{kind=link}

As liquidity conditions have normalized quickly after the holiday lull, markets are digesting the fallout from Washington’s weekend raid in Venezuela and the capture of President Nicolás Maduro. While the operation initially triggered a spike in geopolitical risk, price action suggests investors remain cautious but far from alarmed.

The greenback rallied broadly alongside precious metals as safe-haven demand picked up. However, risk sentiment has not deteriorated meaningfully. Asian equities were notably resilient, with Nikkei 225 posting strong gains, indicating the absence of broad risk-off positioning. Oil prices have also remained relatively steady, reinforcing the view that markets are not yet pricing material supply disruption or wider geopolitical spillovers. For now, the reaction remains contained across asset classes.

That reflects a familiar pattern. Unless geopolitical shocks escalate beyond regional boundaries, markets tend to refocus quickly on macro fundamentals. So far, investors appear to be treating developments in Venezuela as serious but localized.

Attention is therefore shifting back to the economic calendar for clearer directional guidance. This week’s focus is firmly on heavyweight US data, beginning with ISM Manufacturing, followed by ISM Services midweek. The main event, however, will be December non-farm payrolls on Friday. The report will offer the first clean read on US labor conditions following last year’s data distortions and is likely to drive short-term volatility across FX and rates.

Even so, the set of data is unlikely to alter expectations for a January hold by the Fed. While the data could influence pricing around a possible March rate cut, it will not be decisive, with further inflation and employment releases due before that meeting.

For now, Dollar sits at the top of the performance table, followed by Yen and Swiss Franc as secondary haven beneficiaries. At the other end, Aussie lags, trailed by Loonie and Kiwi. Euro and Sterling are trading in the middle.

In Asia, Nikkei closed up 2.97%. Hong Kong HSI is up 0.02%. China Shanghai SSE rose 1.38%. Singapore Strait Times is up 0.67%. Japan 10-year JGB yield rose 0.048 to 2.122.

