Yen’s pull back continues today despite more positive news on wages negotiations in Japan. Remarkably, the currency has undone its gains from last week against all major counterparts, barring the even more beleaguered New Zealand Dollar. Expectations are still leaning towards an imminent interest rate hike by BoJ; however, speculation is rife that the central bank may postpone this move to April to coincide with the release of new economic projections.

Dollar remains the strongest currency for the week, although it has started to lose some momentum. Traders seem to be adopting a more cautious stance in anticipation of next week’s FOMC meeting and the forthcoming economic projections. The financial markets are bracing for a significant week ahead, with several other major central banks, including BoJ, RBA, SNB, and BoE, all scheduled to announce their monetary policy decisions. In light of these upcoming events, it is unsurprising that traders are hesitant to place substantial bets during the last trading session of the week.

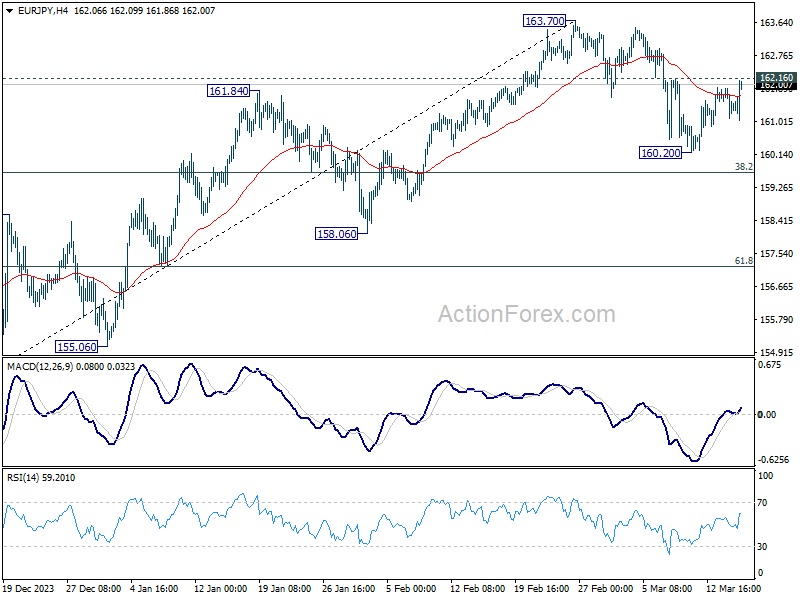

Technically, EUR/JPY is now eyeing 162.16 minor resistance with current rebound. Firm break there will argue that corrective fall from 163.70 has completed at 160.20 already, and stronger rise would be seen back to retest 163.70 resistance. However, it is crucial to bear in mind the considerable market risk posed by the upcoming BoJ rate decision next Tuesday, which could overturn all the technical development. So, any bounce could be short lived until 163.70 is firmly taken out with power.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is up 0.41%. CAC is up 0.50%. UK 10-year yield is up 0.024 at 4.216. Germany 10-year yield is up 0.0177 at 2.445. Earlier in Asia, Nikkei fell -0.26%. Hong Kong HSI fell -1.42%. China Shanghai SSE rose 0.54%. Singapore Strait Times fell -0.42%. Japan 10-year JGB yield rose 0.0174 to 0.793.

US Empire state manufacturing dives to -20.9, activity falls significantly

US Empire State Manufacturing Index fell sharply from -2.4 to -20.9 in March, well below expectation of -6.5. Looking at some details, new orders fell from -6.3 to -17.2. Shipments fell from 2.8 to -6.9. Prices paid fell from 33.0 to -28.7. Prices received ticked up from 17.0 to 17.8. Number of employments fell from -0.2 to -7.1. Average workweek fell from -4.7 to -10.4.

Richard Deitz, Economic Research Advisor at the New York Fed said: “Manufacturing activity fell significantly in New York State in March, with a decline in new orders pointing to softening demand. Labor market conditions remained weak as both employment and hours worked decreased.”

Japan’s Shunto negotiations yield 5.28% pay rise, a 33-Year High

Japan’s annual labor negotiations, known colloquially as “Shunto” or the “spring wage offensive,” have culminated in a remarkable outcome this year, with major firms agreeing to a pay increase of 5.28%—the highest in 33 years.

This significant hike, announced by the country’s largest trade union group Rengo, surpasses the previous year’s increase of 3.80%. With wage talks for smaller companies anticipated to wrap up by the end of March, this development is a critical one in the context of monetary policy considerations by BoJ.

This wage growth is likely to be viewed positively by BoJ officials, who are widely expected to be on the verge of ending the long-standing negative interest rate policy. However, the exact timing of such a policy shift, whether it could be announced as soon as next week’s meeting or delayed until April, remains a matter of speculation.

A recent Reuters poll conducted between March 11 and 14 showed that out of 34 economists surveyed, only 12 anticipate a rate hike in the upcoming week. The majority, 21 out of 34, foresee such a move in April.

Those in favor of an April decision point to BoJ’s access to more comprehensive information by then, including results from Tankan survey, insights from branch managers, and a new set of economic projections.

Yet, history has shown that BoJ has a penchant for surprising the markets. This unpredictability serves as a reminder to never rule out the possibility of a sooner move.

NZ BNZ manufacturing climbs to 49.3, a glimmer of hope in ongoing recession

New Zealand BusinessNZ Performance of Manufacturing Index rose from 47.5 to 49.3 , marking the highest point in a year. However, the sub-50 reading indicates that the sector remains in contraction for the twelfth consecutive month.

