{kind=link}

Sterling rallied broadly after the BoE delivered a widely expected rate cut that came with a distinctly hawkish undertone. The 5–4 vote, with four members dissenting in favor of holding rates steady, was a surprise and prompted a reassessment of how smooth the easing path ahead will be.

Fundamentally, the BoE still sees scope for further easing. However, policymakers were explicit that any additional cuts would now be a much “closer call”. That caution and the tight voting are striking given this week’s downside surprises in both UK employment and inflation. Despite the softer data, the MPC remains deeply divided.

February remains the most likely window for a follow-up cut, particularly with new economic projections due. Still, conviction has clearly faded, and markets are no longer confident that the BoE will simply return to a predictable quarterly easing rhythm.

By contrast, Dollar came under renewed pressure after US CPI undershot expectations. The weaker inflation print prompted a swift repricing of Fed expectations, with markets lifting the probability of a March rate cut to around 60%.

Even so, Dollar downside may not be linear. With risk sentiment fragile, further losses will likely depend on how equities behave through the rest of the session rather than on rate expectations alone. At the time of writing, US futures—particularly NASDAQ—are pointing to a rebound at the open. That recovery, however, remains tentative and vulnerable to reversal.

Looking ahead to Asia, attention turns to the BoJ, which is widely expected to raise rates by 25bps to 0.75%. That would mark the highest policy rate in 30 years, the first hike since January, and the first under Prime Minister Sanae Takaichi. The case for the move rests on persistently elevated core inflation and easing uncertainty tied to US tariffs, as confirmed by recent Tankan data. Political resistance to tightening has also softened.

Still, further tightening is far from assured. The BoJ is likely to wait for clearer evidence of sustained wage growth into 2026, with January’s economic projections set to shape expectations for what comes next.

In Europe, at the time of writing, FTSE is down -0.22%. DAX is up 0.40%. CAC is up 0.27%. UK 10-year yield is up 0.026 at 4.513. Germany 10-year yield is up 0.031 at 2.899. Earlier in Asia, Nikkei fell -1.03%. Hong Kong HSI rose 0.12%. China Shanghai SSE rose 0.16%. Singapore Strait Times fell -0.11%. Japan 10-year JGB yield fell -0.019 to 1.966.

US CPI slows sharply to 3.7% in November, core down to 2.6%

US inflation slowed more than expected in November, with the data compared against September levels due to the absence of October figures following the government shutdown.

Headline CPI eased from 3.0% yoy to 2.7%, undershooting expectations for a pickup to 3.1%. Core CPI also surprised to the downside, slowing from 3.0% yoy to 2.6% , well below forecasts for no change at 3.0%.

The broad-based moderation reinforces the view that underlying inflation pressures are easing faster than previously anticipated. Within the components, energy prices rose 4.2% yoy, while food prices increased 2.6% yoy.

US initial jobless claims fall back to 224k, match expectations

US initial jobless claims fell -13k to 224k in the week ending December 13, matched expectations. Four-week moving average of initial claims rose 500k to 217.5k.

Continuing claims rose 67k to 1897k in the week ending December 6. Four-week moving average of continuing claims fell -14k to 1902.

ECB holds rates, forecasts reinforce inflation convergence around target

The ECB left its deposit rate unchanged at 2.00%, in line with expectations, signaling continued confidence that current policy settings remain appropriate. With inflation broadly converging around target and growth improving, policymakers saw no need to adjust rates at this stage.

Updated Eurosystem staff projections show headline inflation averaging 2.1% in 2025, easing to 1.9% in 2026 and 1.8% in 2027, before returning to 2.0% in 2028. Core inflation excluding energy and food is projected at 2.4% in 2025, 2.2% in 2026, 1.9% in 2027 and 2.0% in 2028.

The inflation outlook for 2026 was revised higher, mainly reflecting expectations that services inflation will decline more slowly than previously anticipated.

On growth, projections were revised higher across the forecast horizon. GDP is now expected to expand by 1.4% in 2025, 1.2% in 2026 and 1.4% in 2027, with growth holding at 1.4% in 2028. The improvement is driven primarily by stronger domestic demand.

BoE cuts to 3.75% with hawkish vote, future easing a closer call

The BoE delivered a widely expected 25bps rate cut, taking Bank Rate to 3.75%. However, the decision was accompanied by a surprisingly hawkish 5–4 vote split.

Supporters of the cut, led by Governor Andrew Bailey (with Sarah Breeden, Swati Dhingra, Dave Ramsden and Alan Taylor), argued that disinflation remains broadly on course. Some members emphasized that “upside risks to inflation had continued to recede”. Others focused on weakening activity and downside inflation risks.

