Dollar weakens broadly after FOMC rate decision that provides little news to the markets. Instead, traders are keen awaiting US President Donald Trump’s announcement on nominating Fed Governor Jerome Powell to take over Fed chair job next year. The announcement is expected at 3pm New York Time today. Also, after a day of delay, House is set to reveal the details of the tax bill. But the greenback could continue to stay in range and wait for tomorrow’s non-farm payroll report. Meanwhile, Sterling remains the strongest one for the week as markets await the highly anticipated BoE rate hike.

As widely anticipated, the November FOMC meeting contained few changes from the previous one. The members left the target range of the Fed funds rate unchanged at 1-1.25%. One surprise came from the upgrade of the growth assessment to ‘solid’ for the first time since 2015, despite disruptions by hurricanes. Inflation stayed below the 2% target and the members acknowledged that core inflation ‘remained soft’. However, the encouraging growth outlook and further decline in the unemployment rate suggest that a December rate hike remains on track. More in FOMC Upgraded Growth Assessment First Time In Two Years, December Hike On Track

Also on FOMC:

- FOMC Review: Overshadowed by Fed Chair Announcement Tomorrow

- Few Changes from the Fed as December Hike Appears on Track

- Fed Holds the Line on Rates in November

- Few Surprises from the FOMC

House Ways and Means Committee Chairman Kevin Brady said yesterday that Republicans will "definitely" reveal the details of the tax bills today. Brady also hinted on a phased approach on tax cuts for businesses. Responding on questions of whether the cuts are permanent Brady said that "that’s our goal, and I think it’s going to take several steps through the process to achieve that." But it’s believed that the purpose of the phased approach is to get around with Senate budget rules and Democratic filibuster.

BoE to hike for the first time in a decade

BoE is widely expected to hike interest rate for the first time in a decade. The Bank Rate would be raised by 25bps to 0.50%. The core question is whether this is a one-off hike. In our view, it will be a one-off as the Bank Rate will be brought back to pre-Brexit referendum level. The impact of the voting decision is largely absorbed by the monetary stimulus as well as depreciation in Sterling. BoE policy makers would hesitate to make any more move before getting a clearer picture on Brexit. With that in mind, the vote split of the decision is the first key point to watch. The tighter the decision, the more unlikely for another hike in near term. In addition, BoE will release the quarterly inflation report. Revision in inflation projection there will tell us how policymakers general feel about the recent surge in inflation.

ECB Hansson: Tapering a minor issue

ECB Governing Council Member Ardo Hansson said yesterday that tapering the asset purchase is a "minor issue" for the central bank. He noted that "How we move in the future … to zero, is a very minor issue in the context where the stock of accumulated purchases is already in the trillions of euros." And, "so the question about 10 billion euros there or the precise phasing, I think is not really a material issue". That is taken by a sign by some that ECB could be moving the policy focus away from asset purchases. That is, the central bank will put more emphasis on tools like interest rates, or forward guidance.

Japan PM Abe undecided yet on next BoJ head

In Japan, the question on whether BoJ Governor Haruhiko Kuroda would be given another five year term next year is still unanswered. Prime Minister Shinzo Abe expressed his recognition on Kuroda’s achievements. He said that "we have created a situation in a short period of time that Japan is no longer in deflation as a result of strengthening policy coordination between the government and the BOJ." And, "the government and the BOJ have achieved a major result on employment, which is the most important responsibility of politics." But he also noted he had "no decided at all" on who will lead BoJ after Kuroda’s term expires next April.

On the data front

Australian Dollar rebounds notably today after positive economic data. Trade surplus widened to AUD 1.75b in September, above expectation of 1.2b. Building approvals rose 1.5% in October versus expectation of -1.0% fall. Japan monetary base rose 14.5% yoy in October.

Swiss will release retail sales and SECO consumer confidence and retail sales in European session. Eurozone will release PMI manufacturing revision and German unemployment. UK will release construction PMI but focus will be on BoE rate decision and inflation report.

From US, jobless claims, Challenger job cuts and non-farm productivity will be featured.

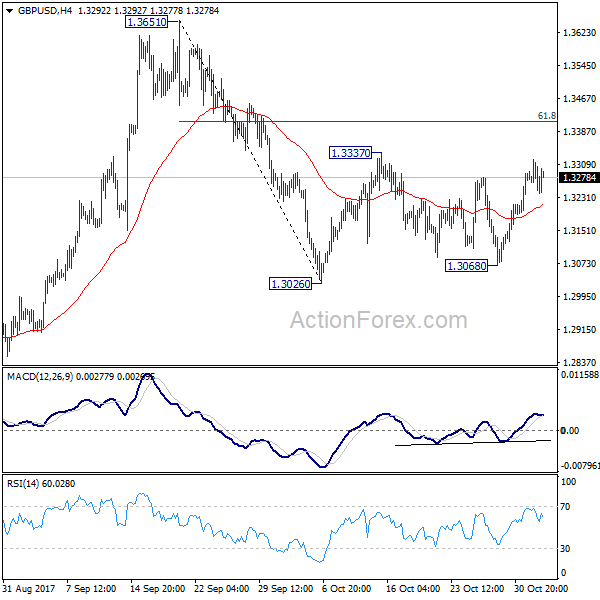

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3216; (P) 1.3268; (R1) 1.3297; More….