A closer examination of the components reveals a mixed bag of progress and setbacks. Production saw a significant leap from 42.9 to 49.1, reaching its peak since January 2023. Contrarily, employment edged down to the breakeven point of 50.0 from 51.3. New orders continued to struggle, remaining unchanged at 47.8 and indicating contraction for the ninth month in a row, reflecting the ongoing difficulty in securing new business. Finished stocks and deliveries both saw improvements, with deliveries crossing into expansion territory at 51.4, the highest since March 2023.

Despite these developments, the sector’s sentiment remains cautious, with 62% of comments being negative in February, marginally less pessimistic than January’s 63.2% but more so than December’s 61%. The primary concerns among respondents were a lack of orders, both domestically and internationally, and a general slowdown in the economy.

Stephen Toplis, BNZ’s Head of Research acknowledged that while New Zealand’s manufacturing sector “is still in recession”, the latest PMI data signals “there is light at the end of the tunnel”. The proximity of the PMI to the “breakeven” threshold and the positive differential between new orders and inventory suggest an upcoming increase in production.

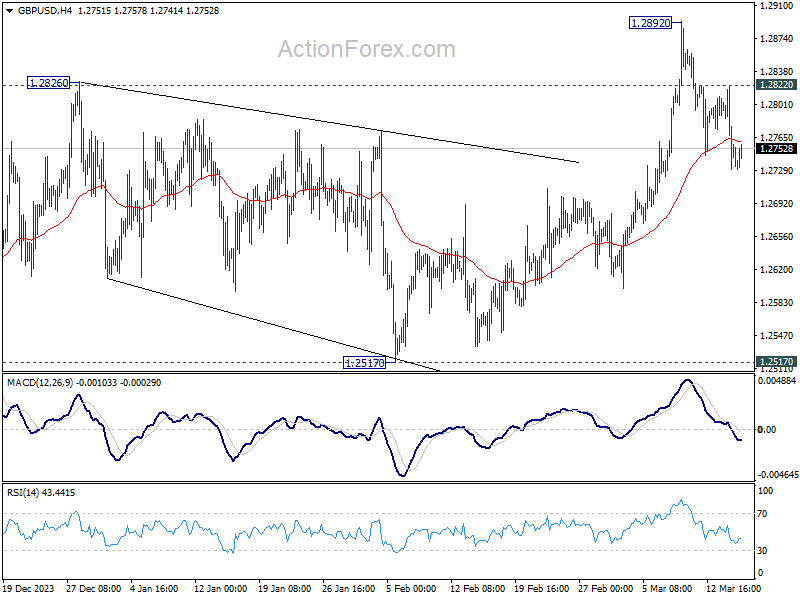

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2769; (R1) 1.2807; More…

Intraday bias in GBP/USD remains mildly on the downside at this point. Fall from 1.2892 short term top would target 55 D EMA (now at 1.2673). Sustained break there will target 1.2517 structural support next. For now, risk will stay mildly on the downside as long as 1.2822 minor resistance holds, in case of recovery.

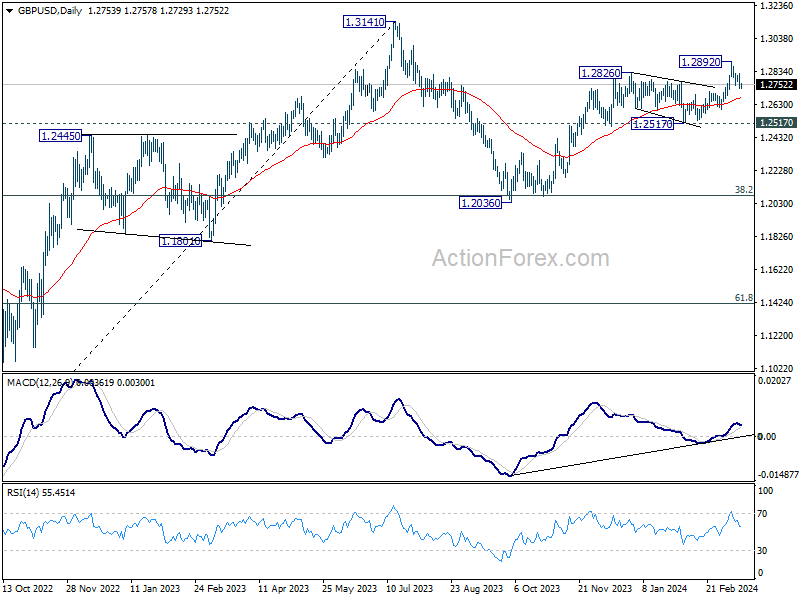

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern to up trend from 1.0351 (2022 low). Rise from 1.2036 is seen as the second leg, which is still in progress. But upside should be limited by 1.3141 to bring the third leg of the pattern. Meanwhile, break of 1.2517 support will argue that the third leg has already started for 38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075 again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ PMI Feb | 49.3 | 47.3 | 47.5 | |

| 04:30 | JPY | Tertiary Industry Index M/M Jan | 0.30% | 0.10% | 0.70% | |

| 09:30 | GBP | Consumer Inflation Expectations | 3.00% | 3.30% | ||

| 10:00 | EUR | Italy Retail Sales M/M Jan | -0.10% | 0.20% | -0.10% | -0.20% |

| 12:15 | CAD | Housing Starts Y/Y Feb | 253K | 227K | 224K | 223K |

| 12:30 | CAD | Wholesale Sales M/M Jan | 0.10% | -0.60% | 0.30% | |

| 12:30 | USD | NY Empire State Manufacturing Index Mar | -20.9 | -6.5 | -2.4 | |

| 12:30 | USD | Import Price Index M/M Feb | 0.30% | 0.20% | 0.80% | |

| 13:15 | USD | Industrial Production M/M Feb | 0.00% | -0.10% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Mar P | 77.3 | 76.9 |

{kind=link}