Initial reactions show markets are not too happy with US non-farm payroll report. While headline job growth beat expectation, it was partly offset by downward revision in prior month’s figure. More importantly, wage growth came in weaker than expected. It’s seen as a crucial factor for inflationary pressure, or the lack thereof. While the greenback retreats mildly as knee jerk reaction, there is no sign of a reversal. Instead, the greenback stays very strong against Euro and Swiss Franc. 1.1712 in EUR/USD is now at risk and break will probably trigger broad based acceleration in Dollar. Meanwhile, Sterling reversed earlier gains as Brexit negotiation breakthrough finally becomes a fact today.

Non-farm payroll report showed 228k growth in jobs in November, above expectation of 200k. Prior month’s figure was revised down to 244k, from 261k. Unemployment rate was unchanged at 4.1% as expected. However, average hourly earnings rose 0.2% mom only, below expectation of 0.3% mom.

Also release in US session, Canada housing starts rose to 252.2k in November. Capacity utilization rate was unchanged at 85% in Q3.

Brexit: Sufficient progress finally made to move on to trade talks

Brexit negotiations between UK and EU have finally made the break through o move on to trade agreements. European Commission President Jean-Claude Juncker declared after meeting UK Prime Minister Theresa May that "sufficient progress has now been made on the three terms of the divorce." May said that "getting to this point required give and take on both sides." A joint report was published detailing the agreements. In short:

- Divorce bill: UK agreed to contribute to EU budget up the end of 2020 "as if it had remained in the union". And UK will be liable for its commitments and liabilities up to December 3, 2020. No hard figure was given but according to the framework, the net payment should be around GBP 40b.

- EU citizen rights in UK: EU citizens in UK will continue to have the rights to live, work and study after Brexit. UK court will enforce the rights in concession to EU. And, the European Court of Justice will continue to have a role in overseeing the rights for eight years. On the other hand, guarantees will also apply to UK citizens living in EU.

- Irish border: The report noted that "in the absence of agreed solutions, as set out in the previous paragraph, the United Kingdom will ensure that no new regulatory barriers develop between Northern Ireland and the rest of the United Kingdom, unless, consistent with the 1998 Agreement, the Northern Ireland Executive and Assembly agree that distinct arrangements are appropriate for Northern Ireland." But both EU and UK will "establish mechanisms to ensure the implementation and oversight of any specific arrangement to safeguard the integrity of the EU Internal Market and the Customs Union."

Released from UK, industrial production rose 0.0% mom, 3.6% yoy in October. Manufacturing production rose 0.1% mom, 3.9% yoy. Construction output dropped -1.7% mom. Visible trade deficit narrowed to GBP -10.8b in October. NIESR GDP estimate rose 0.5% in November. From Eurozone, German trade surplus narrowed to EUR 19.9b in October.

Japan GDP grew 0.6% qoq in Q3, doubled initial estimate

Japan GDP growth was finalized at 0.6% qoq in Q3, double the pace of initial estimate of 0.3% qoq. Annualized rate was 2.5%. GDP deflator was finalized at 0.1% yoy, unchanged. The data showed that Abenomics and BoJ’s easing have definite boosted growth, but is so far having little impact on lifting inflation. Also from Japan current account surplus widened to JPY 2.44T in October. Labor cash earnings rose 0.6% yoy, below expectation of 0.8% yoy.

China trade surplus widened to USD 40.2b in November, up from USD 38.2b and above expectation of USD 34.9b.Exports rose 12.3% yoy while imports also surged 18% yoy. In Yuan, trade surplus widened to CNY 264b, up fro CNY 254b and beat expectation of CNY 238b. Also from Asia Pacific, Australia home loans dropped -0.6% mom in October. New Zealand manufacturing activity rose 0.5% in Q3.

