{kind=link}

Asian markets were mixed in quiet trade today, with investors holding back ahead of two key events: the ECB policy meeting and U.S. CPI. The lack of conviction reflects a cautious stance, with traders unwilling to take on fresh positions before clarity emerges.

The ECB decision is much less likely to spark volatility, with a steady 2.00% deposit rate firmly priced in. While President Christine Lagarde is not expected to offer firm forward guidance, attention will fall on her tone and the updated projections for clues on whether policymakers view the easing cycle as complete.

By contrast, U.S. CPI carries far greater potential to shake markets, and the risk skew appears asymmetric: a downside surprise could trigger a sharper reaction than an upside print. Any softer-than-expected CPI outcome could extend the dovish repricing on Fed that’s already underway, and quicken the slide in yields and Dollar.

In weekly performance, Aussie remains the strongest G10 currency, followed by Kiwi and Sterling. Loonie is the weakest, trailed by Euro and Swiss Franc, while Dollar and Yen are holding in the middle of the field.

In Asia, at the time of writing, Nikkei is up 0.90%. Hong Kong HSI is down -0.35%. China Shanghai SSE is up 1.04%. Singapore Strait Times is up 0.07%. Japan 10-year JGB yield is up 0.013 at 1.581. Overnight, DOW fell -0.48%. S&P 50 rose 0.30%. NASDAQ rose 0.03%. 10-year yield fell -0.042 to 4.032.

