{kind=link}

Trading in Asian markets was subdued at the start of the week, with activity dampened by the U.S. holiday and the approach of Lunar New Year. Many regional desks are already lightly staffed, leaving liquidity thin and conviction limited. The holiday mood has kept volatility compressed.

Major currency pairs and crosses are confined within Friday’s ranges, with little appetite to initiate fresh positions ahead of key catalysts. Dollar, Yen, and Euro are all holding steady, while commodity currencies are drifting modestly but without follow-through.

The week ahead, however, offers potential triggers. RBNZ policy decision, FOMC minutes from January meeting, and a heavy slate of UK data including inflation and employment could inject direction back into markets.

Beyond scheduled events, geopolitical developments may prove more consequential. The second round of U.S.–Iran talks in Geneva on Tuesday is drawing attention. The discussions aim to de-escalate tensions over Tehran’s nuclear programme and avert renewed military confrontation.

According to reports, Iran is pursuing an agreement that would provide economic benefits for both sides, including energy and mining investments as well as aircraft purchases. Progress would signal easing geopolitical risk in Middle East.

Any meaningful breakthrough could weigh on oil prices by reducing supply risk premium. In turn, that may spill over into Gold, which has recently been vulnerable after sharp technical selloff. Conversely, stalled negotiations could revive safe-haven demand.

In currency markets, relative performance remains fluid. Aussie is currently the strongest, followed by Loonie and Dollar, while Yen is lagging alongside Swiss Franc and Sterling. Euro and Kiwi are positioned mid-pack. Given the low-liquidity backdrop, these rankings could shift quickly once participation normalizes.

In Asia, at the time of writing, Nikkei is up 0.07%. Hong Kong HSI is up 0.52%. China is on holiday. Singapore Strait Times is up 0.02%. Japan 10-year JGB yield is up 0.001 at 2.214.

Japan sidesteps technical recession as Q4 growth barely grows by 0.1% qoq

Japan’s economy narrowly avoided a technical recession in Q4, but the rebound fell short of expectations. GDP rose just 0.1% qoq, below the 0.4% forecast, though an improvement from Q3’s -0.6% contraction. On an annualized basis, growth came in at 0.2%, recovering from -2.6% but well under the expected 1.6%.

Private consumption, which accounts for more than half of output, edged up 0.1%. Demand for mobile phones provided support, though spending on food and autos declined. External demand was weak, with exports falling -0.3% qoq, dragged down by soft automobile shipments.

Investment provided modest offsets. Business spending rose 0.2%, supported by strong demand for semiconductor-manufacturing equipment, while housing investment jumped 4.8%.

NZ BNZ services falls to 50.9, employment weakness offsets sales strength

New Zealand’s BusinessNZ Performance of Services Index eased from 51.7 to 50.9 in January, slipping further below the survey’s historical average of 52.8. While the index remains marginally in expansion territory, the details reveal a mixed picture. Activity and sales improved from 52.5 to 54.2, but employment deteriorated from 49.6 to 49.1, staying firmly in contraction. New orders edged lower from 52.1 to 51.8, suggesting demand momentum is softening at the margin.

Sentiment remains subdued. The proportion of negative comments rose sharply to 58.7%, up from 50.4% in December and 52.9% in November. Respondents cited seasonal disruptions from Christmas–New Year holidays, fewer enquiries, and a prolonged post-holiday lull. Elevated living and operating costs continue to weigh on business confidence, underscoring fragile recovery conditions.

Still, BNZ Senior Economist Doug Steel struck a more constructive tone, noting that data since late 2025 has reinforced confidence that positive momentum can be sustained. While services growth is hardly robust, the economy appears to be expanding gradually.

