{kind=link}

News of a US criminal investigation into Fed Chair Jerome Powell dominated global financial headlines, injecting a fresh dose of political risk into markets. While the investigation itself was unsettling, the sharper jolt came from Powell’s unusually direct response, which framed the episode as part of a broader campaign to pressure the central bank.

In a formal statement posted on the Fed’s website, Powell warned that the threat of criminal charges was a consequence of “broader threats and ongoing pressure” by the administration. The language marked a rare and blunt escalation from a Fed chair typically careful to avoid political confrontation.

Powell went further, stating explicitly that “the threat of criminal charges is a consequence of the Federal Reserve setting interest rates based on our best assessment of what will serve the public, rather than following the preferences of the President.” Markets interpreted the remark as confirmation that tensions between the Fed and the Donald Trump administration have entered a more confrontational phase.

The clash unsettled markets, but reactions so far remain contained. Gold was the clear standout, surging to fresh record highs as investors sought protection against institutional risk and perceived threats to monetary policy independence. By contrast, moves elsewhere were more restrained. Dollar traded broadly lower, but the selloff lacked momentum. US equity futures dipped modestly, stopping well short of anything resembling disorderly risk-off conditions. Crucially, interest-rate expectations remain stable. Pricing for a March Fed rate cut is largely unchanged, with markets still assigning only around a 30% probability.

For now, investors appear reluctant to extrapolate political noise into imminent policy shifts. But that calm could prove fragile. If the standoff between Trump and Powell intensifies further, markets may be forced to reassess not just Fed independence, but the credibility of forward guidance itself. For now, however, investors are treating the episode as a risk premium adjustment rather than a regime shift.

Elsewhere, Yen continued to weaken, pressured by domestic political developments. Public broadcaster NHK reported that Japan’s ruling Liberal Democratic Party is preparing to dissolve the Lower House later this month, paving the way for a snap election likely in February. The move is seen as an attempt to capitalize on Prime Minister Sanae Takaichi’s strong approval ratings and stabilize the ruling coalition, including the Japan Innovation Party. Japan is on holiday today, leaving markets to assess whether the sharp jump in Nikkei futures will translate into a gap higher and follow-through momentum when trading resumes.

Overall, Dollar sits at the bottom of the performance table so far today, followed by Yen and then Loonie. Swiss Franc leads gains, with Euro and Kiwi close behind, while Aussie and Sterling are broadly in the middle of the pack.

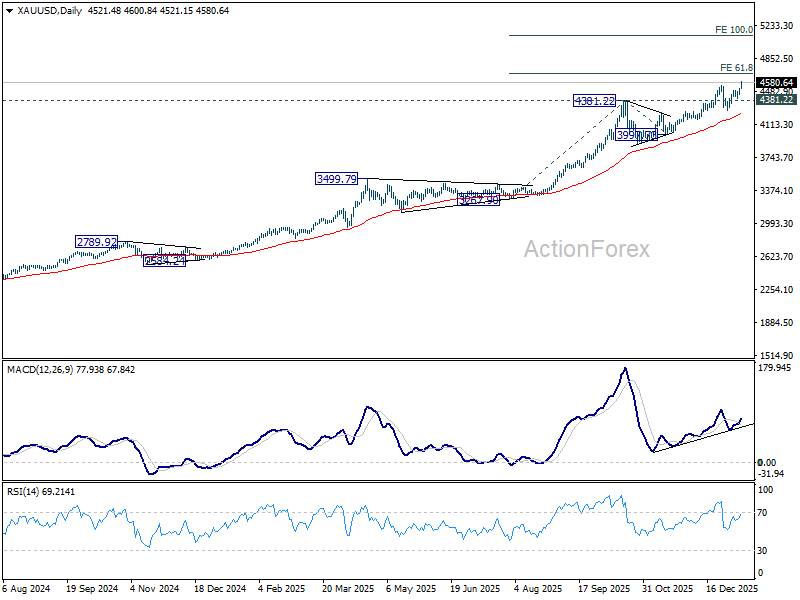

Powell investigation shock sparks Gold rush as 5,000 comes into view

Gold surged to a fresh record high, with Silver following close behind, as markets reassessed political risk around US monetary policy. The 4,685 projection firmly within reach for Gold, and break of which would pave the way to 5,000 psychological level and above.

