Trading was relatively subdued in Asia today, with China and Hong Kong closed for holidays and little reaction seen across the rest of the region. Equity markets were mixed, reflecting a cautious tone after Wall Street managed to end slightly higher overnight despite a fresh government shutdown in the US.

Gold edged to another record high but with far less momentum than in recent sessions. The lack of follow-through reflects both subdued regional liquidity and some restraint among investors, who are weighing the potential fallout of the US fiscal standoff.

The US government formally shut down much of its operations on Wednesday after President Donald Trump and Congressional leaders failed to agree on a short-term funding deal through November 21. This marks the 15th shutdown since 1981, though markets typically treat such events as temporary and relatively immaterial.

This episode, however, carries additional risk. Trump suggested his administration could use the shutdown to push broader policy actions, including cuts to government benefits for “large numbers of people.” That raises the possibility of a mini-labor market shock, which markets cannot entirely dismiss.

Currency markets were livelier, with Yen leading gains for the week. Today’s Tankan survey signaled resilience in large manufacturers despite tariff headwinds, lending credibility to speculation that the BoJ will resume rate hikes later this year.

Aussie was the next strongest, though it is consolidating after sharp gains earlier this week. Reports around China’s state-run iron ore buyer CMRG briefly unsettled markets, with Bloomberg suggesting it had instructed steelmakers to halt new purchases from BHP. But Mysteel disputed the claims, calling the report “not true,” leaving traders uncertain.

At the bottom, Dollar is currently the weakest performer, though still above last week’s lows. Loonie was the next weakest, while European majors and the Kiwi held mid-pack.

In Asia, at the time of writing, Nikkei is down -0.92%. Hong Kong and China are on holiday. Singapore Strait Times is up 0.63%. Japan 10-year JGB yield is down -0.003 at 1.648. Overnight, DOW rose 0.18%. S&P 500 rose 0.41%. NASDAQ rose 0.30%. 10-year yield rose 0.007 to 4.418.

Japan’s Tankan shows resilience, supports BoJ tightening outlook

Japan’s Q3 Tankan survey showed large manufacturers growing more confident, with the index rising from 13 to 14, in line with expectations and the highest since Q4 2024. While the manufacturing outlook held steady at 12, suggesting some softening ahead, sentiment remains resilient despite trade headwinds.

Non-manufacturing confidence also stayed firm, with the index unchanged at 34, beating forecasts, and the outlook improving to 28 from 27.

Large firms signaled robust investment plans, projecting a 12.5% increase in capital expenditure for the fiscal year to March 2026, up from June’s forecast of 11.5%.

The results suggest Japan’s economy is weathering tariff pressures and steady domestic demand continues to support activity. For the Bank of Japan, the data bolster expectations that further tightening is coming — the debate is less about if and more about when policymakers will move.

Japan PMI manufacturing finalized at 48.5, weak demand from China and US

Japan’s manufacturing sector contracted further in September, with the PMI finalized at 48.5, down from August’s 49.7. S&P Global’s Annabel Fiddes said the sector ended Q3 “on a weaker note,” as output and new orders declined at a faster pace, driven by softer demand across key markets such as China and the drag from US tariffs.

Weaker demand weighed on business confidence, leading firms to scale back activity. Employment expanded at the slowest pace since February, while purchasing activity dropped at the second-steepest rate since early 2024. The cautious stance underscores concern that the sector may “struggle to see much growth in the near term.”

Price dynamics offered some relief, with cost pressures “less pronounced” than earlier in the year. Still, selling prices rose at a “historically strong pace” as firms sought to protect margins.

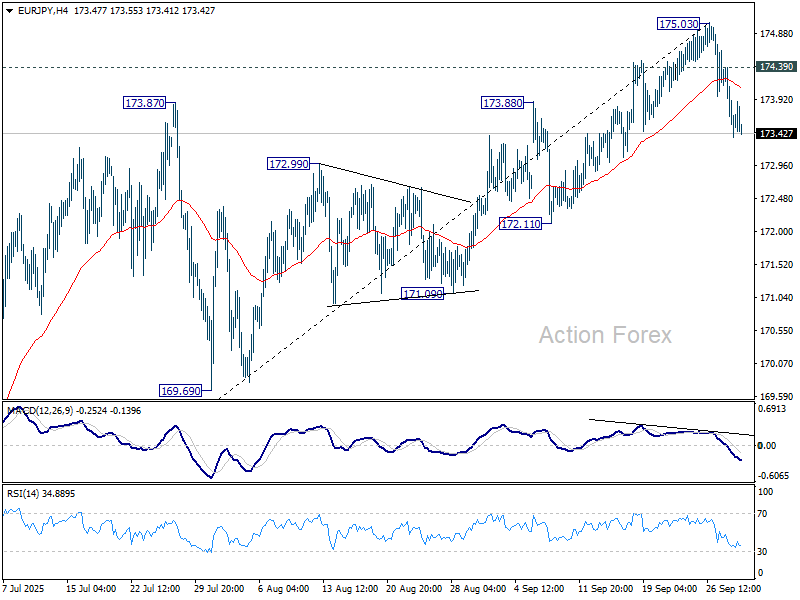

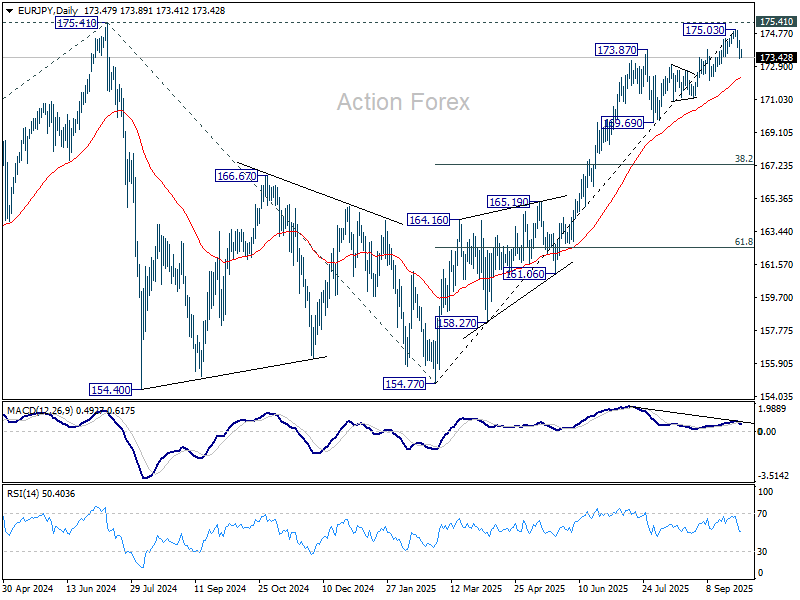

EUR/JPY Daily Outlook

Daily Pivots: (S1) 173.17; (P) 173.80; (R1) 174.20; More…

Intraday bias in EUR/JPY stays on the downside for the moment. Fall from 175.03 short term bottom is in progress for 55 D EMA (now at 172.24). Sustained break there will argue that whole five-wave rally from 154.77 has also completed. On the upside, above 174.39 will turn bias neutral first. But risk will stay on the downside as long as 175.03 resistance holds, in case of recovery.

In the bigger picture, current rally from 154.77 is still tentatively seen as resuming the larger up trend. Firm break of 175.41 (2024 high) will confirm and target 61.8% projection of 124.37 (2022 low) to 175.41 from 154.77 (2025 low) at 186.31. However, sustained break of 55 D EMA will delay this bullish case, bring deeper pullback to 169.69 support first.

{kind=link}