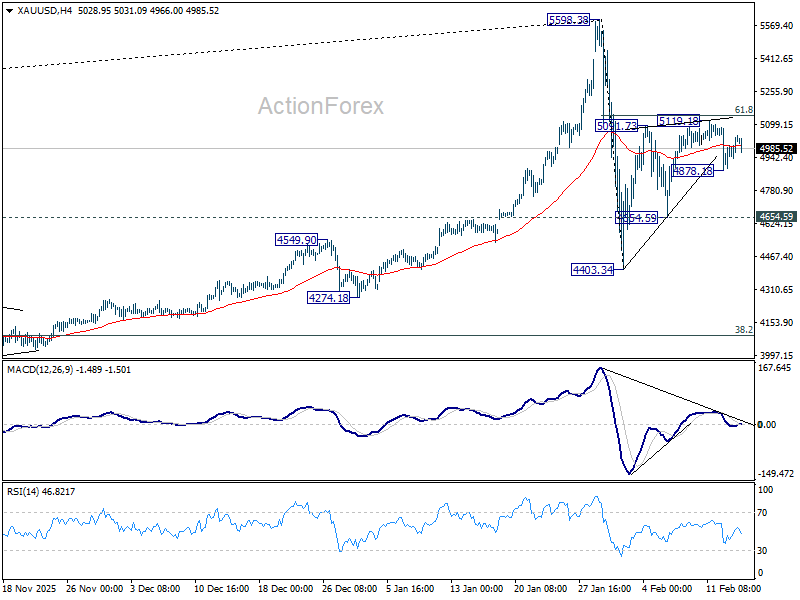

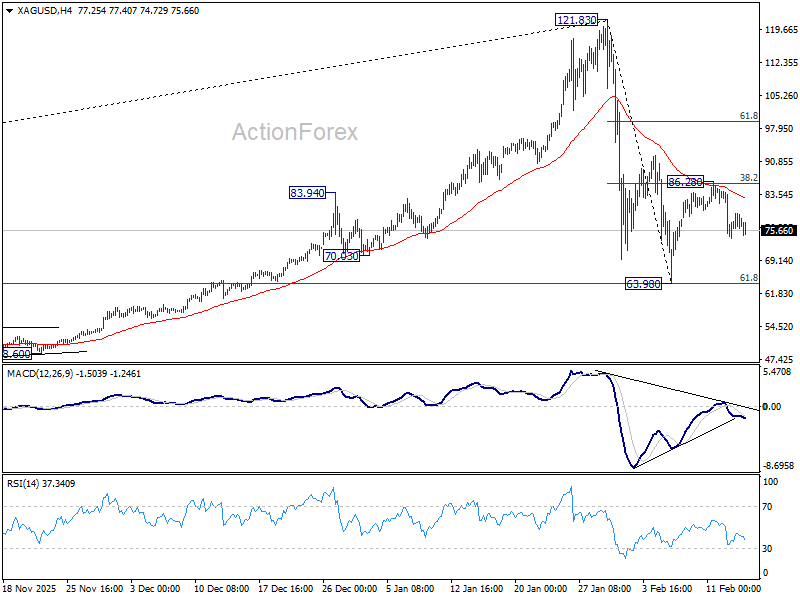

Gold and Silver risk revisiting February lows as corrective rebound fade

Gold and Silver are technically fragile after last week’s sharp mid-week selloff. The subsequent recoveries have lacked conviction, with momentum indicators failing to show meaningful upside traction. Price action suggests sellers remain in control in the near term. A retest of the early February lows now looks increasingly likely, particularly if Dollar stages a more notable rebound.

In broader context, both metals have transitioned into medium-term corrective phases. The powerful, unified macro narrative that fueled last year’s record-breaking rally is no longer present. Instead of a dominant theme like geopolitics or central bank policies, price movements are now more technical and intermarket-driven.

Technically, Gold’s break below its near-term rising trend line raises the risk that rebound from 4,403.34 has already completed at 5,119.18 in a three-wave corrective structure. As long as 5119.18 caps upside, near-term risks remain mildly skewed lower. Break below 4,878.18 temporary low could trigger acceleration toward 4654.59 support. A firm move through that level would open the door for retest of 4,403.34.

Silver shows similar vulnerability. Strong rejection at the 85 resistance zone — where 55 4H MACD rolled over and 38.2% retracement of 121.83 to 63.98 at 85.46 converged — suggests rebound from 63.98 has likely completed at 86.28. Deeper fall would be seen back to retest 63.98. But an immediate break there is not expected. Range trading between 63.98 and 86.28 may dominate in near term before broader decline from 121.83 resumes.

The week ahead: RBNZ hold, Fed minutes, UK CPI, and AU employment

This week’s macro calendar lacks a blockbuster event, but central bank communication and key inflation prints could still shift rate expectations at the margin. RBNZ stands as the only policy meeting, while FOMC minutes, UK CPI, and Australian employment data provide additional catalysts.

RBNZ is widely expected to hold OCR at 2.25%. After an aggressive easing cycle, policymakers are now in prolonged pause mode, allowing prior rate cuts to filter through economy. Growth has shown tentative stabilization, but recovery remains uneven. Inflation rebounded to 3.1% in Q4 from prior quarter, while one-year inflation expectations rose to 2.59%. Although uptick grabbed attention, with spare capacity lingering and unemployment still above average, RBNZ has little urgency to reverse course.

Late 2026 or early 2027 remains base case for an RBNZ rate hike. Guidance on tightening remains premature. However, tone matters. If policymakers sound increasingly confident that recovery is taking hold, markets could begin to price earlier normalization. That would offer near-term support to NZD, particularly against soft Dollar backdrop.

In US, focus shifts to FOMC minutes from January meeting. Rates were left unchanged at 3.50–3.75%, with only Governors Christopher Waller and Stephen Miran dissenting in favor of a cut. Both are well-known doves, so attention will center on broader committee debate.

The key question is whether majority views easing cycle as completed, or merely paused. March hold is effectively locked in, but nuance in discussion could shift June pricing slightly. Markets will parse language around inflation progress and labor market resilience for clues.

UK data calendar is heavier. Employment, wage growth, CPI, and retail sales all arrive as markets increasingly price March rate cut following dovish hold by BoE. Inflation dynamics remain decisive. Any faster-than-expected slowdown would cement expectations for imminent easing. Conversely, sticky wage growth would complicate picture and limit downside for Sterling. Political instability continues to weigh on GBP sentiment, leaving currency sensitive to macro surprises.