Additionally, after a year of Silver leadership, momentum may now be shifting back toward Gold, a shift consistent with rising concern over institutional credibility rather than cyclical reflation.

The immediate catalyst came US prosecutors launched on Friday a criminal investigation into Fed Chair Jay Powell. The development jolted markets, reviving concerns that the central bank could face increasing political interference at a time when policy credibility remains critical.

The episode is widely seen as the latest salvo from the Donald Trump administration against the Fed. The central bank has been under sustained pressure to ease policy faster, even as policymakers remain wary of reigniting price pressures or undermining hard-won inflation progress.

Powell, in a statement released Sunday, confirmed that the Fed had received grand jury subpoenas and a threat of criminal indictment from the Justice Department. The matter relates to his testimony before Congress concerning a USD 2.5B renovation of the Fed’s headquarters, though Powell framed the move in a much broader political context.

He warned that the action should be seen against a backdrop of ongoing threats and pressure aimed at forcing lower interest rates and securing greater political control over monetary policy. He said bluntly, “this unprecedented action should be seen in the broader context of the administration’s threats and ongoing pressure”.

Technically, Gold’s up trend resumed and it’s now on track to 61.8% projection of 3,267.90 to 4,381.22 from 3,997.73 at 4,685.76. Decisive break there will pave the way to 5,000 psychological level, and possible further to 100% projection at 5,111.05. Outlook will stay bullish as long as 4,381.22 resistance turned support holds, in case of retreat.

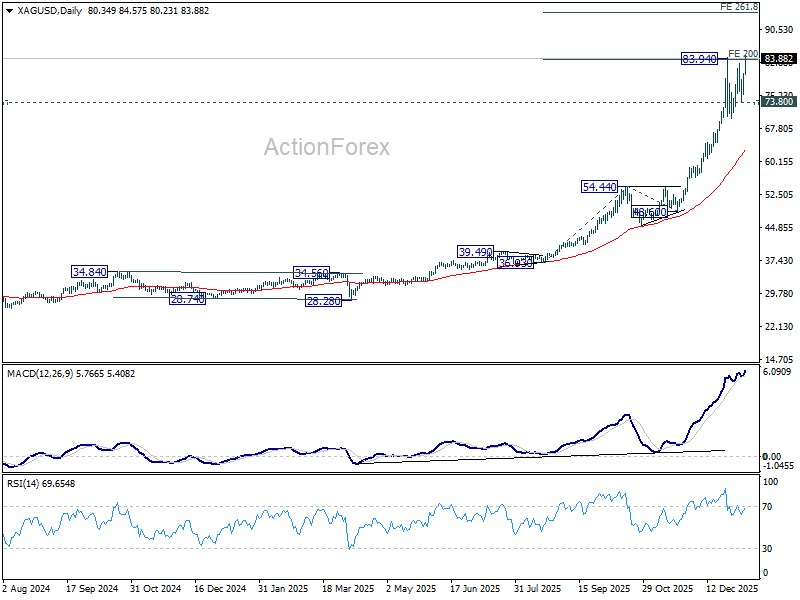

Silver is also trying to resume its long term up trend. Sustained trading above 83.94 resistance will pave the way to 261.8% projection of 36.93 to 54.44 from 48.50 at 94.34. Nevertheless, break of 73.80 will bring another pullback first.

US December CPI seen as speed bump, not a turning point for risk markets

December US inflation data dominates the macro calendar, as the broader week is filled mostly with second-tier releases. For markets, CPI is the key checkpoint for Fed policy expectations, though the bar for a disruptive surprise appears high.

November’s CPI print drew criticism from some economists, who argued that prolonged US government shutdown effects may have dampened the readings. Disruptions were seen as distorting seasonal patterns and muting underlying price pressures, leaving markets cautious about overinterpreting the softness.

