{kind=link}

Risk aversion dominated markets across Asia and spread into Europe today as an abrupt transatlantic diplomatic and trade shock rippled through asset prices. Investors fled to traditional safe havens, pushing Gold and Silver to fresh record highs, while equities came under heavy pressure.

At the core was the dramatic escalation in tensions over Greenland. Donald Trump threatened to impose 10% tariffs on several European allies from February 1, rising to 25% by June unless a deal is reached for the “complete and total purchase of Greenland.” The eight countries named include Denmark, Norway, Sweden, Finland, Germany, France, the Netherlands, and the United Kingdom.”

The risk-aversion impulse quickly lifted precious metals. With tensions unresolved and traders wary of further policy shocks, Gold risks extending toward the 5000 level, and Silver toward 100 if stress deepens further.

Equities, by contrast, bore the brunt of the selloff. European automotive names were particularly weak, with heavyweights such as Volkswagen, BMW, Mercedes‑Benz Group, as well as Milan-listed Ferrari and Stellantis sliding. The sector is seen as vulnerable given globalized supply chains and sensitivity to potential levies and trade barriers.

Despite sharp moves in metals and equities, currency markets have been relatively restrained. Swiss Franc has emerged as the strongest major currency on risk-off flows, followed by Kiwi and Euro. Yen is back at the bottom of the leaderboard, followed by Dollar and Sterling, with Loonie and Aussie positioned in the middle.

Attention now turns to the World Economic Forum in Davos for any diplomatic reprieve, but optimism remains low. The gathering comes amid extraordinary geopolitical tumult, with the Greenland crisis front and center as leaders convene. Compounding market nerves, ongoing conflicts such as the war in Ukraine and other flashpoints continue to test risk appetite.

Greenland risk explodes, tilts Gold towards 5000, Silver towards 100

Risk aversion returned abruptly as the new week opened, propelling Gold and Silver to new all-time highs. With sentiment turning defensive, upside risks are building, raising the prospect of Gold extending toward 5,000 and Silver toward 100 should geopolitical tensions worsen.

At the center of the shock were escalating tensions over Greenland. Over the weekend, US President Donald Trump threatened to impose additional tariffs from February 1 on European countries linked to the dispute over control of the Arctic island. He further warned that duties would rise to 25% from June 1 until what he described as a “complete and total purchase” of Greenland is achieved.

The list of countries explicitly targeted was broad and politically sensitive, spanning Denmark, Norway, Sweden, Finland, Germany, France, the Netherlands, and the United Kingdom. By including both EU members and close U.S. allies, the threat immediately raised concerns about a wider transatlantic rupture rather than a contained bilateral dispute.

Trump’s shift from rhetorical pressure to concrete economic measures marked a clear escalation and signaled that the administration is prepared to use trade policy again as direct geopolitical leverage. With tariffs now explicitly tied to territorial acquisition, the Greenland threat is real rather than symbolic. The episode has intensified fears of deeper political imbalance within Europe and raised uncomfortable questions about the long-term cohesion of NATO, already strained by diverging strategic priorities.

European leaders reacted quickly, condemning the move as unacceptable and signaling a unified response. After emergency talks on Sunday, EU officials began weighing counter-tariffs worth up to EUR 93 billion on U.S. imports.