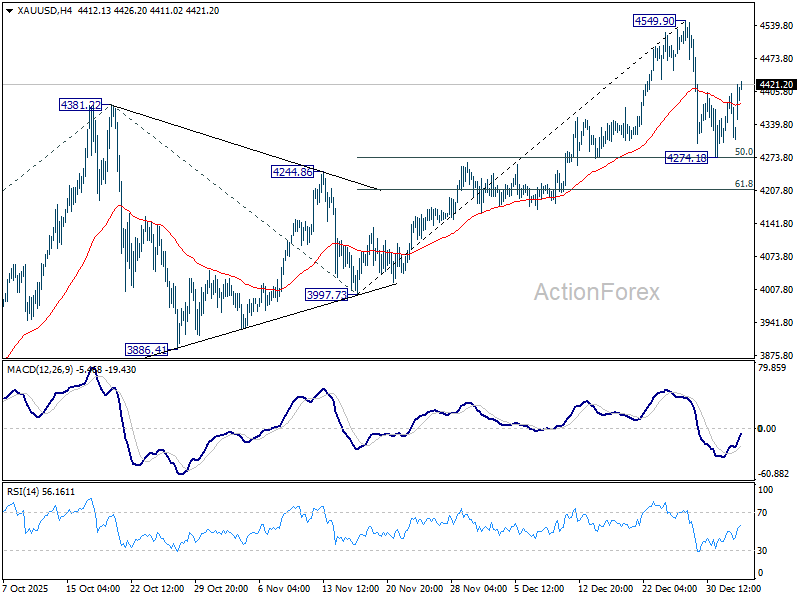

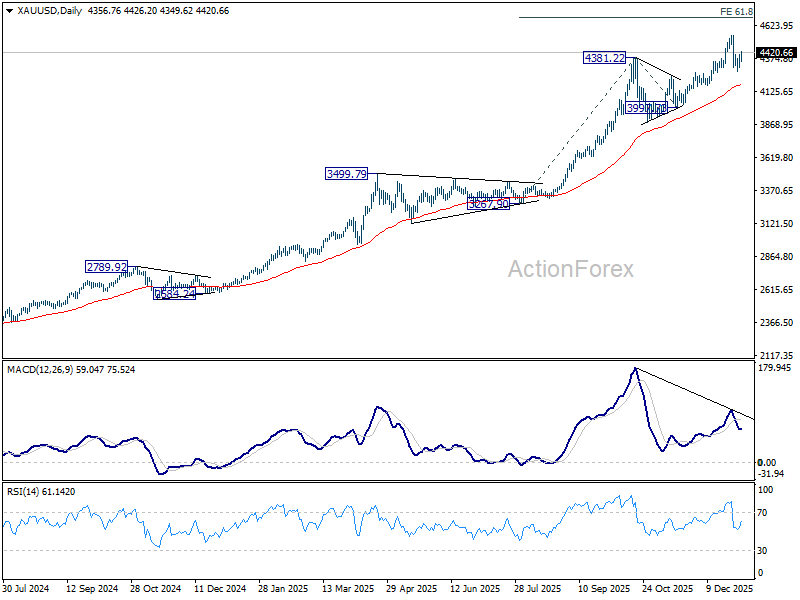

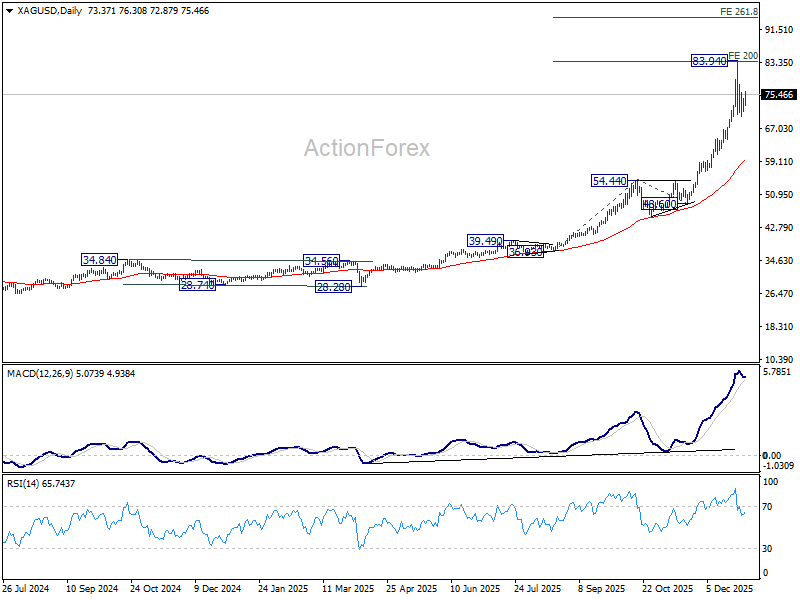

Gold and Silver bounce on Venezuela shock, bull trends intact

Safe-haven demand is flowing back into precious metals, with Gold and Silver posting notable rebounds at the start of the week. Price action in both metals remains corrective following recent record highs. The resilience reinforces the view that larger uptrends remain intact for new record highs later in Q1.

The trigger for the renewed haven bid was news that the US captured Venezuelan President Nicolás Maduro over the weekend. Saturday’s operation marked Washington’s most controversial intervention in the region since the invasion of Panama nearly four decades ago. The symbolism of the move have unsettled regional stability assumptions, pushing investors back toward assets perceived as protection against geopolitical shocks.

Technically, Gold’s recent pullback from 4549.90 was slightly deeper than expected, nearly reaching 50% retracement of 3,997.73 to 4,549.90 at 4,273.81. Still, price has remained well supported above 55 D EMA (now at 4,172.34), keeping the long-term uptrend intact.

Once the current consolidation phase completes, the longer-term bullish trend is expected to reassert itself. Decisive break above 4,549.90 would open the way toward 61.8% projection of 3,267.90 to 4,381.22 from 3,997.73 at 4,685.76. However, bearish divergence on D MACD suggests strong resistance could emerge near that zone, capping upside on the first attempt.