Those distortions should fade in the December release. Consensus looks for headline CPI to hold steady at 2.7%, while core CPI is expected to tick higher from 2.6% to 2.7%. Such an outcome would offer little encouragement for earlier easing from the Fed. With core inflation still sticky, policymakers are likely to maintain their wait-and-see approach.

Markets pricing suggests just over a 70% chance of no change in March, with June shaping up as the earliest realistic opportunity for a cut, coinciding with updated economic projections that could give the Fed greater confidence.

Importantly, this outlook appears largely embedded in asset prices. As long as the data does not force a meaningful shift in the expected rate path. As a result, CPI may prove to be more of a clearing event than a catalyst. Absent a dramatic surprise, risk-on momentum could extend once uncertainty around the release passes, with investors comfortable holding positions aligned to mid-year easing.

In the UK, monthly GDP data is another focal point, with expectations for marginal growth of 0–0.1% in November. Activity had been weighed down by uncertainty ahead of the Autumn Budget, a drag that likely lingered, though consumer-facing sectors may have seen some support from pre-holiday demand and Black Friday promotions.

For the BoE, ongoing weakness in activity strengthens the case for further cuts, even if delivered cautiously. However, policymaker rhetoric continues to highlight internal divisions, leaving February finely balanced, while March remains the more probable window for the next move.

Here are some highlights for the week:

- Monday: Eurozone Sentix investor confidence:

- Tuesday: New Zealand NZIER business confidence; Australia Westpac consumer sentiment; US CPI.

- Wednesday: China trade balance; US retail sales, PPI, Fed’s Beige Book.

- Thursday: Japan PPI; UK GDP; Eurozone industrial production, trade balance; Canada manufacturing sales, wholesale sales; US jobless claims, Empire state manufacturing; Philly Fed manufacturing, import prices.

- Friday: New Zealand BNZ manufacturing; US industrial production, NAHB housing index.

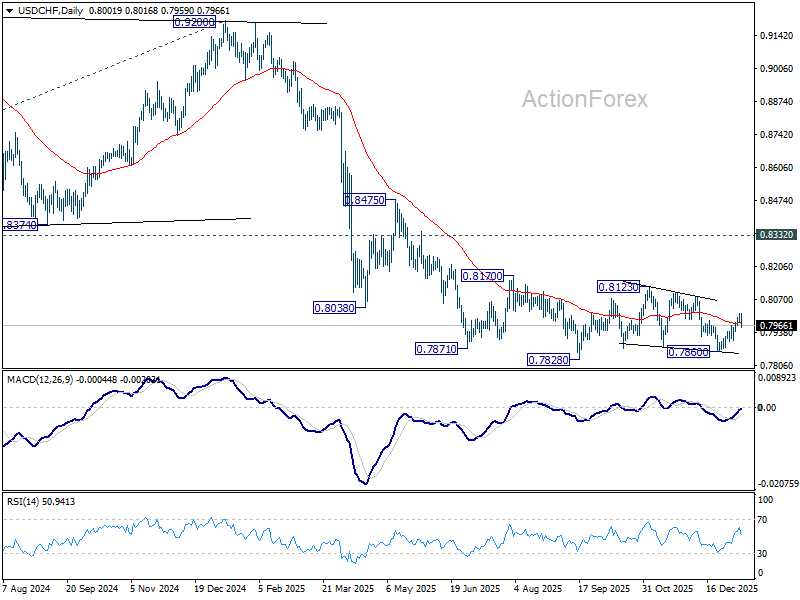

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.7990; (P) 0.8004; (R1) 0.8026; More….

Intraday bias in USD/CHF is turned neutral with today’s retreat and break of 0.7967 minor support. Overall outlook is unchanged that corrective pattern from 0.7828 low is extending. On the upside, above 0.8016 will target 08123 resistance next. Nevertheless, break of 0.7860 will bring retest of 0.7828, with odds of a break there to resume the larger down trend.

In the bigger picture, price actions from 0.7828 are seen as a correction. Larger down trend from 1.0342 (2017 high) is in still in progress. Break of 0.7828 will target 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382. In any case, outlook will stay bearish as long as 0.8332 support turned resistance holds (2023 low).