Dollar jumps in early US session, buoyed by a robust set of employment data. headline job growth exceeded expectations, narrowly missing 200k mark, while unemployment rate showed a decline. This data suggests a still-tight job market, raising concerns among some market participants that underlying inflation pressures may not be easing as hoped. Notably, strong wage growth stands out as a key indicator of persistent inflationary pressures.

Today’s positive employment figures are unlikely to change the prevailing expectation that Fed will keep interest rates unchanged at the upcoming meeting this month. However, the likelihood of an earlier-than-anticipated rate cut seems to have diminished. The market’s attention is now shifting towards next week’s key economic events, particularly the US CPI data on Tuesday and FOMC economic projections on Wednesday.

In terms of currency market performance for the week, Dollar has solidified its position as the second-best performer, although it remains far from challenging Yen for the top spot. Canadian Dollar ranks as the third strongest currency currently. On the other end of the spectrum, Australian and New Zealand Dollars occupy the weakest positions, followed closely by Sterling. Euro and Swiss Franc are showing mixed performances, positioned in the middle of the currency rankings.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.37%. CAC is up 0.90%. Germany 10-year yield is up 0.076 at 2.274. UK 10-year yield is up 0.073 at 4.046. Earlier in Asia, Nikkei fell -1.68%. Hong Kong HSI fell -0.07%. China Shanghai SSE rose 0.11%. Singapore Strait Times rose 1.19%. Japan 10-year JGB yield rose 0.0178 at 0.774.

US NFP grows 199k, unemployment rate down to 3.7%

US Non-Farm Payroll employment grew 199k in November, slightly above expectation of 190k. That was below the average monthly gain of 240k over the prior 12 months.

Unemployment rate fell from 3.9% to 3.7%, below expectation of 3.9%. Participation rate rose 0.1% to 62.8%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Over the past 12 months, average hourly earnings rose 4.0% yoy. Average workweek for all employments edged up by 0.1 hour to 34.4 hours.

BoE survey reveals lower public inflation expectation

The latest Bank of England/Ipsos quarterly Inflation Attitudes Survey show inflation expectations decreased in the near term. There’s also a shift in public sentiment towards a more balanced view of the economic situation in the UK, with decreasing number of people expecting further interest rate hikes and an increasing number advocating for stability or reduction in rates.

Median expectation for inflation over the coming year has decreased to 3.3%, down from 3.6% in August 2023. This decline suggests a growing optimism among respondents about the easing of inflationary pressures in the near term. However, when considering the twelve months following that period, expectations remain unchanged at 2.8%, indicating that respondents anticipate a stabilization of inflation rates in the longer term.

Regarding the future path of interest rates, there has been a notable shift in public opinion. Only 44% of respondents now expect rates to rise over the next 12 months, a significant decrease from the 63% who held this view in August. Conversely, 29% expect rates to stay about the same, up from 19%.

When asked about what would be “best for the economy”, only 11% of respondents suggested that rates should “go up”, down from 13%. Meanwhile, the proportion of respondents who believe that interest rates should “go down” remains steady at 40%, and those who think rates should “stay where they are” have increased to 29% from 26%.

Japan’s nominal pay rises 1.5% yoy, but fail to keep pace with inflation, consumer spending drops

Japan’s nominal pay growth rose by 1.5% yoy, surpassing the expected 1.0% yoy increase. This marked the fastest rate of increase since June. Regular or base salaries contributed to this increase with a 1.4% yoy rise. However, overtime pay slightly decreased by -0.1% yoy. Special payments, a variable component of wages, saw a significant jump of 7.5% yoy.

However, the positive trend in nominal pay was offset by the continued decline in inflation-adjusted real wages, which fell for the 19th consecutive month, dropping by -2.3% yoy. A labor ministry official commented, “Price increases have outpaced wage growth.” This situation is exacerbated by the consumer inflation rate, which includes fresh food prices but excludes owner’s equivalent rent, re-accelerating to 3.9% after a brief two-month slowdown.

Alongside wage trends, household spending in Japan also experienced a downturn, decreasing by -2.5% yoy in October. This decline, while still significant, was less severe than the anticipated 3.0% yoy drop. The continued decrease in household spending, which has now extended to eight consecutive months, reflects ongoing challenges in the domestic consumption sector.

