{kind=link}

Risk sentiment turned decisively positive overnight and carried through the Asian session as traders looked past Venezuela-related geopolitical risks. The shift marked a clear return to risk-on positioning, and prompted a broad reversal in the Dollar, which broke lower after firming earlier on Monday. With haven demand fading, the greenback slipped to the bottom of the FX performance table as investors rotated toward higher-beta and commodity-linked currencies.

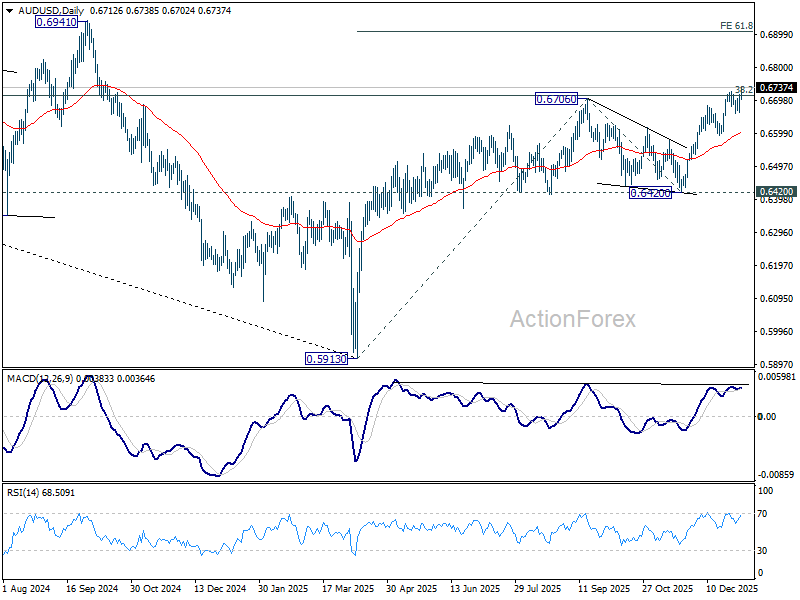

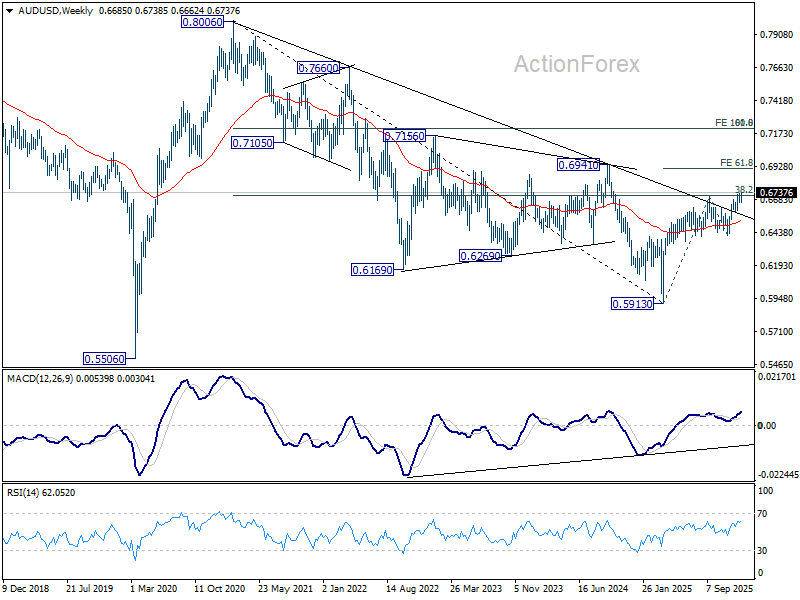

Australian Dollar emerged as a clear beneficiary, jumping broadly across the board, with strength reinforced by a renewed rally in metals, led by Copper pushing further into record territory. Support from commodities helped lift AUD/USD to its highest level since late 2024.

In contrast, traditional havens came under pressure. Both Yen and Swiss Franc weakened as risk appetite improved, with Yen facing additional headwinds from domestic fiscal concerns in Japan. Japanese government bonds sold off after soft demand at a 10-year auction. The bid-to-cover ratio fell to 3.30 from 3.59 at the previous sale, while the auction tail widened to 0.05 yen, signaling weaker investor appetite. As a result, the 10-year JGB yield climbed to its highest level since February 1999.

Across markets, Dollar is currently the weakest major currency, followed by Swiss Franc and Yen. Aussie and Kiwi lead gains, with Euro also firmer. Sterling and Loonie trade in the middle.

Overnight, US equities surged — DOW rose 1.23%, S&P 500 gained 0.64%, and NASDAQ Composite advanced 0.69%. In Asia, Nikkei rose 1.32%. Hong Kong HSI is up 1.39%. China Shanghai SSE rose 1.50%. Singapore Strait Times is up 1.18%. Japan 10-year JGB yield rose 0.015 to 2.134.

UD/USD breaks higher decisively, risk appetite returns as markets look past Venezuela

Risk appetite has returned decisively, pushing DOW to fresh record highs overnight and drawing Asian markets higher in its wake. The improved tone has spilled into FX, with Australian Dollar emerging as the strongest performer amid renewed risk-on sentiment.

The US deposition of Venezuelan President Nicolás Maduro initially injected caution into markets. However, investor hesitation proved short-lived as participants reassessed the broader implications and found little reason to sustain defensive positioning.

