{kind=link}

Global markets opened the final full trading week of 2025 on a mixed footing, with price action shaped more by thin holiday liquidity than fresh conviction. Asian equities leaned modestly higher, led by a strong surge in Japanese stocks after Friday’s firm close in the U.S., where technology shares again drove gains. Elsewhere in the region, equities also firmed, but advances were far more restrained, reflecting limited follow-through rather than renewed risk appetite.

The real focus has shifted decisively toward precious metals. Gold and Silver both pushed to new record highs, pulling attention away from equities and currencies alike. With positioning light and liquidity thin, the outsized moves in metals are more of a function of defensive demand amplified by year-end conditions.

That broader theme is visible across markets. Volatility remains elevated in pockets, but without the kind of cross-asset confirmation typically associated with durable trends. This pattern is likely to persist through the remainder of the year, with more meaningful repricing deferred until liquidity normalizes in early 2026.

In FX markets, Yen is attempting to stabilize against Dollar after a sharp selloff, but the effort remains tentative. There is little evidence of broad-based support for the currency, and gains have failed to spill over into crosses.

Japanese officials have stepped up verbal intervention, warning against rapid and one-sided currency moves. Top currency diplomat Atsushi Mimura said authorities were concerned and ready to take “appropriate actions” against excessive moves, while Chief Cabinet Secretary Minoru Kihara echoed concerns about speculative pressure and stressed the need for stability reflecting fundamentals.

Despite the firmer rhetoric, markets remain unconvinced. The key test will be whether Tokyo delivers concrete measures if USD/JPY pushes higher again and approaches the 160 area, or whether officials continue to rely solely on verbal warnings.

For now, Kiwi is the strongest currency on the day, followed by Aussie and Sterling. Dollar sits at the bottom of the table, trailed by Swiss Franc and Loonie, while Euro and Yen are holding middle ground amid the broader holiday drift.

In Asia, Nikkei rose 1.81%. Hong Kong HSI rose 0.43%. China Shanghai SSE rose 0.69%. Singapore Strait Times is up 0.68%. Japan 10-year JGB yield rose 0.058 to 2.082.