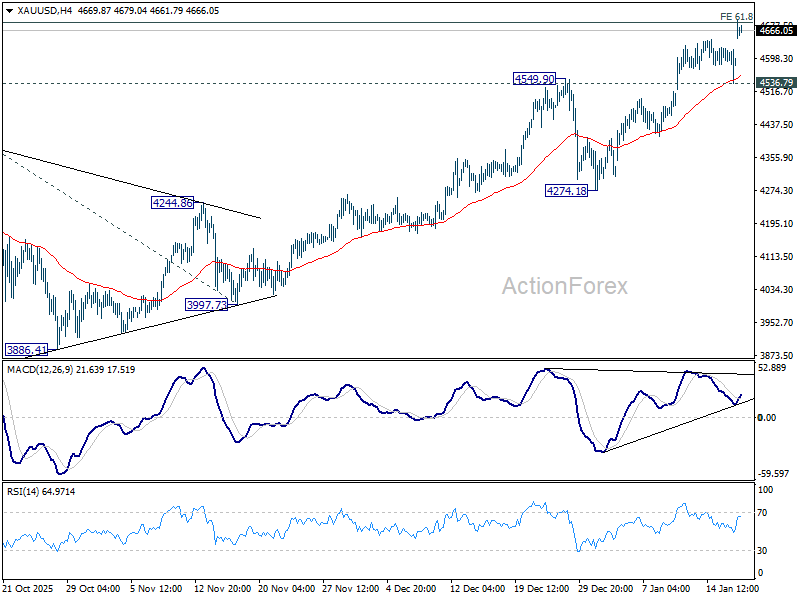

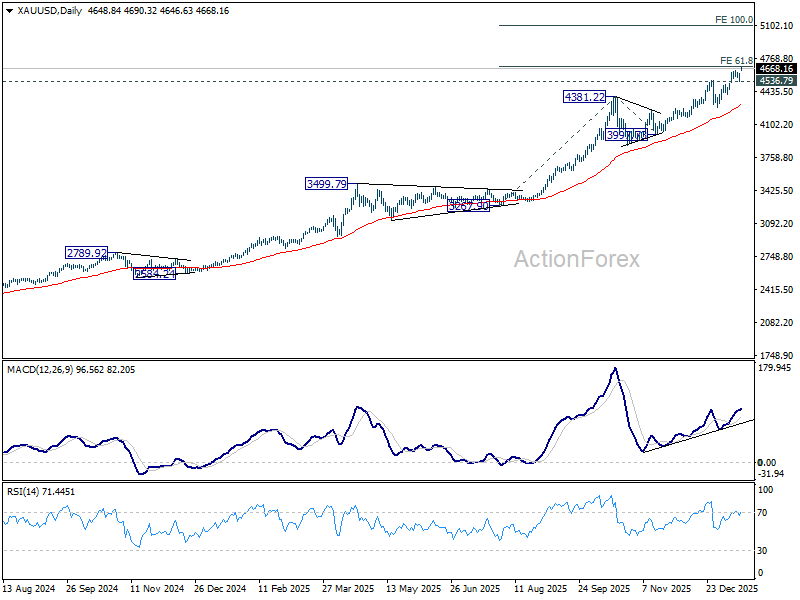

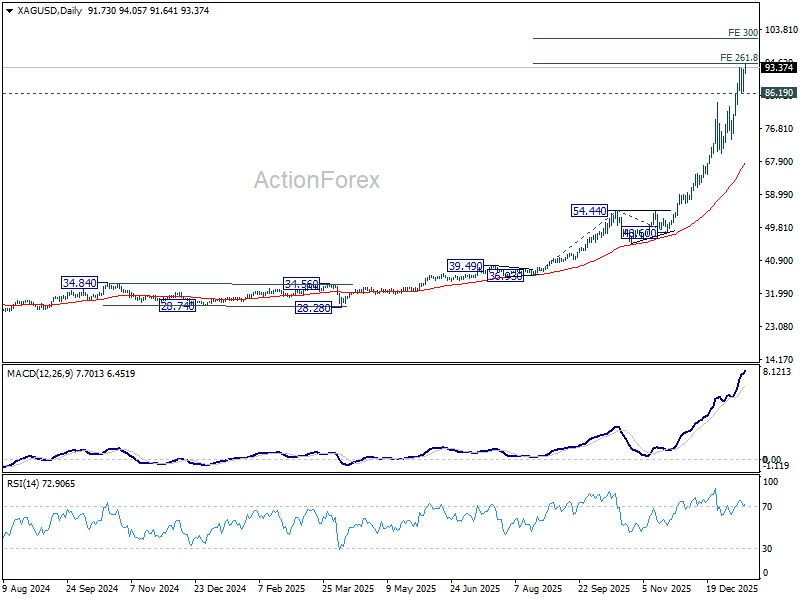

Technically, Gold has already met target of 61.8% projection of 3,267.90 to 4,381.22 from 3,997.73 at 4,685.76. There is no sign of topping, and indeed from 4H MACD, Gold might even be trying to reaccelerate.

