{kind=link}

Dollar came under renewed selling pressure today after a sharp upside surprise in US weekly jobless claims. The surge in initial claims reminded investors that last week’s notably low reading was likely a statistical outlier rather than a sign of renewed labor-market strength. While the data does not yet move the needle on the probability of a Fed cut in Q1, it does inject an additional caution into assessments of the US economy’s momentum.

For now, futures pricing still shows little urgency for a Q1 move, but confidence in the labor market’s resilience has diminished. The narrative of a “soft landing” remains intact, but today’s figures point to less optimism around hiring conditions as the economy enters year-end.

In contrast, Swiss Franc extended its near-term rebound after SNB kept interest rates unchanged at 0.00%, as widely expected. The statement carried a slightly more positive tone, with the central bank noting that the recent US–Swiss tariff agreement—cutting tariff rates retroactively—had improved Switzerland’s growth outlook.

More importantly, SNB downplayed near-term inflation miss and stressed that medium-term inflation dynamics are “virtually unchanged.” The forecast path remains comfortably within price stability. This stance reduces the likelihood of any return to negative interest rates, at least for now, giving CHF modest support.

Market sentiment, however, turned more cautious as the US session began. The strong post-FOMC equity rally looks exhausted, dragged lower by a heavy selloff in Oracle. The firm’s disappointing results and guidance rattled broader tech sentiment, snapping investors back to concerns about stretched AI-related valuations.

Oracle has long sat at the center of the debate over AI-capex sustainability. Unlike Google, Amazon, and Microsoft, the company lacks the deep cash flows required to support ballooning infrastructure and compute investments. Markets were quick to brush aside the headline earnings beat—which was driven by a one-off asset sale—and instead focused on rising capex and weaker free cash flow.

The result: renewed worries that AI investment is not translating into profits as quickly as optimists hoped. The broader tech complex weakened in sympathy, raising the risk that Wednesday’s FOMC-driven stock surge proves short-lived.

In FX for the week so far, Dollar is the worst performer as it extends its post-FOMC decline. Yen follows as second-weakest, with Loonie in third. At the top end, Swiss Franc is the strongest, followed by Kiwi and then Euro. Sterling and Aussie sit in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.08%. DAX is up 0.27%. CAC is up 0.55%. UK 10-year yield is down -0.029 at 4.480. Germany 10-year yield is down -0.002 at 2.853. Earlier in Asia, Nikkei fell -0.90%. Hong Kong HSI fell -0.04%. China Shanghai SSE fell -0.70%. Singapore Strait Times rose 0.20. Japan 10-year JGB yield fell -0.033 to 1.931.

US initial jobless claims jump back to 236k

US initial jobless claims rose 44k to 236k in the week ending December 6, above expectation of 205k. Four-week moving average of initial claims rose 2k to 217k. Continuing claims fell -99k to 1838k in the week ending November 29. Four-week moving average of continuing claims fell -17k to 1918k.

SNB holds at 0.00%, medium term inflation outlook virtually unchanged.

SNB left its policy rate unchanged at 0.00%, as widely expected, and reiterated its readiness to intervene in foreign exchange markets if necessary. The hold reflects the bank’s assessment that current conditions do not justify a shift, even as inflation undershot expectations.

In its statement, the SNB noted that inflation has been slightly weaker than anticipated in recent months, but emphasized that medium-term pressures are “virtually unchanged” compared with September. The conditional inflation forecast is marginally lower in the near term but shows little change beyond that. The Bank now sees inflation averaging 0.2% in 2025, 0.3% in 2026 and 0.6% in 2027, based on the assumption of a 0% policy rate throughout the forecast horizon.

The economic outlook for Switzerland has “improved slightly”, helped by reduced U.S. tariffs and a modestly better global backdrop. SNB now expects GDP to grow just under 1.5% in 2025 and around 1% in 2026, though it cautioned that unemployment is likely to edge higher.

Australia jobs shock as employment drops -21.3k in November

Australia’s November labor data delivered a downside surprise, with employment falling by -21.3k against expectations for a 20k increase. The weakness was driven by a sharp -56.5k drop in full-time positions, partly offset by a 35.2k rise in part-time roles.