A growing consensus has emerged that events in Venezuela are unlikely to disrupt global or Latin American financial markets. Crucially, investors see limited risk of spillovers into energy markets, removing a key channel through which geopolitical shocks typically feed into broader macro pricing.

Oil’s muted reaction has been central to the shift back toward risk. With crude prices steady, markets are increasingly confident that the Venezuela developments will not materially affect US inflation dynamics, keeping the Fed’s easing path intact. That backdrop supports expectations for at least one further rate cut this year.

Technically, AUD/USD has resumed its uptrend after firm break above the 38.2% retracement of 0.8006 to 0.5913 at 0.6713. The move strengthens the case that the rebound from 0.5913 is evolving into a broader trend reversal of the decline from the 2021 high at 0.8006. The next near-term target is seen at 61.8% projection of 0.5913 to 0.6706 from 0.6420 at 0.6910.

Japan monetary base drops below JPY 600T, as BoJ presses ahead with normalization

Japan’s monetary base contracted in 2025 for the first time since 2007, underlining the Bank of Japan’s decisive shift away from decades of ultra-loose policy. Data released today showed the average balance of the monetary base fell -4.9% year-on-year, echoing the period when the BoJ last embarked on a rate-hike cycle.

The contraction accelerated toward year-end. The average balance in December stood at JPY 594.19 trillion, down -9.8% yoy and falling below the JPY 600 trillion mark for the first time since September 2020.

The decline reflects the BoJ’s ongoing exit from its decade-long stimulus, which began in 2024. Since then, the central bank has raised interest rates, slowed purchases of JGBs and wound down funding schemes designed to encourage bank lending. With policy normalization still underway, Japan’s monetary base is expected to continue shrinking as bond tapering and further rate hikes proceed.

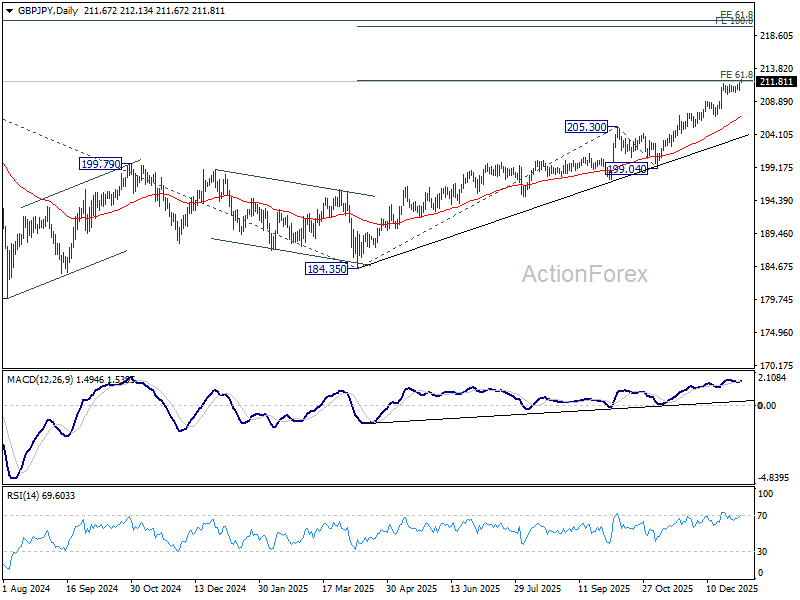

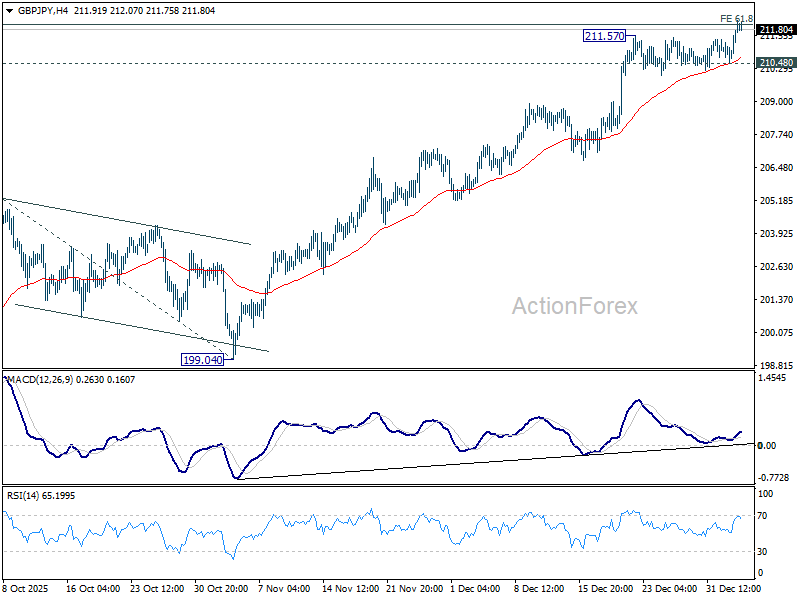

GBP/JPY Daily Outlook

Daily Pivots: (S1) 210.93; (P) 211.39; (R1) 212.27; More…

GBP/JPY’s rally resumed by breaking through 211.57 temporary top and intraday bias is back on the upside. Decisive break of 61.8% projection of 184.35 to 205.30 from 199.04 at 211.98 will extend current up trend to 100% projection at 219.99 next. On the downside, break of 210.48 support will argue that a short term top is already formed, and turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 to 208.09 from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.