Sterling is taking a modest step back today, responding to UK’s latest inflation report that came in below market expectations. Despite this, the actual figures for both headline and core CPI merely held their ground compared to the previous month’s readings, signaling continued pause in disinflationary progress. Additionally, the report highlighted a slight uptick in services inflation.

Consequently, the data underscores a lingering necessity for the BoE to adopt a wait-and-see approach, and data more economic data before acting on interest rate. August still appears more feasible than an earlier first cut in May. Consequently, Sterling’s reaction was measured, reflecting a cautious recalibration of expectations rather than a drastic reassessment of the BoE’s monetary policy path

In the broader currency market, Dollar softens slightly today, taking a moment to consolidate after achieving significant gains earlier in the week. Euro and Swiss Franc found themselves on the softer side as well. Conversely, Australian Dollar found favor among traders, buoyed by an easing in risk aversion. Yen’s performance is mixed, showing indifference to Japan’s verbal interventions amid its depreciation past the 150 mark against Dollar.

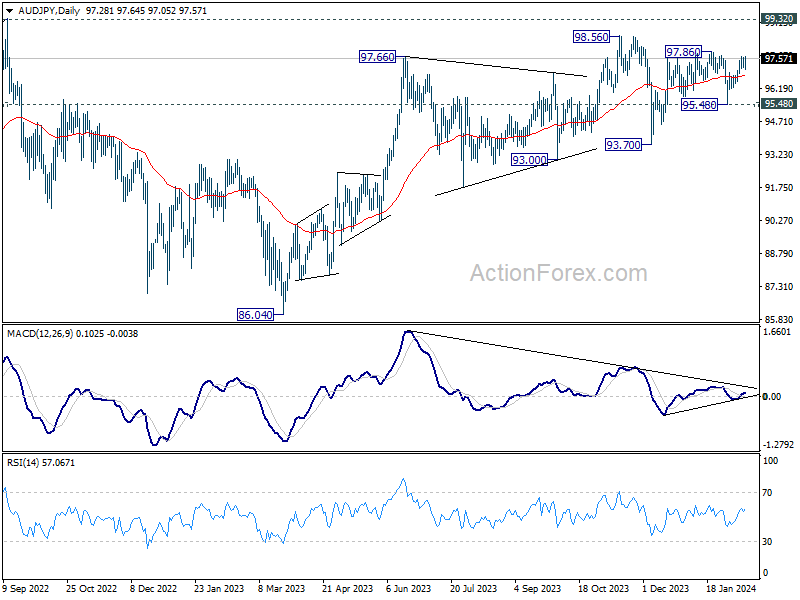

AUD/JPY is a pair to watch in the upcoming Asian session, with Japan GDP and Australia employment data due. The cross rebounded strong strong after a brief dip to 95.48 earlier in the month. Further rise is mildly in favor and break of 97.86, or even 98.56, could be seen. However, based on current momentum. Upside would likely be limited by 99.32 (2022 high).

In Europe, at the time of writing, FTSE is up 0.87%. DAX is up 0.35%. CAC is up 0.59%. UK 10-year yield is down -0.067 at 4.088. Germany 10-year yield is down -0.022 at 2.375. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI rose 0.84%. Singapore Strait Times fell -0.09%. Japan 10-year JGB yield rose 0.0304 to 0.760.

ECB’s de Guindos: we must not get ahead of ourselves

ECB Vice President Luis de Guindos acknowledged in a speech that inflation is moving “on the right track” towards target. But he also pointed out several factors that could derail progress.

De Guindos highlighted “wage pressures” as a crucial factor yet to show signs of easing, alongside the potential for “profit margins” to remain robust. Furthermore, he pointed to “heightened geopolitical tensions,” especially in the Middle East, as a risk that could lead to increased energy prices and disrupt global trade, complicating the inflation outlook.

“While we are heading in the right direction, we must not get ahead of ourselves,” he said, indicating that it would take “some more time” to gather necessary data to confirm that inflation is on a stable path towards 2% target.

The coming months are expected to provide crucial insights into underlying inflation drivers, with forthcoming data on wage settlements and firms’ pricing behaviors, along with new economic projections in March, set to inform ECB’s future policy decisions.

Eurozone industrial production rises 2.6% mom in Dec, vs exp -0.3% mom

Eurozone industrial production rose 2.6% mom in December, much better than expectation of -0.3% mom decline. Production grew by 20.5% for capital goods, by 0.5% for durable consumer goods, by 0.3% for energy and by 0.2% for non-durable consumer goods, while production fell by -1.2% for intermediate goods.

EU industrial production also rose 2.6% mom. Among Member States for which data are available, the highest monthly increases were registered in Ireland (+23.5%), the Netherlands (+6.6%) and Denmark (+5.6%). The largest decreases were observed in Slovenia (-7.4%), Croatia (-4.3%) and Finland (-2.7%).

UK CPI and core unchanged in Jan, at 4.0% and 5.1%

UK CPI fell -0.6% mom in January, below expectation of -0.3% mom. Annually, CPI was unchanged at 4.0% yoy, below expectation of 4.1% yoy.

Core CPI (excluding energy, food, alcohol and tobacco) was also unchanged at 5.1% yoy, below expectation of 5.2% yoy. CPI goods slowed from 1.9% yoy to 1.8% yoy. CPI services accelerated from 6.4% yoy to 6.5% yoy.

The largest upward contribution to the monthly change in both CPI annual rates came from housing and household services (principally higher gas and electricity charges), while the largest downward contribution came from furniture and household goods, and food and non-alcoholic beverages.