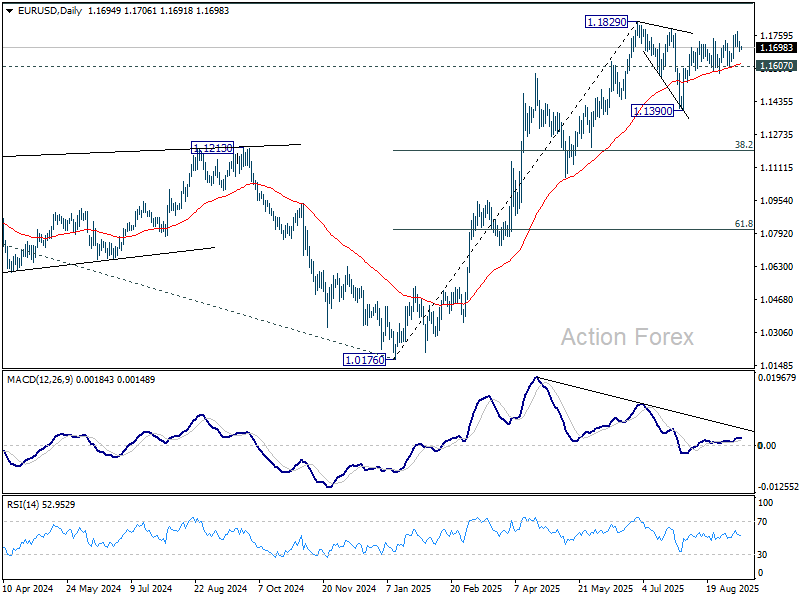

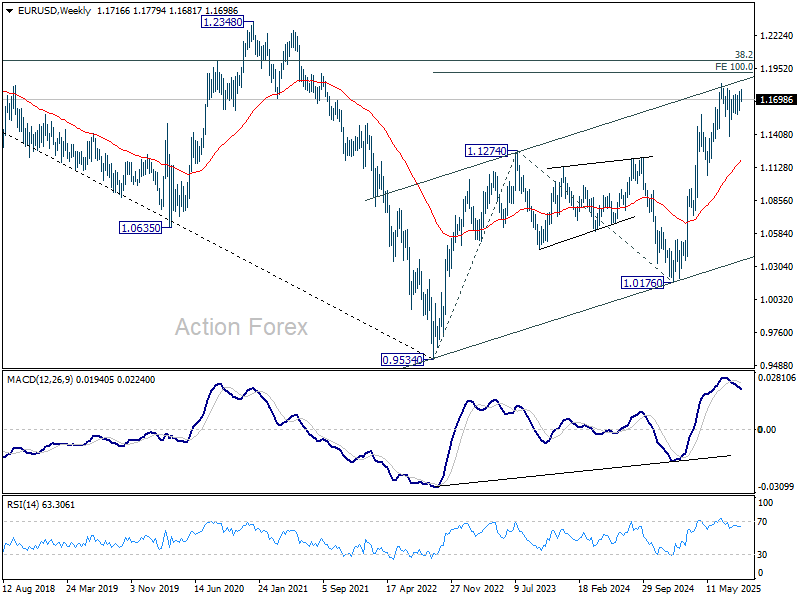

EUR/USD awaits twin catalysts: ECB pause, U.S. CPI test

EUR/USD is holding near its highest levels since 2021 as traders await two pivotal events today: ECB policy decision and U.S. CPI data.

The ECB is set to hold its deposit rate at 2.00%, marking a second consecutive pause. Investors will be listening closely for any hint from President Christine Lagarde that policymakers are ready to park rates for the long haul.

The U.S.-EU trade agreement, which capped tariffs at 15%, has given the central bank more breathing space. If updated projections show limited fallout from tariffs and the Governing Council signals satisfaction with the current stance, Euro could draw support from the perception that the easing cycle is finished.

On the U.S. side, August CPI is expected to show headline inflation rising to 2.9% from 2.7%, with core CPI steady at 3.1%. The report is the final major data input before next week’s FOMC, where markets see a 25bps cut as the base case.

Political noise around the Fed has grown louder. After weaker-than-expected PPI figures yesterday, US President Donald Trump again lashed out at Chair Jerome Powell, calling him a “total disaster” and demanding immediate deep cuts.

Markets currently expect a series of back-to-back 25bps cuts in September, October, and December, bringing rates down to 3.50–3.75% by year-end. A downside surprise in CPI would reinforce that view and might even revive discussion of a larger move in September.

Technically, for EUR/USD, further rise is expected as long as 1.1607 support holds. Firm break of 1.1829 will resume larger up trend to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. Then EUR/USD will face the real test at 1.2 psychological level.

Meanwhile, break of 1.1607 will delay the bullish case, and extend the corrective pattern from 1.1829 with another dip back towards 1.1390 support in the near term.

Japan CGPI accelerates to 2.7% yoy, import price declines ease

Japan’s producer prices rose modestly in August, with CGPI climbing 2.7% yoy from 2.5% yoy in July, matching market forecasts. The pickup was driven mainly by food and beverage costs, which rose 5.0% yoy versus 4.7% yoy previously. In contrast, utility bills fell -2.9% yoy due to government subsidies, softening the overall inflation impact.

Import price declines eased significantly in the past two months, with yen-based import prices down -3.9% yoy compared with a revised -10.3% fall in July. The data suggest external cost pressures are stabilizing, even as domestic food inflation remains sticky.

RBNZ’s Hawkesby: OCR seen at 2.5% by year-end, data dependent

RBNZ Governor Christian Hawkesby said today the central bank still projects the Official Cash Rate to fall to around 2.50% by year-end, down from current 3.00%. Though, the pace could be “faster or slower” depending on incoming data. He emphasized that the path of policy easing will hinge on the “speed of New Zealand’s economic recovery”.

Hawkesby noted the August Monetary Policy Statement highlighted the sharp blow to household and business confidence, with the economy stalling mid-year and creating more slack. He attributed much of the “confidence shock” to uncertainty over U.S. tariff policies, compounded by cost-of-living pressures and a weak housing market.

Still, leading indicators for July were “better” and aligned with the RBNZ’s outlook for a rebound in the second half of the year. Hawkesby said policymakers will keep monitoring spillovers from U.S. tariffs on both global growth and New Zealand firms. The RBNZ resumed rate cuts last month after a July pause.

