{kind=link}

Forex markets are trading in mixed fashion, with hesitant tone, as investors continue to digest the controversial US seizure of Venezuelan President Nicolás Maduro over the weekend. While geopolitical risk has clearly entered the equation, price action suggests the response is far from a textbook risk-off move.

There are visible safe-haven bids flowing into Dollar and Yen, both of which are outperforming. However, Swiss Franc is notably lagging, highlighting the uneven nature of defensive positioning. Also, that complexity is evident across asset classes. European equity markets are treading water rather than selling off sharply, supported in part by strong gains in defense stocks. US equity futures are also flat, while Treasury markets show little sign of meaningful inflows. The markets are not pricing systemic escalation risks.

The surge in Gold and Silver initially points to rising risk aversion. However, Copper has also jumped to fresh record highs, muddying the narrative. Strength across both precious and industrial metals suggests the move is likely not purely geopolitics-driven.

That metals backdrop helps explain the relative resilience in Aussie, which is finding some support despite broader Dollar strength. In contrast, Euro and Swiss Franc are clearly under pressure, partly reflecting spillover from Sterling’s strength following strong UK borrowing data.

Overall, Dollar sits at the top of the FX performance table so far today, followed by Yen and Sterling. Loonie is the weakest, trailed by Swiss Franc and Euro, while Aussie and Kiwi trade in the middle.

For now, markets appear content to wait for clarity, hoping geopolitical tensions fade and attention returns to data and policy fundamentals.

In Europe, at the time of writing, FTSE is up 0.35%. DAX is up 0.71%. CAC is up 0.04%. UK 10-year yield is down -0.018 at 4.521. Germany 10-year yield is down -0.013 at 2.890. Earlier in Asia, Nikkei rose 2.97%. Hong Kong HSI rose 0.03%. China Shanghai SSE rose 1.38%. Singapore Strait Times rose 0.52%. Japan 10-year JGB yield rose 0.047 to 2.120.

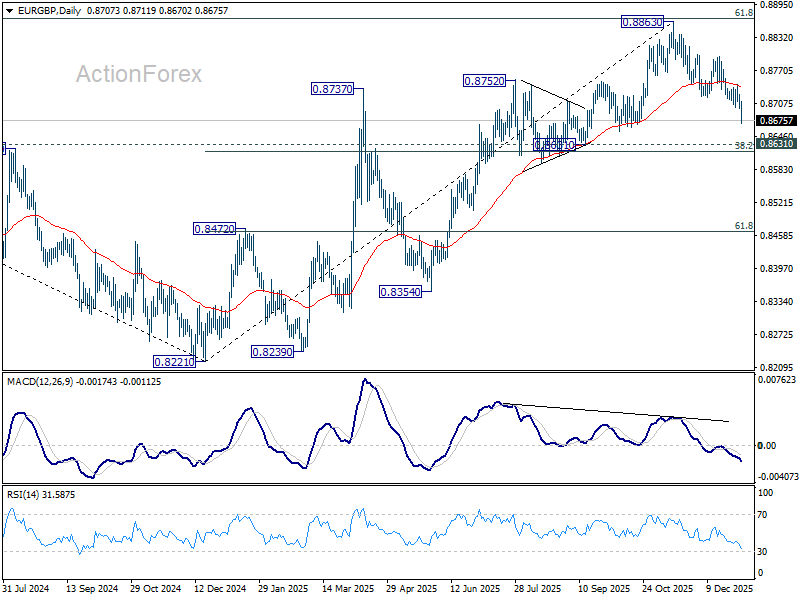

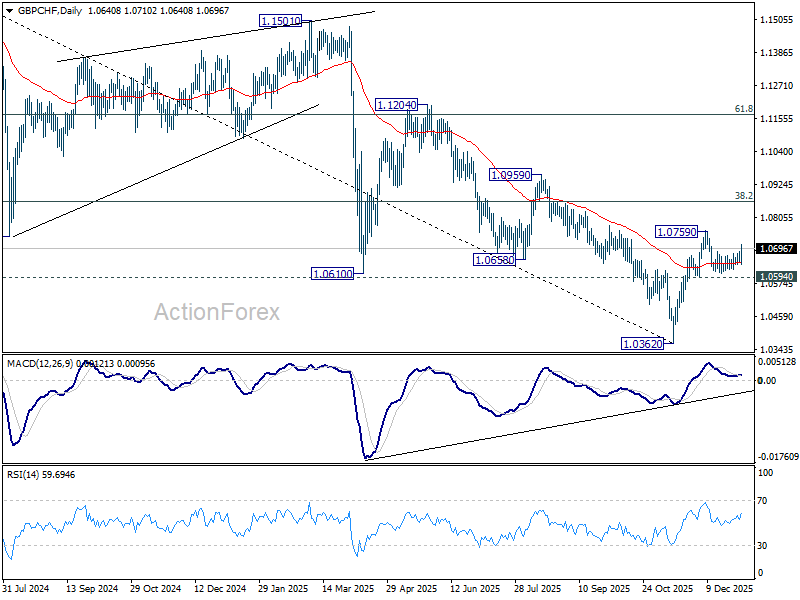

EUR/GBP slides, GBP/CHF jumps; strong UK borrowing data fuels Sterling strength

Sterling is rallying sharply today as UK domestic data challenge expectations of a smooth cooling in demand. The catalyst appears to be November consumer credit data from the BoE, which showed borrowing rose by GBP 2.08B, the largest monthly increase in two years and stronger than any economist forecast.