Despite the weaker headline, unemployment rate held at 4.3%, better than the expected uptick to 4.4%. The jobless rate has now been steady at 4.3% in five of the past six months, reflecting a labor market that is loosening but not deteriorating sharply. Participation rate dipped -0.2pts to 66.7%, suggesting some softening in labor-force engagement.

Monthly hours worked were unchanged on the month but still up 1.2% yoy, indicating modest resilience in total labor input despite weaker job creation.

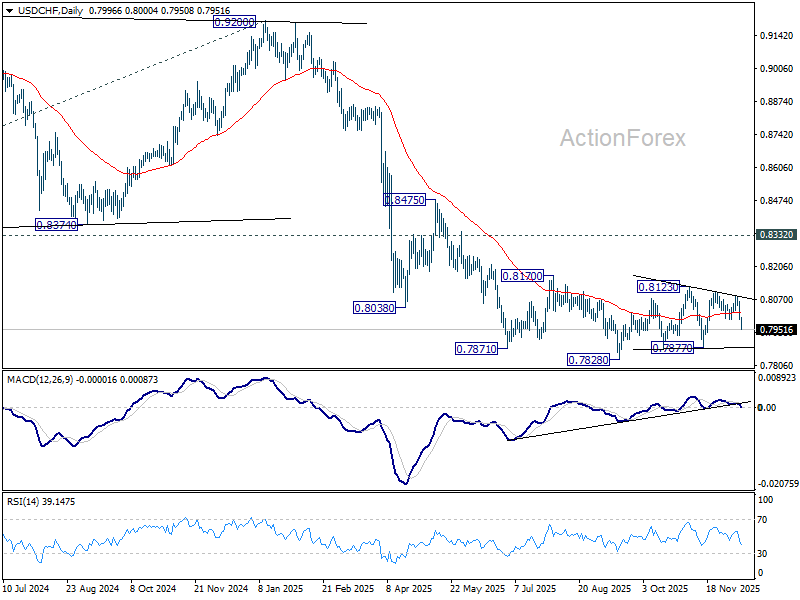

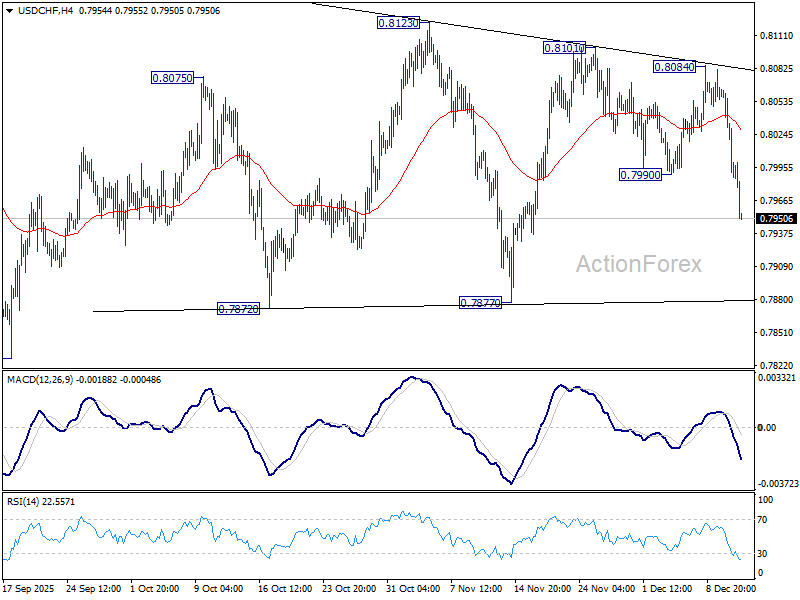

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7970; (P) 0.8022; (R1) 0.8053; More…

USD/CHF’s fall from 0.8101 resumes through 0.7990 and intraday bias is back on the downside. Further fall should be seen to 0.7877 support. Overall, price actions from 0.7828 are seen as a corrective pattern and might extend. Nevertheless, firm break of 0.7877 will argue that larger down trend might be ready to resume through 0.7828 low.

In the bigger picture, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low). Long term down trend from 1.0342 (2017 high) is still in progress. Next target is 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382.