Sustained trading above 4,685.76 will pave the way to 5,000 psychological level or even 100% projection at 5,111.05. Nevertheless, break of 4536.79 support will indicate short term topping, and bring consolidations first.

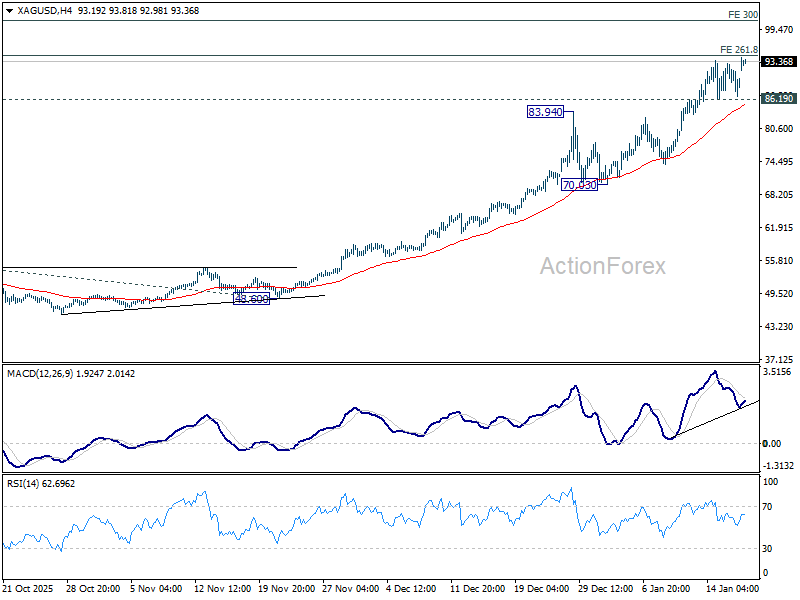

Silver is also just inch below 261.8% projection of 36.93 to 54.44 from 48.50 at 94.34 as the up trend resumes today. Near term outlook will remain bullish as long as 86.19 support holds. Firm break of 94.34 will pave the way to 300% projection at 101.13.

China GDP growth slows to 4.5% in Q4, pressure builds for fresh stimulus

China’s economy slowed at the end of 2025, reinforcing concerns that headline growth masks deepening domestic weakness. GDP expanded 4.5% yoy in Q4, down from 4.8% in Q3, in line with expectations. For the full year, growth reached 5.0%, matching the government’s target, but momentum clearly faded as the year closed.

Officials were quick to acknowledge the strain. Kang Yi, head of the National Bureau of Statistics, described 2025’s performance as “hard-won,” citing persistent challenges from strong supply and weak demand—a combination that continues to weigh on private confidence.

Full-year investment data underscored the depth of the slowdown. Fixed asset investment fell -3.8% ytd yoy, marking the first full-year contraction since the 1990s. The property sector remained the biggest drag, with property investment plunging -17.2% and new construction starts down -20.4%, extending a downturn now in its fourth year. Private investment dropped -6.4%, reflecting weak profit incentives amid overcapacity and cautious households.

December activity data showed mixed signals. Industrial production rose 5.2% yoy, improving from November and beating expectations of 5.0%. But retail sales slowed to 0.9% yoy, missing 1.2% forecasts and reinforcing the message that consumption remains the economy’s main weak spot.

