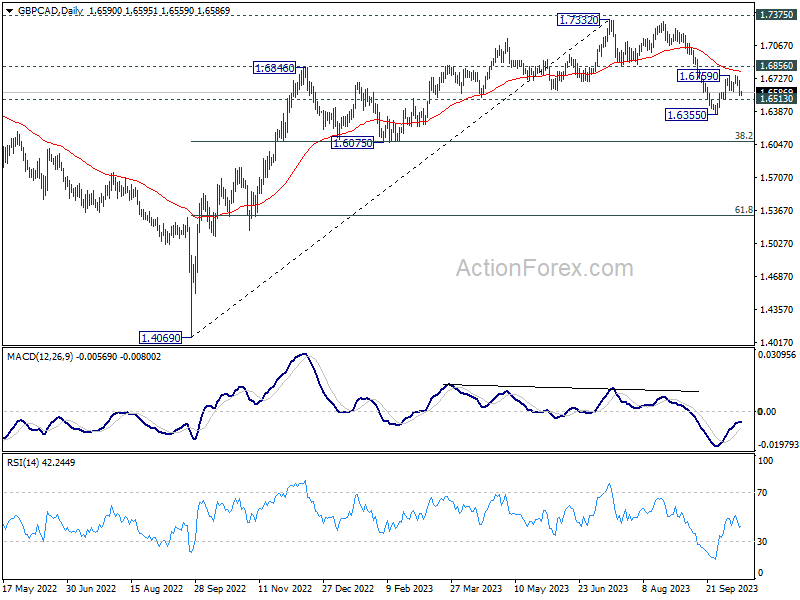

From a technical perspective, GBP/CAD is the currency pair to monitor closely this week, especially with CPI data releases slated for both UK and Canada. While recovery from 1.6355 might extend higher, near term outlook will stay bearish as long as 1.6586 support turned resistance holds. Break of 1.6513 minor support will suggest that fall from 1.7322 is ready to resume through 1.6355. Next target will be 1.6075 cluster support (38.2% retracement of 1.4069 to 1.7322 at 1.6086). Reaction from there will reveal whether GBP/CAD is correcting or reversing the rise from 1.4069.

In Asia, at the time of writing, Nikkei is down -1.86%. Hong Kong HSI is down -0.49%. China Shanghai SSE is down -0.34%. Singapore Strait Times is down -0.68%. Japan 10-year JGB yield is down -0.0061 at 0.753.

IMF Affirms Yen’s Movement Rooted in Fundamentals; Intervention Unwarranted

Sanjaya Panth, Deputy Director of IMF’s Asia and Pacific Department, indicated that Yen’s depreciation this year is primarily driven by fundamental factors, particularly interest rate differentials. He opined that current Yen dynamics don’t necessitate intervention. Although Japan’s inflation outlook is optimistic, Panth advises against immediate short-term rate hikes by BoJ due to global demand uncertainties. Instead, he suggests BoJ focus on enhancing flexibility of long-term interest rates.

He stated, “On the yen, our sense is that the exchange rate is driven pretty much by fundamentals. As long as interest rate differentials remain, the yen will continue to face pressure.”

Addressing the topic of foreign exchange interventions, Panth clarified IMF’s stance, emphasizing that interventions are justifiable only under specific scenarios: market severe dysfunction, elevated financial stability risks, or when inflation expectations become unanchored.

Reflecting on the recent fluctuations in Yen, he mentioned, “I don’t think any of the three considerations are existing right now,” essentially suggesting that the current Yen dynamics do not warrant any interventions by authorities.

Highlighting Japan’s economic outlook, Panth shared a more optimistic tone on the nation’s near-term inflation. He noted that there were “more upside than downside risks” to Japan’s inflation forecast, with the economy operating close to its full capacity. Additionally, price increments in Japanese market are predominantly fueled by robust demand.

However, Panth believes that BoJ should hold off on any immediate hikes in short-term rates. He expressed concerns over global demand trends, saying it was “not yet the time” to act given the potential impacts on Japan’s export-centric economy.