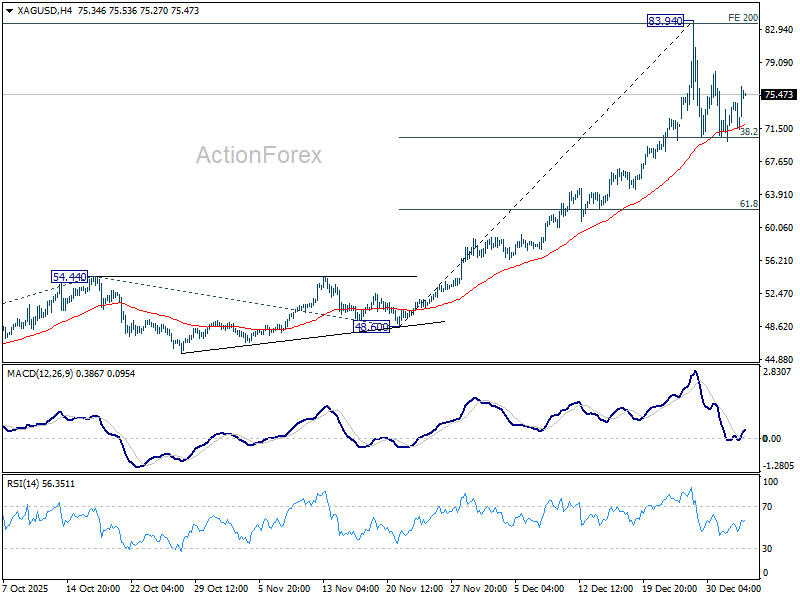

Silver continues to display relative strength versus Gold. Support has been confirmed near 38.2% retracement of 48.60 to 83.94 at 70.44. The price action since remains viewed as a sideways consolidation, expected to remain bounded within the 70–84 range.

On resumption, the next major upside target for Silver sits at 261.8% projection of 36.93 to 54.44 from 48.50 at 94.43. Though, that level may be adjusted depending on the depth and duration of the current consolidation.

BoJ’s Ueda sees durable wage-price cycle, signals scope for further hikes

BoJ Governor Kazuo Ueda reaffirmed the tightening bias today, adding wages and prices are “highly likely to rise together moderately.” In a speech he said adjusting the degree of monetary support would help place the economy on a path toward sustained growth.

Ueda added that the central bank will continue to raise interest rates if economic activity and inflation evolve in line with its forecasts. Also, Japan’s economy maintained a moderate recovery last year despite pressure on corporate profits from higher U.S. tariffs.

Speaking at the same banking event, Finance Minister Satsuki Katayama said Japan is at a critical stage of shifting toward a growth-driven economy after decades of deflation.

Japan PMI manufacturing stabilizes at 50.0, weak Yen lifts inflation risks

Japan’s Manufacturing PMI was finalized at 50.0 in December, rising from 48.7 in November and ending a five-month stretch of contraction. The reading points to stabilization rather than renewed expansion, but marks a clear improvement in underlying momentum as 2025 drew to a close.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, factories reported a much softer decline in sales alongside broadly steady production levels. Employment also provided a modest positive signal, with staffing levels rising at a slightly faster pace as firms positioned for firmer demand in the months ahead.

That said, confidence remains fragile. Respondents continued to flag headwinds from sluggish global conditions, Japan’s ageing population, and rising cost pressures. Input prices climbed at the fastest pace since April, driven by higher raw material and labor costs as well as a weak Yen, prompting firms to lift output prices to protect margins.

China’s private PMI services falls to 52.0, constraints persist into 2026

China’s RatingDog PMI Services edged down from 52.1 to 52.0 in December, marking the lowest level in six months and extending the slowdown in growth momentum for a fourth consecutive month.