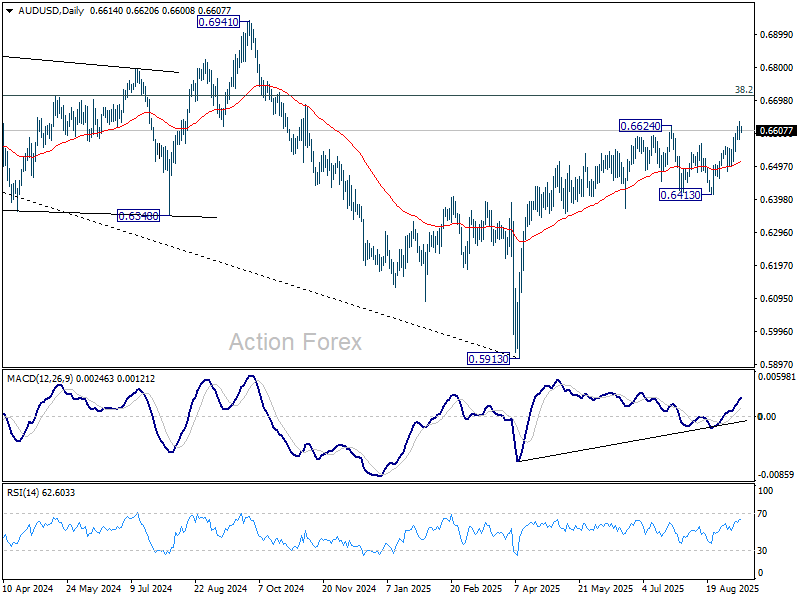

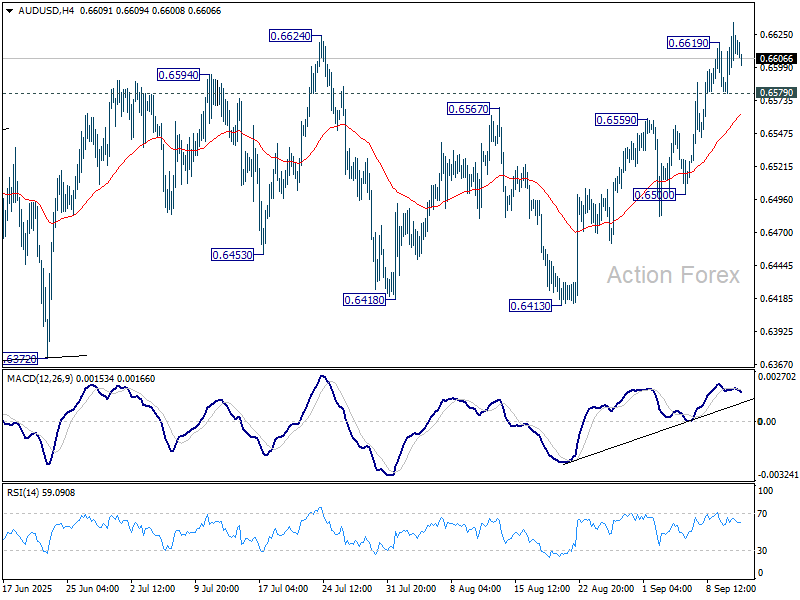

AUD/USD Daily Report

Daily Pivots: (S1) 0.6583; (P) 0.6610; (R1) 0.6639; More...

AUD/USD’s rally resumed after brief consolidations and intraday bias is back on the upside. The break of 0.6624 resistance indicates that larger rally from 0.5913 is resuming. Further rise should be seen to 0.6713 fibonacci level. On the downside, through, below 0.6579 minor support will turn intraday bias neutral again.

In the bigger picture, there is no clear sign that down trend from 0.8006 (2021 high) has completed. Rebound from 0.5913 is seen as a corrective move. While stronger rally cannot be ruled out, outlook will remain bearish as long as 38.2% retracement of 0.8006 to 0.5913 at 0.6713 holds. Nevertheless, considering bullish convergence condition in W MACD, even in case of another fall through 0.5913, downside should be contained above 0.5506 (2020 low).