As a recommendation for BoJ’s ongoing strategy, Panth encouraged measures that enhance the flexibility of long-term interest rates. This would strategically set the stage for any required monetary tightening measures in the future.

ECB’s Lagarde: Eurozone Growth Faces Downward Pressure With Downside Risks

ECB President Christine Lagarde, during her speech at IMF annual meetings, highlighted the weakening activity in the Eurozone’s economy in Q3 due to slower with risks lean more towards the downside ahead. Lagarde expects continued decline in inflation, but the path has risks on both sides. She also reiterated that current interest rate would bring inflation down to target is maintained for “sufficiently long duration”.

She noted, “Incoming data suggest that activity has been weak in the third quarter,” attributing this to “slower global demand and the impact of tighter financing conditions.”

Lagarde noted that the “risks to the outlook continue to be tilted to the downside,” while also acknowledging the possibility that factors like a “strong labour market, rising real incomes, and receding uncertainty” could uplift growth.

On the inflation front, Lagarde expects decline in Eurozone, driven by “easing cost pressures” and the influence of tighter monetary policy. But, “the downward path has risks in both directions.” While upward risks could emanate from factors such as “renewed upward energy and food cost pressures,” potential downside risks could arise from “weaker demand” or a deteriorating international economic environment.

Lagarde also reiterated ECB’s stance on interest rates: “we consider that our key interest rates have reached levels that, maintained for a sufficiently long duration, will make a substantial contribution to the timely return of inflation to our target.”

New Zealand BNZ Service rose to 50.7, Yet Uncertainties Linger

New Zealand’s service sector showed signs of recovery in September, with BusinessNZ Performance of Services Index rising to 50.7, up from 47.7 in August. This improvement marks an end to the three consecutive months of contraction, though the index is still languishing below the long-term average of 53.5.

Among the key components, activity/sales witnessed a notable rise, moving up to 50.9 from 44.9. Meanwhile, employment indicators slightly dipped from 51.0 to 50.6. New orders/business experienced a healthy increase, reaching 53.9 from 48.5. However, stocks/inventories decreased to 47.9 from 51.4, while supplier deliveries inched up to 49.6 from 49.2.

Addressing the sentiment, BusinessNZ’s Chief Executive, Kirk Hope, pointed out that negative sentiments remained prevalent, with 61.8% in September, only slightly lower than 63.9% in August. A significant portion of these concerns was attributed to uncertainties surrounding the General Election and rising cost of living.

Week of Anticipated CPI and Retail Data Amid Global Uncertainties

The coming week promises to be eventful, with CPI data from major economies including UK, Japan, Canada, and New Zealand poised to draw significant attention. Other crucial economic releases in the limelight include retail sales figures from US and UK, employment data from UK and Australia, Germany’s ZEW economic sentiment, and China’s GDP figures.

Comments from BoE’s Governor, Andrew Bailey, last week signaled that upcoming policy decisions could be as closely contested as the recent 5-4 vote to maintain the status quo. Therefore, any unforeseen upside surprises in UK’s CPI data, especially when paired with a robust labor market and wage growth, could enhance the prospects of an interest rate hike in early November.

Over in Canada, concerns about inflation momentum have been vocalized by BoC Governor Tiff Macklem. During remarks made last Friday, the emphasis was placed on a discernible downturn in core inflation rates. As the bank prepares for its next meeting, the conversation will center on any “additional actions” needed to restore price stability. The CPI data set for release this week will play a pivotal role in shaping discussions for the upcoming October 25th meeting.

In Japan, expectations are tempered. Despite the anticipation surrounding CPI data, it’s believed to be too early for BoJ policymakers to consider the exit from negative interest rates. The consensus, even among the more optimistic board members, leans towards a cautious stance until concrete support materializes, potentially in early next year.

New Zealand is a wildcard this week, with the financial markets bracing for the aftermath of the general elections. While political developments will undoubtedly influence market sentiment, Q3 CPI data, expected this week, will offer markets substantial material to recalibrate divided opinions on the prospect of further rate hikes by the RBNZ.