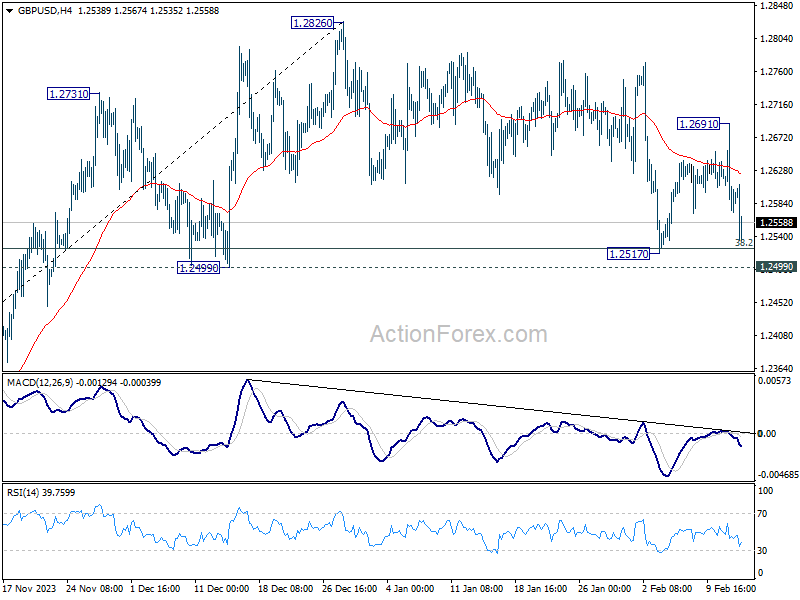

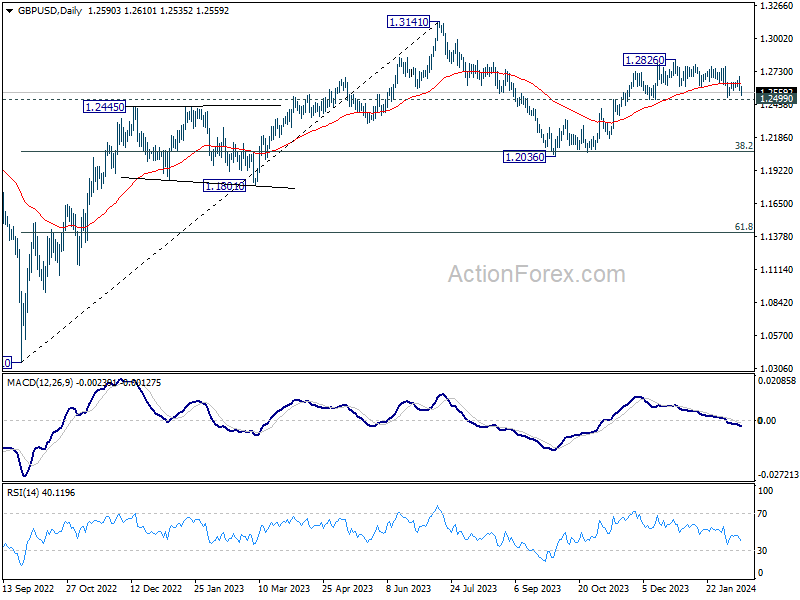

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2549; (P) 1.2617; (R1) 1.2661; More…

GBP/USD dips notably today but stays above 1.2517 support. Intraday bias remains neutral for the now. On the upside, break of 1.2691 resistance will indicate that correction from 1.2826 has completed. Intraday bias will be back on the upside for retesting 1.2826. Nevertheless, decisive break of 1.2499 will argue that whole rise from 1.2036 has completed and turn near term outlook bearish.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which could be still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2499 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 07:00 | GBP | CPI M/M Jan | -0.60% | -0.30% | 0.40% | |

| 07:00 | GBP | CPI Y/Y Jan | 4.00% | 4.10% | 4.00% | |

| 07:00 | GBP | Core CPI Y/Y Jan | 5.10% | 5.20% | 5.10% | |

| 07:00 | GBP | RPI M/M Jan | -0.30% | -0.10% | 0.50% | |

| 07:00 | GBP | RPI Y/Y Jan | 4.90% | 5.20% | 5.20% | |

| 07:00 | GBP | PPI Input M/M Jan | -0.80% | 0.00% | -1.20% | -0.40% |

| 07:00 | GBP | PPI Input Y/Y Jan | -3.30% | -3.00% | -2.80% | -2.10% |

| 07:00 | GBP | PPI Output M/M Jan | -0.20% | -0.20% | -0.60% | -0.50% |

| 07:00 | GBP | PPI Output Y/Y Jan | -0.60% | -0.50% | 0.10% | |

| 07:00 | GBP | PPI Core Output M/M Jan | 0.20% | 0.00% | -0.10% | |

| 07:00 | GBP | PPI Core Output Y/Y Jan | -0.40% | 0.10% | 0.00% | |

| 10:00 | EUR | Eurozone GDP Q/Q Q4 P | 0.00% | 0.00% | 0.00% | |

| 10:00 | EUR | Eurozone Employment Change Q/Q Q4 P | 0.30% | 0.20% | 0.20% | |

| 10:00 | EUR | Eurozone Industrial Production M/M Dec | 2.60% | -0.30% | -0.30% | 0.40% |

| 15:30 | USD | Crude Oil Inventories | 3.3M | 5.5M |

{kind=link}