The Q4 slowdown increases pressure on Beijing to step up stimulus in 2026 to meet a growth target of 4.5–5.0%. Without a more decisive pivot toward households and consumption, growth is likely to settle in the low- to mid-4% range, forcing policymakers to confront one of the most persistent domestic demand slumps in decades.

Snap election puts BoJ policy signals under the spotlight

The BoJ’s rate decision is a central focus this week. Consensus remains that the BoJ will hold the policy rate at 0.75%, but confidence around the forward path has been shaken by last week’s sharp market reaction to domestic political developments.

According to a recent Reuters poll, 65 of 67 economists expect the BoJ to keep rates unchanged at both the January and March meetings. At the same time, conviction remains strong that normalization is not finished. Seventy-six percent of respondents see rates reaching at least 1.00% by end-September, with two analysts projecting a move as high as 1.25%.

When asked about timing, expectations are still clustered around mid-year. Among economists who specified a month, July emerged as the most popular choice at 43%, followed by June at 27%. Smaller minorities pointed to April, October, or even January 2027 or later.

However, that outlook shifted abruptly last week after Japanese equities surged and the Yen weakened on reports that Prime Minister Sanae Takaichi plans to dissolve parliament and call a snap election as early as February 8. The move sparked speculation that the BoJ could be forced to act sooner, potentially pulling forward the next rate hike to April.

Still, history cautions against assuming the BoJ will validate market pricing. The central bank has repeatedly shown a willingness to defy consensus expectations, often delivering policy surprises. While an immediate hike this week is not the base case, it cannot be fully ruled out, particularly as the BoJ will publish updated economic and inflation forecasts at this meeting.

More likely, any policy shift would come after the snap election, reducing the risk of political entanglement. Even so, the meeting could mark a turning point through subtle but meaningful changes in forward guidance, either in the statement or during the post-meeting press conference, laying groundwork for a hike that is increasingly viewed as inevitable.

Outside Japan, the UK is another major focus, with labor market data, CPI inflation, and retail sales all due. These releases arrive against a backdrop where the BoE is widely expected to continue easing policy through 2026, but with considerable uncertainty around pace and timing.

Markets currently price two additional 25bp cuts this year, taking Bank Rate from 3.75% to 3.25% by year-end. However, confidence in that path is limited. The Monetary Policy Committee remains deeply divided, with last year’s cuts passing by narrow 5–4 votes, leaving the door open for swift repricing should incoming data tip the balance.

This week’s data are likely to reinforce expectations for the BoE to hold in February, with March seen as the next realistic window for easing. June remains the base case for the final cut of the cycle, though that assumption will remain highly sensitive to inflation persistence and wage dynamics.

From the southern hemisphere, New Zealand’s Q4 CPI and Australia’s employment report take focus. Markets broadly assume both the RBNZ and RBA are done easing. The next phase of debate centers on when hikes start. Risks currently tilt toward Australia moving first, but confirmation will depend more heavily on Australia’s Q4 CPI next week.

Beyond these highlights, markets will also track US PCE inflation, German ZEW sentiment, Japan CPI, Canada’s CPI and retail sales, and PMIs from major global economies.

Here are some highlights for the week:

- Monday: China GDP, industrial production, retail sales, fixed asset investment; Eurozone CPI final; Canada CPI, BoC business outlook survey.

- Tuesday: New Zealand BNZ services; China rate decision; Germany PPI, ZEW; UK employment; Swiss PPI.

- Wednesday: UK CPI, PPI; Canada IPPI, RMPI.

- Thursday: Japan trade balance; Australia employment; US GDP final, personal income and spending; PCE inflation.

- Friday: New Zealand CPI; Australia PMIs; Japan BoJ rate decision, CPI, PMIs; UK retail sales, PMIs; Eurozone PMIs; Canada retail sales; US PMIs.