According to Yao Yu, founder of RatingDog, the sector ended the year with a “modest growth, high expectations” profile. Survey responses showed an improvement in business confidence, offering some “psychological support” for the 2026 outlook.

However, structural headwinds remain evident. Employment continued to contract, while volatile external demand weighed on new business. Both will remain “key constraints facing the sector.”

From Fed gridlock to RBA hawkishness, US NFP and AU CPI to drive early-year volatility

The policy divide that shaped the Fed’s debate through the second half of 2025 is set to define early-2026 trading as well. Persistent tension between maximum employment and price stability has left the FOMC deeply split. That tension is expected to continue.

This week’s U.S. data may help narrow the fault lines, but expectations are modest. ISM Manufacturing and ISM Services provide useful color on activity, yet the December non-farm payroll report stands as the decisive macro event of the first full trading week of the year.

Crucially, the end of the government shutdown in November means labor data should return to normal reporting standards. For Fed officials, the key question is whether employment remains strong enough to tolerate prolonged restraint, or whether cooling argues for further easing in 2026.

That judgment directly feeds into rate expectations. The prevailing base case remains just one 25bp cut this year. Yet, pricing reflects a near coin-toss between delivery in Q1 or Q2, with policymakers wary of acting too early against still-sticky inflation dynamics. While no single data point will decide the outcome, December payrolls could set the tone for January trading.

Staying in North America, Canadian labour market data is another focus for the week ahead. After a run of firmer-than-expected prints through the autumn, December employment is expected to show some pullback . Even so, the data should remain broadly consistent with early signs of stabilization.

Beneath the surface, however, heavily trade-exposed sectors continue to lag broader employment trends. Yet, there is little evidence that this weakness is spreading across the wider Canadian economy. Thus, December’s report is unlikely to materially shift the near-term outlook for the BoC. A prolong hold is expected until the next move as a hike, but unlikely to be before 2027.

Outside the North America, Australia stands out as a potential volatility source. CPI data this week lands just after a notably hawkish shift by the RBA, which has reopened debate over whether policy may tighten again rather than continue easing.

Speculation has grown that the RBA could deliver a rate hike as early as February if price pressures fail to cool. Commonwealth Bank of Australia now expects one increase next year to 3.85%, warning of risk toward a larger hiking cycle should growth prove more resilient and inflation more persistent.

That view is echoed by National Australia Bank, whose chief economist Sally Auld forecasts two hikes — in February and May — taking the terminal rate to 4.10%. Much hinges on whether inflation momentum convincingly slows, or instead forces policymakers to reassert control.

Elsewhere, CPI data from the Eurozone, Switzerland and China will be monitored but is unlikely to shift policy expectations materially. ECB remains firmly on hold at 2.00% deposit rate, with next move seen as a hike but timing still distant. The SNB continues to see little deflation risk, keeping rates at 0.00% with a high bar for returning to negative territory. In China, CPI surged to a 21-month high in November, but doubts persist over sustainability, particularly as Yuan strength in late-2025 acts as a disinflationary force.

- Monday: China RatingDog PMI services; Swiss retail sales, PMI manufacturing; US ISM manufacturing.

- Tuesday: Germany CPI flash; Eurozone PMI services final, UK PMI services final.

- Wednesday: Australia CPI; Germany retail sales, unemployment; Swiss foreign currency reserves; UK PMI construction; Eurozone CPI flash; US ADP employment, ISM services.

- Thursday: Japan labor cash earnings; Australia trade balance; Germany factory orders; Swiss CPI; Eurozone PPI; Canada trade balance; US jobless claims, trade balance.

- Friday: Japan household spending; China PPI, CPI; Germany industrial production; Swiss unemployment rate; Eurozone retail sales; Canada employment; US non-farm payroll, U of Michigan consumer sentiment.