In contrast, four members (Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted to hold rates steady, expressing concern on “prolonged inflation persistence”. They highlighted elevated services inflation, wage growth, and inflation expectations. These members are “not convinced that the monetary policy stance was meaningfully restrictive” That main require a more “prolonged period of policy restriction”.

Overall, while reaffirming that Bank Rate is likely to continue on a “gradual downward path”, it stressed that further easing decisions will become a “closer call”.

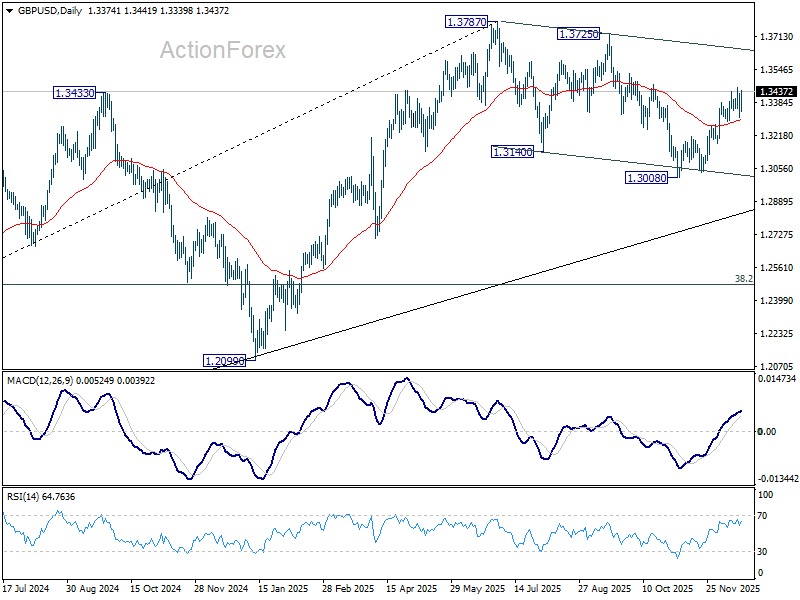

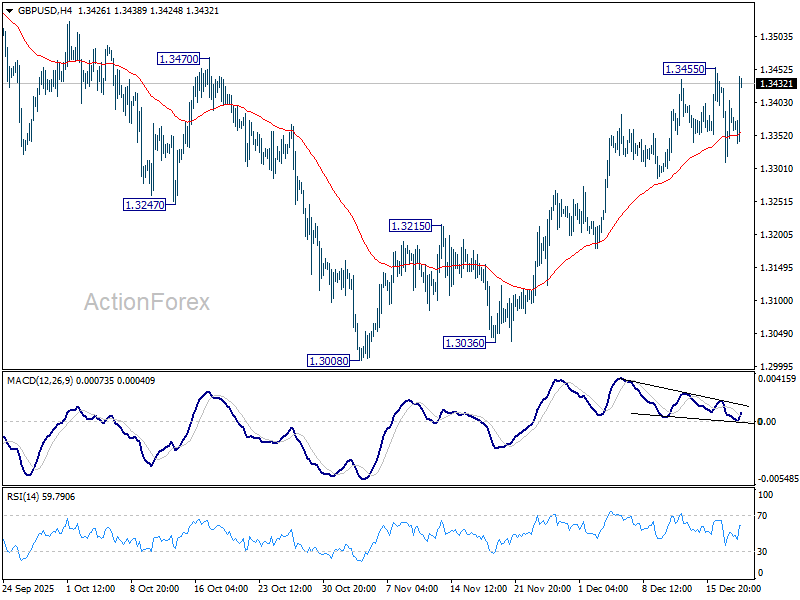

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3315; (P) 1.3372; (R1) 1.3431; More…

GBP/USD rebounds notably but stays below 1.3455 temporary top. Intraday bias remains neutral at this point. On the upside, above 1.3455 will resume the rebound from 1.3008. Firm break of 1.3470 resistance will pave the way to retest 1.3787 high. However, sustained break of 55 D EMA (now at 1.3295) will argue that the rebound has completed. Deeper fall would be seen back to 1.3008 support to resume the whole corrective pattern from 1.3787 high.

In the bigger picture, current development suggests that fall from 1.3787 is merely a corrective move, and larger rise from 1.0351 (2022 low) is still in progress. Firm break of 1.3787 will target 1.4248 (2021 high) key structural resistance. This will remain the favored case as long as target 38.2% retracement of 1.0351 to 1.3787 at 1.2474 holds, in case of another fall.