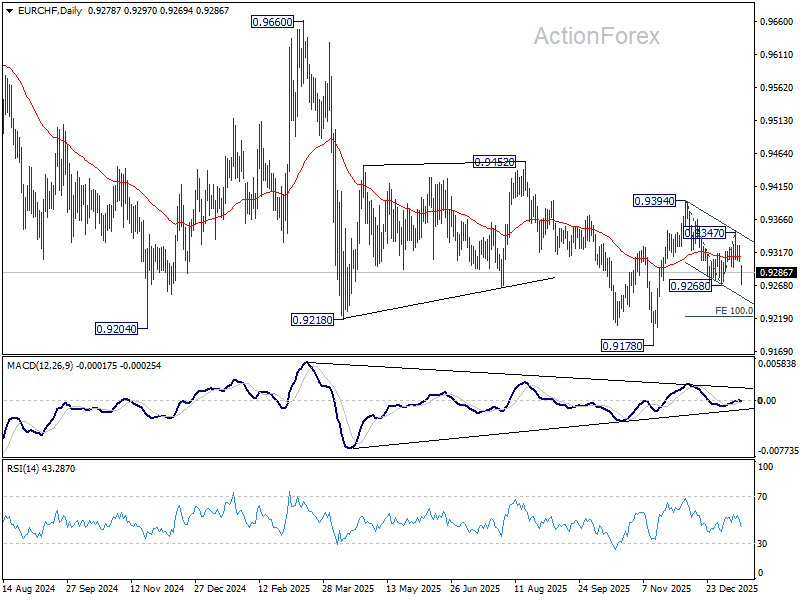

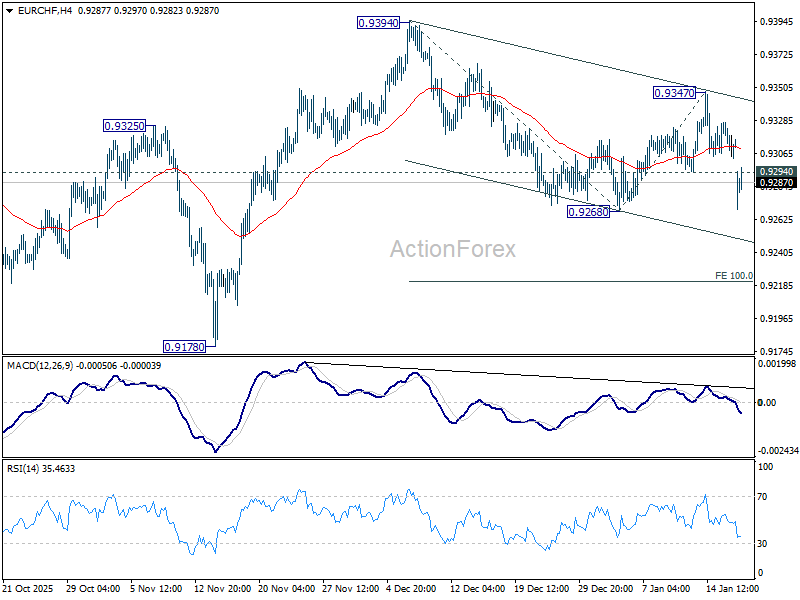

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9301; (P) 0.9315; (R1) 0.9326; More….

EUR/CHF’s steep dive today suggests that corrective recovery from 0.9268 has completed at 0.9347. Intraday bias is back on the downside. Firm break of 0.9268 will resume the fall from 0.9394, and target 100% projection of 0.9394 to 0.9268 from 0.9347 at 0.9221. Break will bring retest of 0.9178 low. For now, risk will stay on the downside as long as 0.9347 resistance holds, in case of recovery.

In the bigger picture, persistent bullish convergence condition in W MACD is a medium term bullish sign. Firm break of 0.9394 resistance should bring sustained trading above 55 W EMA (now at 0.9360). That should indicate medium term bottoming at 0.9178. Further break of 0.9452 resistance will bring stronger medium term rally towards 0.9928 resistance next, even still as a corrective bounce. Nevertheless, rejection by 55 W EMA will retain bearishness for another fall through 0.9178 at a later stage.