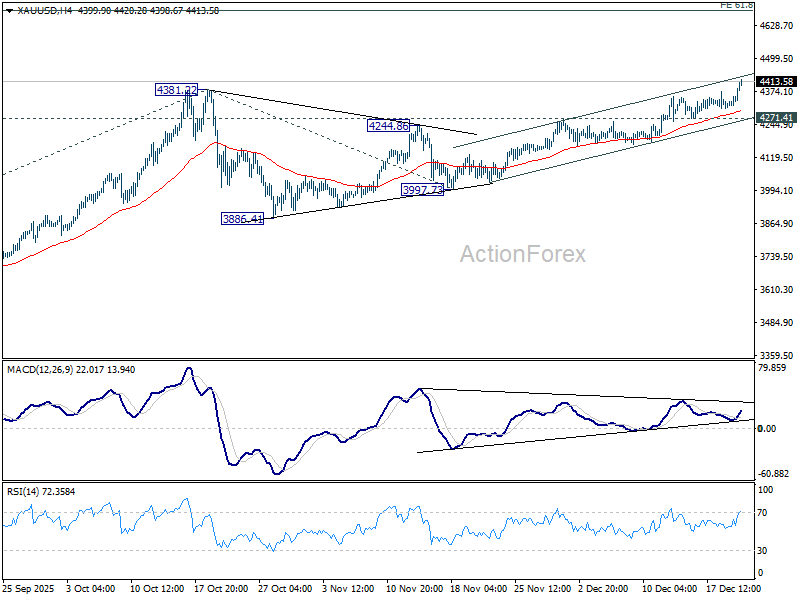

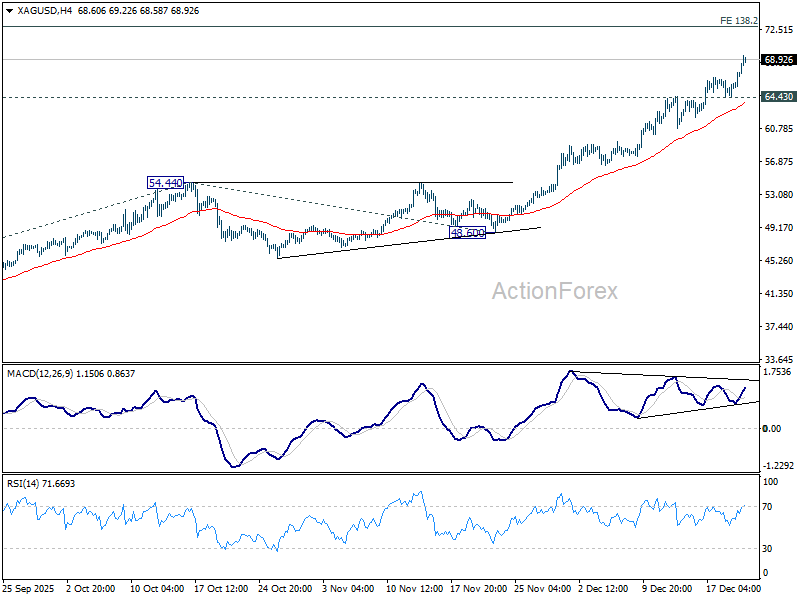

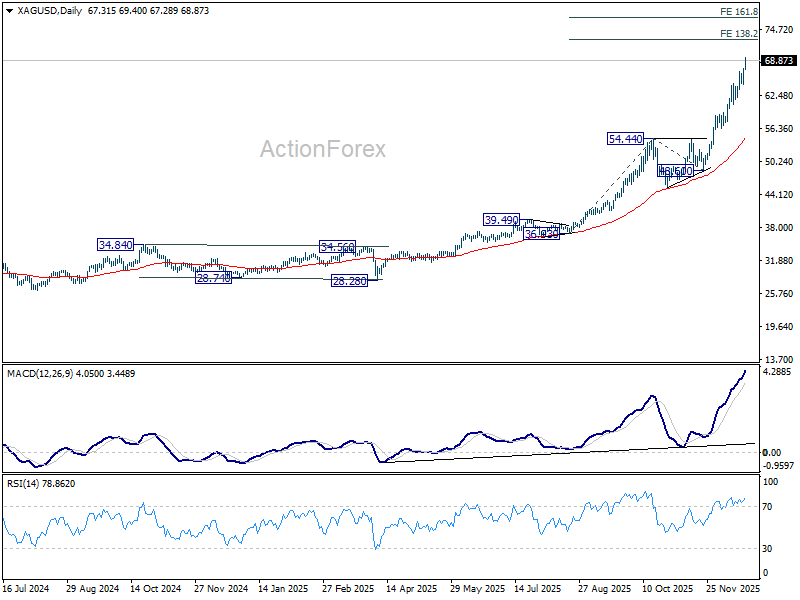

Gold breaks above 4,400 as geopolitics ignite late-year surge, Silver nears 70

Gold surged to a fresh record high above 4,400 today, finally breaking out after weeks of subdued momentum. Though, Silver is still taking the lead, extending its powerful rally toward the psychologically important 70 level.

Thin holiday trading conditions amplified the reaction, but the underlying driver is a sharp escalation in geopolitical risk. Safe-haven demand accelerated after US President Donald Trump and senior aides refused to rule out military conflict with Venezuela, jolting markets that had largely discounted further escalation in Latin America.

Washington is now intensifying pressure on Venezuelan oil exports, tightening what traders increasingly see as a de facto blockade. Multiple vessels have reportedly been seized off Venezuela’s coast in international waters, with another currently being pursued. The move adds further strain on the government of Nicolás Maduro, heightening fears of miscalculation and retaliation.

At the same time, optimism around a diplomatic breakthrough in Ukraine fades. Markets are reassessing the likelihood of a durable ceasefire as negotiations drag on without tangible progress. Comments over the weekend suggested talks remain focused on aligning positions rather than finalizing concrete outcomes, reinforcing skepticism over near-term resolution of Russia’s war in Ukraine.

Against that backdrop, Gold’s technical breakout arrived earlier than expected. The decisive break above 4,381.22 suggests that consolidation from that peak had already completed at 3,997.73. Near-term outlook will stay firmly bullish as long as 4,271.41 holds as support on any pullback.

