{kind=link}

Early market nervousness over a potential escalation in the Middle East eased as investors reassessed the likelihood of near-term US military intervention in Iran. Initial risk-off moves faded quickly, helping stabilize broader sentiment. A key factor was messaging from US President Donald Trump, who signaled that Washington may not intervene militarily in Iran, at least for now. His comments helped temper fears of an immediate escalation and reduced demand for safe havens. Gold retreated from its record highs, while WTI crude oil slipped back toward the 60 level as the immediate geopolitical risk premium was partially unwound.

Tensions remain elevated, however. Iran’s leadership is grappling with its worst domestic unrest in decades, and Tehran has threatened US military bases in the region in an attempt to deter American involvement. At the White House, Trump struck a cautious tone. He cited reports from “very important sources” suggesting that killings in Iran’s crackdown were subsiding. While Trump did not rule out military action outright, he said the administration would “watch what the process is,” noting that the US had received what he described as a “very good statement” from Iran.

Separately, Trump sought to talk down concerns over his standoff with Fed Chair Jerome Powell, saying he had “no plan” to fire Powell. Asked whether the investigation into Powell could change that stance, Trump said the administration was in a “holding pattern” and that it was “too soon” to decide. Trump also offered no new clarity on succession planning at the Fed, as he was inclined to nominate either former Fed Governor Kevin Warsh or National Economic Council Director Kevin Hassett when Powell’s term ends. Announcement is expected “over the next couple of weeks.”

On trade, Trump unveiled a new tariff mechanism targeting NVIDIA and Advanced Micro Devices, designed to enforce a 25% cut of AI chip sales to China. The move follows December’s decision to allow Nvidia’s H200 chips to be shipped to China, reversing an outright ban but attaching a revenue-sharing requirement. The tariff applies to AI chips imported into the US and then transshipped globally, including Nvidia’s H200 and AMD’s MI325X. The move highlights the administration’s preference for deal-based, transactional trade enforcement.

In FX markets this week, Sterling is the top performer so far, though stronger-than-expected UK GDP has failed to add fresh momentum. Kiwi and Loonie follow, largely stabilizing after recent losses. Yen remains pinned at the bottom despite a brief bounce on intensified verbal intervention, while Aussie and Euro lag. Dollar and Swiss Franc sit in the middle of the pack.

In Asia, Nikkei fell -0.42%. Hong Kong HSI fell -0.28%. China Shanghai SSE fell -0.33%. Singapore Strait Times is up 0.20%. Japan 10-year JGB yield fell -0.018 to 2.169. Overnight, DOW fell -0.09%. S&P 500 fell -0.53%. NASASQ fell -1.00%. 10-year yield fell -0.031 to 4.140.

UK GDP beats with 0.3% mom growth in November, services lead

UK economic output surprised to the upside in November, offering a modest boost to the growth outlook late in the year. GDP rose 0.3% mom, beating expectations for flat growth, with strength concentrated in services and production.

Services output increased 0.3% mom, while production jumped 1.1% mom, offsetting a sharp -1.3% mom decline in construction activity. The data points to improving momentum in consumer- and business-facing sectors, even as construction continues to struggle.

Over the three months to November, GDP edged up 0.1%. Services grew 0.2%, while production slipped -0.1% due largely to weaker motor vehicle manufacturing, and construction fell -1.1%. On a year-on-year basis, GDP expanded 1.3%, led by services growth of 1.4%. Production rose 0.4% and construction rose 0.7%.

Fed’s Beige Book signals steady jobs, moderating price pressures

The latest Beige Book from the Fed showed US economic activity improving modestly, with eight of twelve Districts reporting growth at a “slight to modest pace”. Three Districts saw no change and one reported a modest decline, marking a better backdrop than recent cycles where stagnation dominated.

Consumer spending firmed modestly, supported by the holiday shopping season, while business activity presented a mixed picture. Manufacturing remained uneven, with five Districts reporting growth and six citing contraction.

Labor market conditions were “mostly unchanged”. Eight Districts reported flat hiring, though multiple contacts noted increased use of temporary workers as firms seek flexibility amid uncertainty. Wage growth continued at a “moderate pace”, with several businesses saying wage pressures have normalized.

Price pressures remained elevated, rising at a moderate pace across most Districts. Tariff-related cost increases were a common theme, and while firms expect “some moderation in price growth ahead”, many anticipate prices will stay high as they pass through accumulated cost increases.

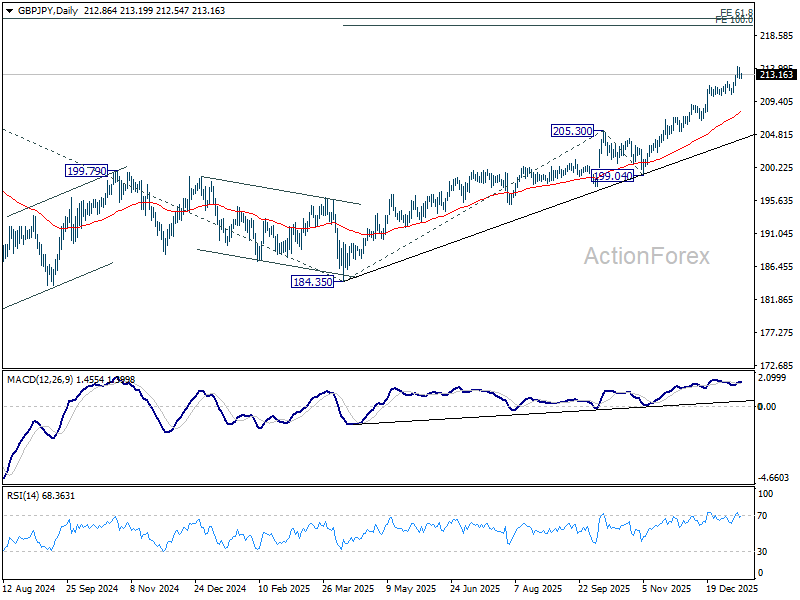

GBP/JPY Daily Outlook

Daily Pivots: (S1) 212.37; (P) 213.25; (R1) 213.93; More…

A temporary top was formed at 214.27 with current retreat. Intraday bias in GBP/JPY is turned neutral first for consolidations. Downside should be contained by 210.28 support to bring another rally. Break of 214.27 will resume larger up trend to 100% projection of 184.35 to 205.30 from 199.04 at 219.99 next. Nevertheless, considering bearish divergence condition in 4H MACD, firm break of 210.28 will confirm short term topping, and turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 123.94 (2020 low) is in progress. Next target is 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. On the downside, break of 205.30 resistance turned support is needed to indicate medium term topping. Otherwise, outlook will stay bullish even in case of deep pullback.