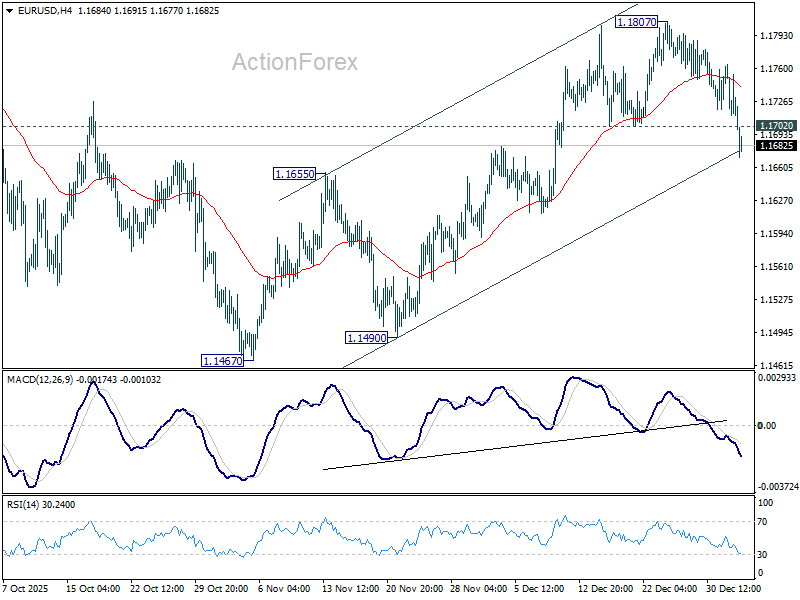

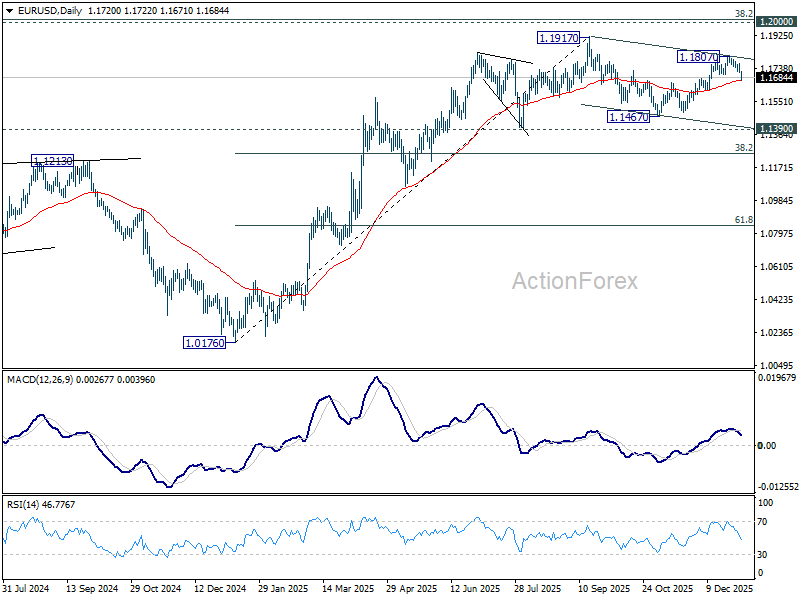

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1701; (P) 1.1733; (R1) 1.1753; More….

EUR/USD’s fall from 1.1807 accelerated lower today and the break of 1.1702 support suggests that rise from 1.1467 could have completed with three waves up to 1.1807. The development argues that fall from 1.1807 is the third leg of the whole pattern from 1.1917 high. Intraday bias is back on the downside. Sustained trading below 55 D EMA (now at 1.1670) will affirm this case and target 1.1467 support and below. For now, risk will stay on the downside as long as 1.1807 resistance holds, in case of recovery.

In the bigger picture, as long as 55 W EMA (now at 1.1408) holds, up trend from 0.9534 (2022 low) is still in favor to continue. Decisive break of 1.2 key psychological level will carry larger bullish implication. However, sustained trading below 55 W EMA will argue that rise from 0.9534 has completed as a three wave corrective bounce, and keep long term outlook bearish.