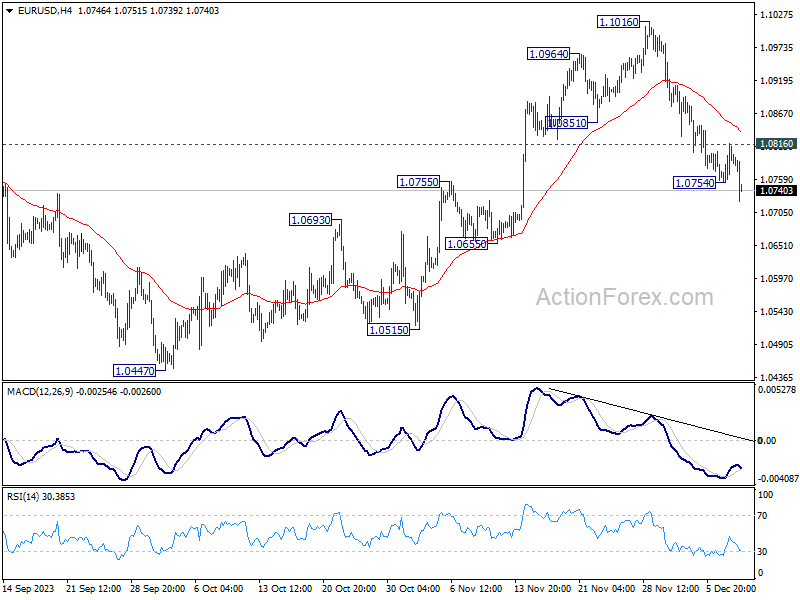

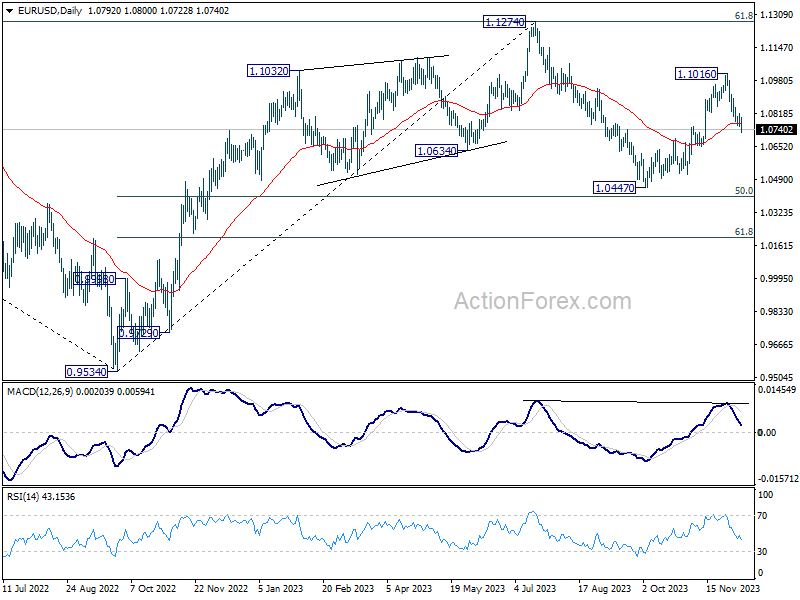

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0760; (P) 1.0788; (R1) 1.0822; More…

EUR/USD’s fall from 1.1016 resumed after brief recovery, and intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.0770) will pave the way to retest 1.0447 support. Nevertheless, break of 1.0894 will turn bias back to the upside for 1.1016 resistance instead. On the upside, above 1.0816 minor resistance will turn intraday bias neutral again.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern. Meanwhile, sustained break of 55 D EMA will argue that the third leg has already started for 1.0447 and below.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Sales Q3 | -2.80% | 0.20% | -0.80% | |

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 1.50% | 1.00% | 1.20% | |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | -2.50% | -3.00% | -2.80% | |

| 23:50 | JPY | Bank Lending Y/Y Nov | 2.80% | 2.80% | 2.80% | 2.70% |

| 23:50 | JPY | GDP Q/Q Q3 F | -0.70% | -0.50% | -0.50% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 | 5.30% | 5.10% | 5.10% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.62T | 1.85T | 2.01T | |

| 05:00 | JPY | Eco Watchers Survey: Current Nov | 49.5 | 49.2 | 49.5 | |

| 07:00 | EUR | Germany CPI M/M Nov F | -0.40% | -0.40% | -0.40% | |

| 07:00 | EUR | Germany CPI Y/Y Nov F | 3.20% | 3.20% | 3.20% | |

| 09:30 | GBP | Consumer Inflation Expectations | 3.30% | 3.60% | ||

| 13:30 | CAD | Capacity Utilization Q3 | 79.70% | 81.40% | 81.40% | |

| 13:30 | USD | Nonfarm Payrolls Nov | 199K | 190K | 150K | |

| 13:30 | USD | Unemployment Rate Nov | 3.70% | 3.90% | 3.90% | |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.40% | 0.30% | 0.20% | |

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | 61.7 | 61.3 |

{kind=link}