Yen’s renewed selloff captured some attention in the otherwise subdued Asian session today. With no new comments from Japanese authorities, market participants are left to speculate on when and where the next intervention might occur. A pivotal moment on the horizon is BoJ’s meeting on July 31, where the central bank is expected to outline its tapering plans for bond purchases. Additionally, there is prospect that BoJ might raise interest rates again to counteract the negative impacts of Yen’s depreciation on the economy. Some analysts suggest that if BoJ’s measures fail to meet market expectations, Yen could plunge straight to 170 level against Dollar. However, the immediate focus remains on whether 165 is the intervention threshold.

In the broader currency markets this week, Sterling and Euro are currently the strongest currencies, followed by Dollar and Aussie. It is worth noting, however, that these four currencies are still trading within last week’s ranges relative to each other, indicating a lack of decisive strength among them. Swiss Franc is the weakest performer, followed by Yen and Kiwi, with Loonie positioned in the middle.

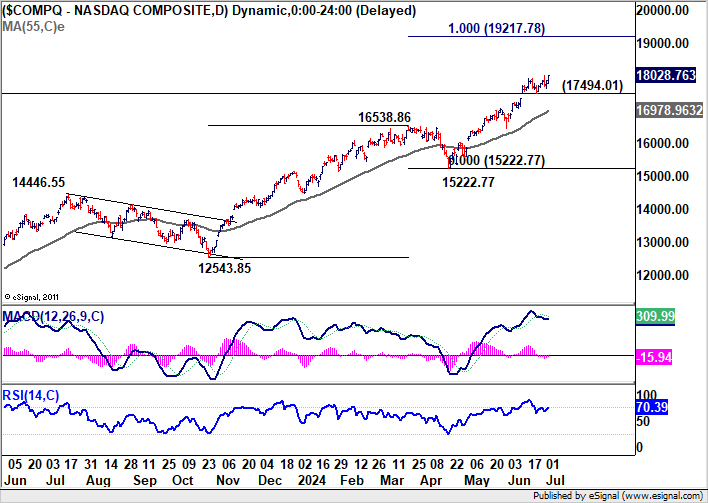

Technically, NASDAQ’s rally resumed overnight and closed at record high above 18k handle. For now, near term outlook will stay bullish as long as 17494.01 support holds. Next target is 100% projection of 12543.85 to 16538.86 from 15222.77 at 19217.78. A key focus for Q3 will be whether this risk-on sentiment, particularly in the tech sector, will persist.

In Asia, at the time of writing, Nikkei is up 1.24%. Hong Kong HSI is up 1.00%. China Shanghai SSE is down -0.41%. Singapore Strait Times is up 1.20%. Japan 10-year JGB yield is up 0.0118 at 1.104. Overnight, DOW rose 0.41%. S&P 500 rose 0.62%. NASDAQ rose 0.84%. 10-year yield fell -0.043 to 4.436.

Australia’s retail sales rises 0.6% mom on sales events boost

Australia’s retail sales turnover increased by 0.6% mom to AUD 35.94B in May, well above expectation of 0.3% mom. On an annual basis, sales grew by 1.5% yoy.

Robert Ewing, ABS head of business statistics, highlighted the influence of early end-of-financial-year promotions and sales events on the boosted turnover.

Despite this seasonally adjusted rise, the underlying trend in spending remains flat. Retail businesses have increasingly relied on discounting and sales events to drive discretionary spending, following several months of restrained consumer activity.

Japan’s PMI services finalized at 49.3, ending 21-month growth streak

Japan’s PMI Services was finalized at 49.4 in June, a significant drop from May’s 53.8, ending a 21-month growth sequence. PMI Composite was finalized at 49.7, down from May’s 52.6, marking the first contraction in seven months.

Trevor Balchin, Economics Director at S&P Global Market Intelligence, highlighted the service sector’s recent strong upturn “ended abruptly”. He noted that the Business Activity Index dropped by -4.4 points during was the largest decline since January 2022 and among the biggest on record.

Despite the concerning headline figures, Balchin pointed out that the underlying details were “less concerning”. The fall in new business was merely a “pause” rather than an “outright decline” in demand. This pause is partly due to the weak yen boosting international new business. Additionally, the 12 month outlook and job growth remained “relatively strong”.

China’s Caixin PMI services drops sharply to 51.2

China’s Caixin PMI Services fell sharply to 51.2 in June, down from 54.0 in May, significantly below expectations of 53.4. This marks the lowest reading since October 2023 but remains in expansionary territory for the 18th consecutive month. PMI Composite also declined from 54.1 to 52.8, signaling an eighth month of expansion.

Wang Zhe, Senior Economist at Caixin Insight Group, stated, “Supply and demand expanded, with the manufacturing sector outperforming services.” He noted that employment at the composite level contracted, while price levels remained stable. However, price levels in the services sector were weaker compared to manufacturing.

“Notably, the gauge for future output expectations recorded a five-year low,” Wang added, indicating weak optimism among both manufacturers and service businesses. This suggests that while current activity remains in growth territory, there are significant concerns about future performance across sectors.

Looking ahead

Eurozone will release PMI services final and PPI in European session while UK will release PMI services final. Later in the day, US will release ADP employment, jobless claims, trade balance, ISM services and factory orders. FOMC minutes will be featured too. Canada will also publish trade balance.