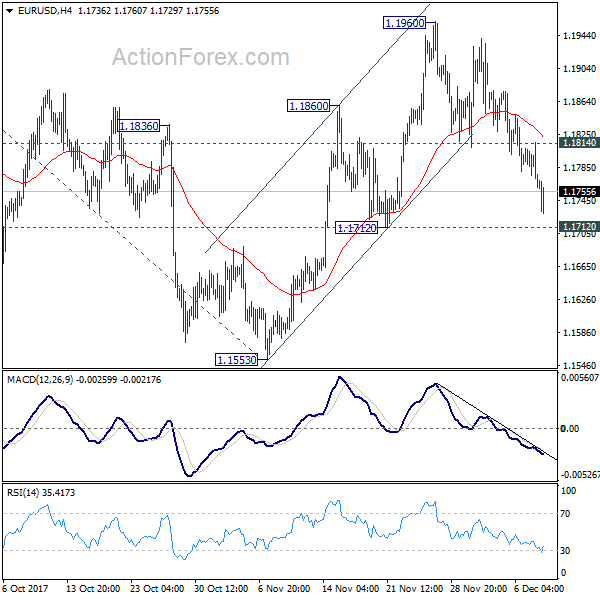

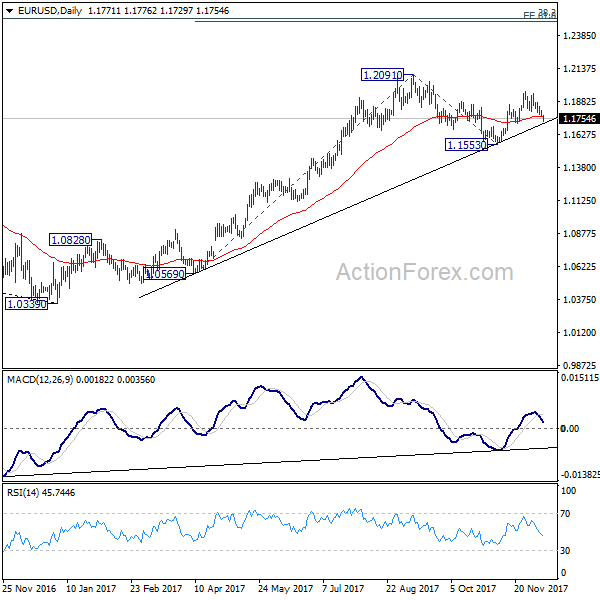

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1757; (P) 1.1786 (R1) 1.1800; More….

EUR/USD drops to as low as 1.1729 so far today and focus in now on 1.1712 near term support. Decisive break there will indicate that rebound from 1.1553 has completed at 1.1960. In that case, deeper fall would be seen to retest 1.1553 low. Meanwhile, with 1.1712 support intact, break of 1.1814 will retain near term bullishness. And in that case, intraday bias will be turned back to the upside for 1.1960. Break will target 1.2091 high.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we’d be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1393) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Manufacturing Activity Q3 | 0.50% | 3.90% | 3.40% | |

| 23:50 | JPY | Current Account (JPY) Oct | 2.44T | 1.93T | 1.84T | |

| 23:50 | JPY | GDP Q/Q Q3 F | 0.60% | 0.40% | 0.30% | |

| 23:50 | JPY | GDP Deflator Y/Y Q3 F | 0.10% | 0.10% | 0.10% | |

| 00:00 | JPY | Labor Cash Earnings Y/Y Oct | 0.60% | 0.80% | 0.90% | |

| 00:30 | AUD | Home Loans M/M Oct | -0.60% | -2.00% | -2.30% | -2.50% |

| 03:13 | CNY | Trade Balance (CNY) Nov | 264B | 238B | 254B | |

| 03:36 | CNY | Trade Balance (USD) Nov | 40.2B | 34.9B | 38.2B | |

| 07:00 | EUR | German Trade Balance (EUR) Oct | 19.9B | 22.3B | 21.8B | 21.9B |

| 09:30 | GBP | Industrial Production M/M Oct | 0.00% | 0.00% | 0.70% | |

| 09:30 | GBP | Industrial Production Y/Y Oct | 3.60% | 3.50% | 2.50% | |

| 09:30 | GBP | Manufacturing Production M/M Oct | 0.10% | 0.00% | 0.70% | |

| 09:30 | GBP | Manufacturing Production Y/Y Oct | 3.90% | 3.80% | 2.70% | |

| 09:30 | GBP | Construction Output M/M Oct | -1.70% | 0.10% | -1.60% | |

| 09:30 | GBP | Visible Trade Balance (GBP) Oct | -10.8B | -11.5B | -11.3B | |

| 12:06 | GBP | NIESR GDP Estimate Nov | 0.50% | 0.40% | 0.50% | |

| 13:15 | CAD | Housing Starts Nov | 252.2K | 221K | 223K | 222.7K |

| 13:30 | CAD | Capacity Utilization Rate Q3 | 85.00% | 85.20% | 85.00% | |

| 13:30 | USD | Change in Non-farm Payrolls Nov | 228K | 200K | 261K | 244K |

| 13:30 | USD | Unemployment Rate Nov | 4.10% | 4.10% | 4.10% | |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.20% | 0.30% | 0.00% | |

| 15:00 | USD | U. of Mich. Sentiment (Dec P) | 99 | 98.5 |