Attention is now on whether price can push cleanly through the rising channel ceiling, a move that would signal further upside acceleration. If that ceiling gives way, the next target comes in at the 61.8% projection of the 3,267.90 to 4,381.22 advance from 3,997.73 at 4,685.76.

As for Silver, outlook will remain bullish as long as 64.43 support holds. 4H MACD suggests that it’s likely now in an upside re-acceleration phase. Next target is 138.2% projection of 36.93 to 54.44 from 48.50 at 72.68. Break there will target 161.8% projection 76.83.

China holds lending rates, leans on fiscal push for growth

China kept benchmark loan prime rates unchanged for a seventh consecutive month, in line with expectations. The one-year loan prime rate was held at 3.0%, while the over-five-year LPR, a key reference for mortgage pricing, remained at 3.5%.

The decision reinforces the view that near-term monetary easing is not a priority. While lower LPRs would help reduce financing costs and support investment and consumption, authorities appear comfortable maintaining current settings as they assess the impact of earlier stimulus and targeted support measures across the economy.

Nevertheless, policy guidance from the Central Economic Work Conference earlier points to a broader strategic tilt. Officials signaled that China will pursue a more proactive fiscal stance alongside a moderately loose monetary policy in 2026, suggesting growth support will increasingly come from government spending and structural measures rather than immediate rate cuts.

Fed’s Hammack downplays CPI drop, backs steady rates into Spring

In an interview with Beth Hammack published by the Wall Street Journal, the Cleveland Fed president argued there was no urgency for the Fed to adjust interest rates, saying policy could remain unchanged at 3.50–3.75% at least until Spring. Hammack said that timeframe would allow policymakers to better judge whether goods price inflation is truly easing as tariffs work their way through supply chains.

Hammack framed her outlook around patience rather than reaction. Her base case is for rates to stay at current levels “for some period of time”, until there is clearer evidence that “either inflation is coming back down to target or the employment side is weakening more materially.”

She was notably skeptical of last week’s November CPI report, which showed a sharp drop in headline inflation to 2.7% from 3.1%, with a similar decline in core inflation. Hammack said she takes the data “with a grain of salt,” pointing to distortions linked to Autumn’s government shutdown. Her own estimates place inflation closer to 2.9–3.0%.

While describing the current policy rate as roughly neutral, Hammack signaled she would actually prefer a slightly more restrictive stance to apply additional pressure on inflation.

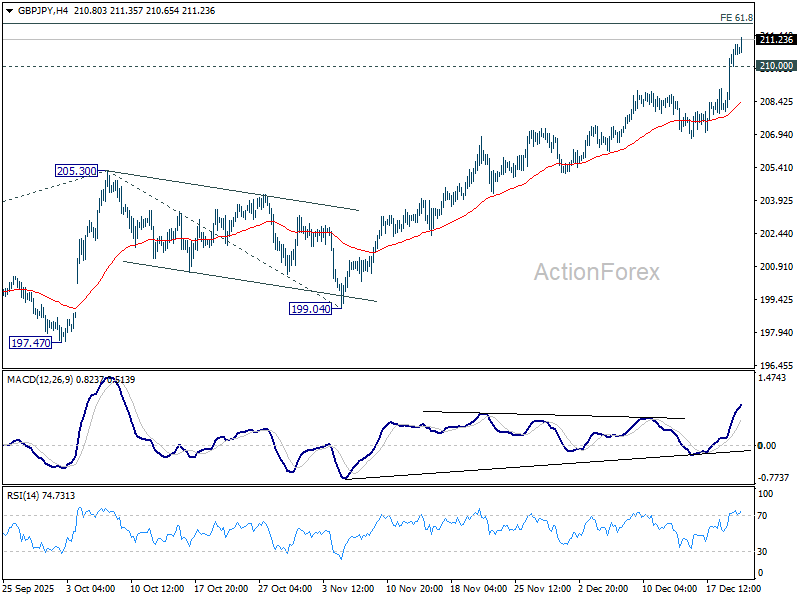

GBP/JPY Daily Outlook

Daily Pivots: (S1) 208.94; (P) 210.01; (R1) 212.03; More…

Intraday bias in GBP/JPY remains on the upside for 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98. Firm break there will extend current up trend to 100% projection at 219.99 next. On the downside, below 210.00 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 199.04 support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.