All in all, as central banks across the globe mull over their next steps, economic releases this week will provide critical indicators, potentially shaping monetary policy directions for the remainder of the year.

Here are some highlights for the week:

- Monday: Eurozone trade balance; Canada manufacturing sales, wholesale sales; US Empire State manufacturing.

- Tuesday: New Zealand CPI; RBA minutes; Japan tertiary industry index; UK employment; Germany ZEW; Canada housing starts, CPI; US retail sales, industrial production, business inventories, NAHB housing index.

- Wednesday: China GDP, industrial production, retail sales, fixed asset investment, UK CPI, PPI; Eurozone CPI final; US housing starts and building permits, Fed’s Beige Book report.

- Thursday: Japan trade balance; Australia employment, NAB quarterly business confidence; Swiss trade balance; Canada IPPI and RMPI; US jobless claims, Philly Fed survey, existing home sales.

- Friday: New Zealand trade balance; UK Gfk consumer sentiment, retail sales; Japan CPI; Germany PPI; Canada retail sales.

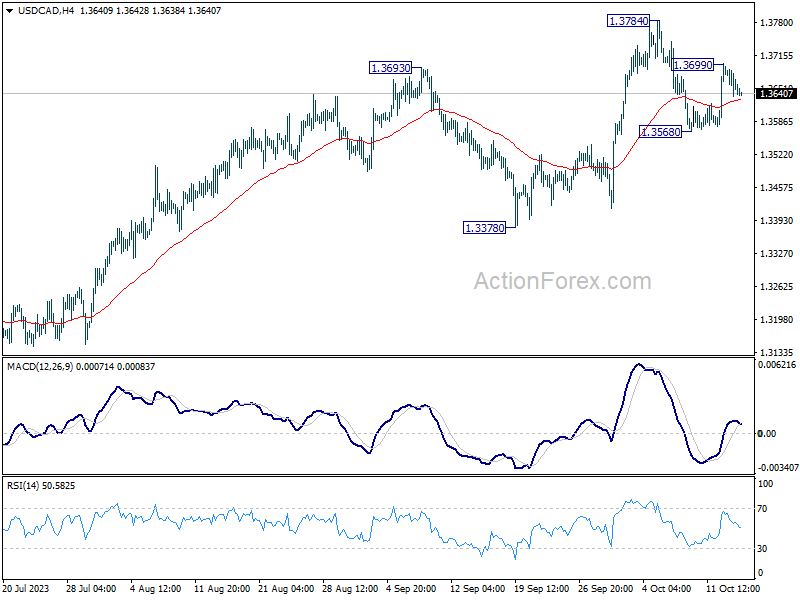

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3632; (P) 1.3663; (R1) 1.3690; More….

Intraday bias in USD/CAD is turned neutral as retreat from 1.3699 is extending today. On the upside, above 1.43699 will target 1.3784 first. Break there will will resume larger rise from 1.3091 to retest 1.3976 high. On the downside, below 1.3568 will bring another falling leg to extend the near term corrective pattern from 1.3784 instead.

In the bigger picture, current development revives the case that corrective pattern from 1.3976 (2022 high) has completed with three waves down to 1.3091. Decisive break of 1.3976 high will confirm resumption of up trend from 1.2005 (2021 low). Next target will be 61.8% projection of 1.2401 to 1.3976 from 1.3091 at 1.4064. This will now remain the favored case as long as 1.3378 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PSI Sep | 50.7 | 47.1 | 47.7 | |

| 23:01 | GBP | Rightmove House Price Index M/M Oct | 0.50% | 0.40% | ||

| 04:30 | JPY | Industrial Production M/M Aug F | -0.70% | 0.00% | 0.00% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Aug | 5.4B | 2.9B | ||

| 12:30 | CAD | Manufacturing Sales M/M Aug | 1.10% | 1.60% | ||

| 12:30 | CAD | Wholesale Sales M/M Aug | 2.50% | 0.20% | ||

| 12:30 | USD | Empire State Manufacturing Index Oct | -4.5 | 1.9 | ||

| 14:30 | CAD | BoC Business Outlook Survey |

{kind=link}