Annual growth in consumer credit also accelerated to 8.1%, from 7.5% previously. Credit card borrowing surged 12.1%, while other consumer credit expanded 6.3%, highlighting robust appetite for spending rather than precautionary retrenchment, even before the government’s Autumn Budget.

Elevated borrowing, especially via credit cards, points to consumer demand holding up more firmly than anticipated, keeping services inflation under upward pressure — the very area where the BoE has struggled to secure sustained disinflation progress.

That backdrop strengthens the case for caution at the February policy meeting. The data give hawkish members of the Monetary Policy Committee justification to push for a hold, at least until post-holiday spending data confirms whether momentum is truly fading.

Technically, Sterling strength is driving EUR/GBP lower, with downside momentum accelerating toward the 0.8618–0.8631 support zone (38.2% retracement of 0.8221 to 0.8663 at 0.8618). A clean break there would signal that the rebound from the 2024 low at 0.8221 has already run its course as a corrective move, shifting the near-term outlook decisively bearish.

In GBP/CHF, today’s bounce argues that support near the 55-day EMA and above 1.0594 has held decisively. That keeps the rebound from 1.0362 alive, with a retest of 1.0759 likely soon. Sustained break higher would target 38.2% retracement of 1.1675 to 1.0362 at 1.0864, even still as a corrective move.

BoJ’s Ueda sees durable wage-price cycle, signals scope for further hikes

BoJ Governor Kazuo Ueda reaffirmed the tightening bias today, adding wages and prices are “highly likely to rise together moderately.” In a speech he said adjusting the degree of monetary support would help place the economy on a path toward sustained growth.

Ueda added that the central bank will continue to raise interest rates if economic activity and inflation evolve in line with its forecasts. Also, Japan’s economy maintained a moderate recovery last year despite pressure on corporate profits from higher U.S. tariffs.

Speaking at the same banking event, Finance Minister Satsuki Katayama said Japan is at a critical stage of shifting toward a growth-driven economy after decades of deflation.

Japan PMI manufacturing stabilizes at 50.0, weak Yen lifts inflation risks

Japan’s Manufacturing PMI was finalized at 50.0 in December, rising from 48.7 in November and ending a five-month stretch of contraction. The reading points to stabilization rather than renewed expansion, but marks a clear improvement in underlying momentum as 2025 drew to a close.

According to Annabel Fiddes, Economics Associate Director at S&P Global Market Intelligence, factories reported a much softer decline in sales alongside broadly steady production levels. Employment also provided a modest positive signal, with staffing levels rising at a slightly faster pace as firms positioned for firmer demand in the months ahead.

That said, confidence remains fragile. Respondents continued to flag headwinds from sluggish global conditions, Japan’s ageing population, and rising cost pressures. Input prices climbed at the fastest pace since April, driven by higher raw material and labor costs as well as a weak Yen, prompting firms to lift output prices to protect margins.

China’s private PMI services falls to 52.0, constraints persist into 2026

China’s RatingDog PMI Services edged down from 52.1 to 52.0 in December, marking the lowest level in six months and extending the slowdown in growth momentum for a fourth consecutive month.

According to Yao Yu, founder of RatingDog, the sector ended the year with a “modest growth, high expectations” profile. Survey responses showed an improvement in business confidence, offering some “psychological support” for the 2026 outlook.

However, structural headwinds remain evident. Employment continued to contract, while volatile external demand weighed on new business. Both will remain “key constraints facing the sector.”

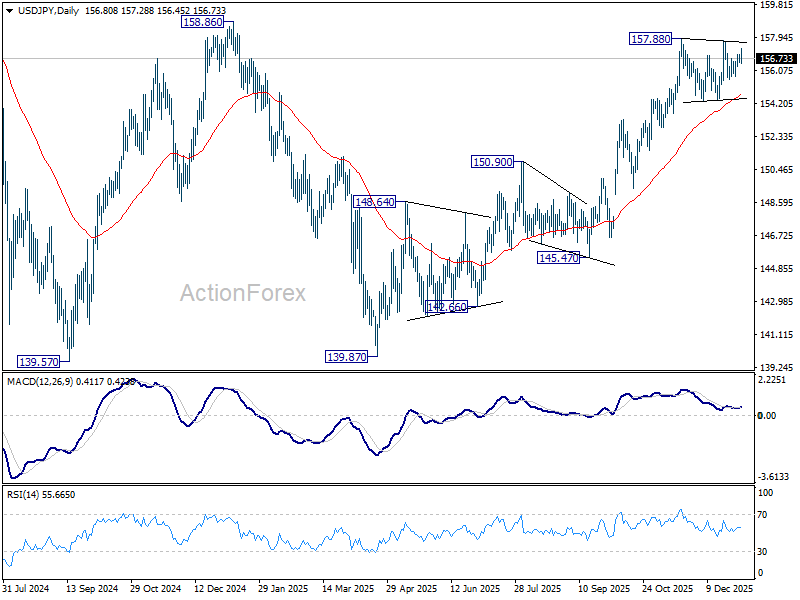

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.57; (P) 156.79; (R1) 157.05; More…

USD/JPY’s recovery lost momentum ahead of 157.75 resistance. Intraday bias remains neutral and more consolidations could be seen. But outlook will stay bullish as long as 154.33 support holds. On the upside, firm break of 158.85 key structural resistance will be an important medium term bullish sign. Next target will be 161.94 high. However, decisive break of 154.38 will turn bias to the downside for deeper correction.

In the bigger picture, corrective pattern from 161.94 (2024 high) could have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94 high. Decisive break of 158.85 structural resistance will solidify this bullish case and target 161.94 for confirmation. On the downside, break of 150.90 resistance turned support will dampen this bullish view and extend the corrective range pattern with another falling leg.