GBP/USD rebounded strongly from 1.3068 but overall outlook is unchanged. Price actions from 1.3026 are seen as forming a consolidation pattern. Further rise and break of 1.3337 cannot be ruled out. But upside should be limited by 61.8% retracement of 1.3651 to 1.3026 at 1.3412 to bring fall resumption finally. On the downside, firm break of 1.3026 support will resume the decline from 1.3651 and target 1.2773 key support level. This will also revive the case of medium term reversal. However, sustained break of 1.3412 will turn focus back to 1.3651 high.

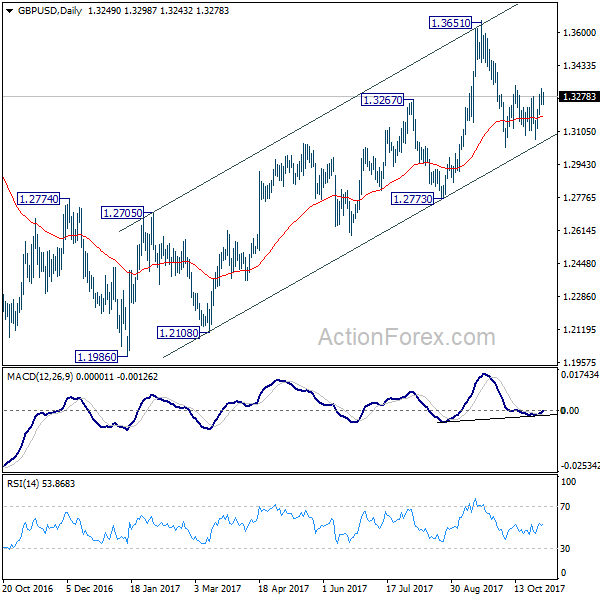

In the bigger picture, while the medium term rebound from 1.1946 was strong, GBP/USD hit strong resistance from the long term falling trend line. Outlook is turned a bit mixed and we’ll stay neutral first. On the downside, decisive break of 1.2773 key support will argue that rebound from 1.1946 has completed. The corrective structure of rise from 1.1946 to 1.3651 will in turn suggest that long term down trend is now completed. Break of 1.1946 low should then be seen. On the upside, break of 1.3835 support turned resistance will revive the case of trend reversal and target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466 .

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Monetary Base Y/Y Oct | 14.50% | 15.70% | 15.60% | |

| 00:30 | AUD | Trade Balance Sep | 1.75B | 1.20B | 0.99B | 0.87B |

| 00:30 | AUD | Building Approvals M/M Sep | 1.50% | -1.00% | 0.40% | |

| 05:00 | JPY | Consumer Confidence Oct | 43.6 | 43.9 | ||

| 06:45 | CHF | SECO Consumer Confidence Oct | 0 | -3 | ||

| 08:15 | CHF | Retail Sales Real Y/Y Sep | 0.30% | -0.20% | ||

| 08:45 | EUR | Italy Manufacturing PMI Oct | 56.5 | 56.3 | ||

| 08:50 | EUR | France Manufacturing PMI Oct F | 56.7 | 56.7 | ||

| 08:55 | EUR | German Unemployment Change Oct | -10K | -23K | ||

| 08:55 | EUR | German Unemployment Claims Rate Oct | 5.60% | 5.60% | ||

| 08:55 | EUR | Germany Manufacturing PMI Oct F | 60.5 | 60.5 | ||

| 09:00 | EUR | Eurozone Manufacturing PMI Oct F | 58.6 | 58.6 | ||

| 09:30 | GBP | Construction PMI Oct | 48.5 | 48.1 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Oct | -27.00% | |||

| 12:00 | GBP | BoE Bank Rate | 0.50% | 0.30% | ||

| 12:00 | GBP | BoE Asset Purchase Target | 435B | 435B | ||

| 12:00 | GBP | MPC Official Bank Rate Votes | 9–0–0 | 2–0–7 | ||

| 12:00 | GBP | MPC Asset Purchase Facility Votes | 0–0–9 | 0–0–9 | ||

| 12:00 | GBP | Bank of England Inflation Report | ||||

| 12:30 | USD | Initial Jobless Claims (OCT 28) | 235K | 233K | ||

| 12:30 | USD | Nonfarm Productivity Q3 P | 2.50% | 1.50% | ||

| 12:30 | USD | Unit Labor Costs Q3 P | 0.40% | 0.20% | ||

| 14:30 | USD | Natural Gas Storage | 64B |