GBP/JPY Daily Outlook

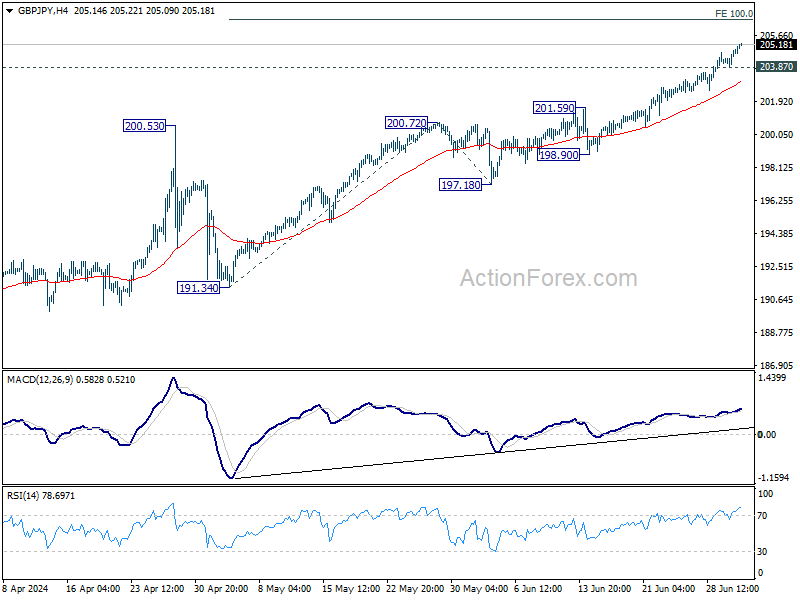

Daily Pivots: (S1) 204.18; (P) 204.53; (R1) 205.17; More…

GBP/JPY’s rally continues today and intraday bias stays on the upside. Current up trend should target 100% projection of 191.34 to 200.72 from 197.18 at 206.56 next. On the downside, below 203.87 minor support will turn intraday bias neutral and bring consolidations. But outlook will remain bullish as long as 201.59 resistance turned support holds, in case of retreat.

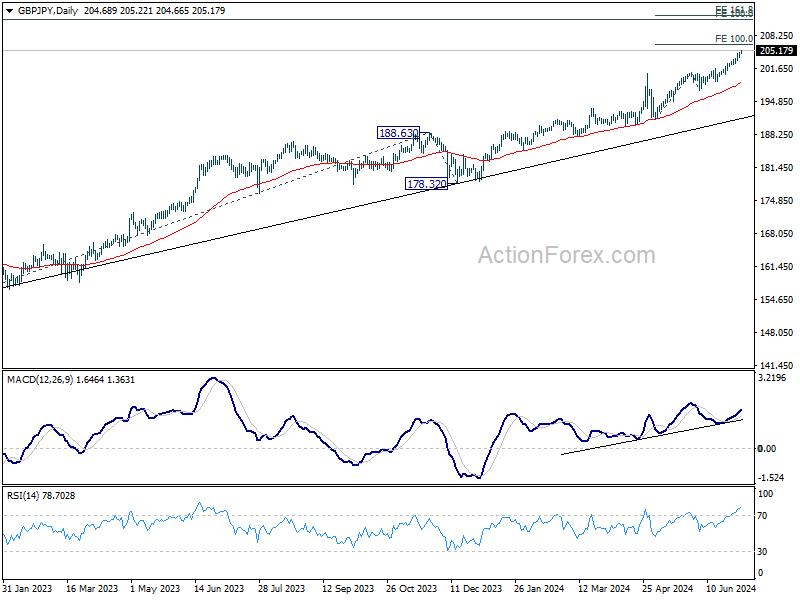

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 197.18 support holds, even in case of deep pullback.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | AUD | Retail Sales M/M May | 0.60% | 0.30% | 0.10% | |

| 01:30 | AUD | Building Permits M/M May | 5.50% | 1.60% | -0.30% | 1.90% |

| 01:45 | CNY | Caixin Services PMI Jun | 51.2 | 53.4 | 54 | |

| 07:45 | EUR | Italy Services PMI Jun | 53.9 | 54.2 | ||

| 07:50 | EUR | France Services PMI Jun F | 48.8 | 48.8 | ||

| 07:55 | EUR | Germany Services PMI Jun F | 53.5 | 53.5 | ||

| 08:00 | EUR | Eurozone Services PMI Jun F | 52.6 | 52.6 | ||

| 08:30 | GBP | Services PMI Jun F | 51.2 | 51.2 | ||

| 09:00 | EUR | Eurozone PPI M/M May | 0.00% | -1.00% | ||

| 09:00 | EUR | Eurozone PPI Y/Y May | -4.10% | -5.70% | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jun | -20.30% | |||

| 12:15 | USD | ADP Employment Change Jun | 158K | 152K | ||

| 12:30 | CAD | Trade Balance (CAD) May | -0.8B | -1.0B | ||

| 12:30 | USD | Trade Balance (USD) May | -76.0B | -74.6B | ||

| 12:30 | USD | Initial Jobless Claims (Jun 28) | 235K | 233K | ||

| 13:45 | USD | Services PMI Jun F | 55.1 | 55.1 | ||

| 14:00 | USD | ISM Services PMI Jun | 52.5 | 53.8 | ||

| 14:00 | USD | Factory Orders M/M May | 0.30% | 0.70% | ||

| 14:30 | USD | Crude Oil Inventories | -0.4M | 3.6M | ||

| 16:00 | USD | Natural Gas Storage | 29B | 52B | ||

| 18:00 | USD | FOMC Minutes |

{kind=link}