Australia’s employment data is another focal point. RBA surprised markets earlier this year by returning to rate hike stance amid renewed inflation pressure. While Q1 CPI remains critical for determining May decision, solid job and wage data would keep tightening bias alive.

Beyond that, Japan GDP, Canada CPI, and flash PMIs from major economies round out calendar.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan GDP; Eurozone industrial production; Canada housing starts, manufacturing sales.

- Tuesday: RBA minutes; Japan tertiary industry index; Germany CPI final; UK employment; Germany ZEW; Canada CPI; US Empire state manufacturing.

- Wednesday: New Zealand PPI; RBNZ rate decision; Japan trade balance; UK CPI, PPI; US durable goods orders; industrial production, FOMC minutes.

- Thursday: Australia employment; Eurozone current account; Canada new housing price index, trade balance; US jobless claims, Philly Fed survey, trade balance.

- Friday: Australia PMIs; Japan PMIs; UK retail sales, PMIs; Eurozone PMIs; Canada retail sales; US GDP revision, personal income and spending, PCE inflation, PMIs.

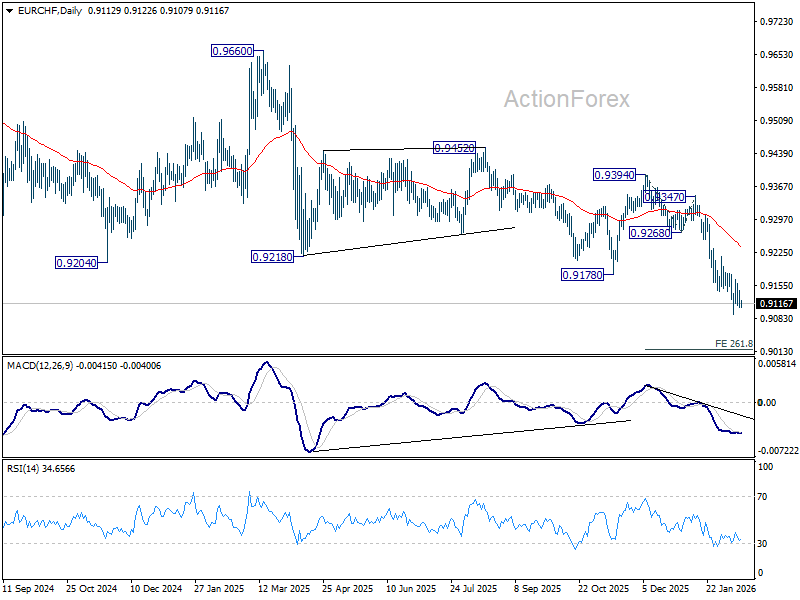

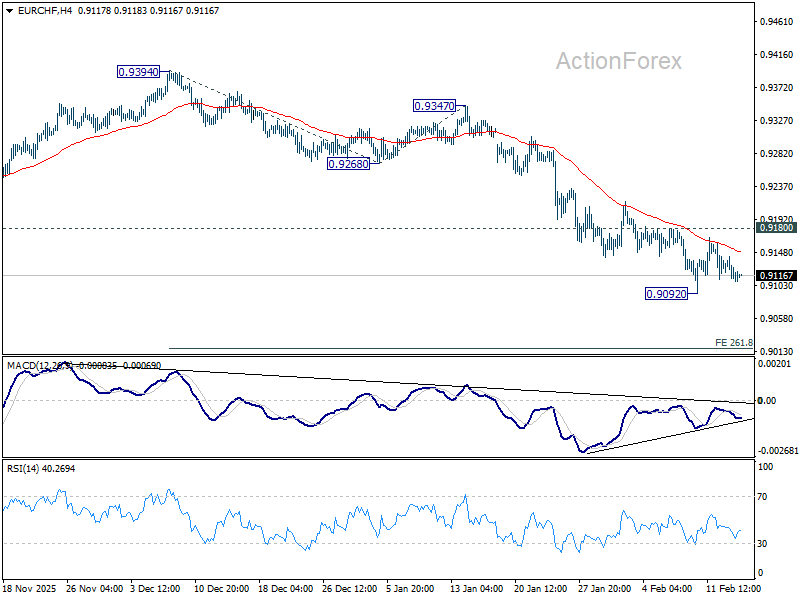

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9099; (P) 0.9122; (R1) 0.9135; More….

EUR/CHF is staying in consolidations above 0.9092 and intraday bias remains neutral. Further decline is expected as long as long as 0.9180 resistance holds. Firm break of 0.9092 will resume larger down trend and target 261.8% projection of 0.9394 to 0.9268 from 0.9347 at 0.9143. However, considering bullish convergence condition in 4H MACD, decisive break of 0.9180 will indicate short term bottoming, and bring stronger rebound towards 55 D EMA (now at 0.9236).

In the bigger picture, down trend from 0.9928 (2024 high) is still in progress with falling 55 W EMA (now at 0.9258) intact. Next target is 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. Outlook will stay bearish as long as 0.9394 resistance holds, in case of recovery.