Global markets extended their recovery today as fears of a catastrophic disruption in global oil supply continued to ease. Asian and European equities rebounded broadly, although US futures were relatively sluggish. WTI crude also remains elevated at around 90 level.

The improvement in sentiment reflects a growing shift in how markets are pricing the conflict. Earlier fears centered on the possibility of a severe supply vacuum if the Strait of Hormuz were effectively shut down. Now, investors appear increasingly confident that global oil flows can be partially maintained through alternative routes and logistical adjustments.

A key development supporting this reassessment came from Saudi Aramco. The company announced it expects to restore roughly 70% of its normal crude shipments within days despite the ongoing disruption to shipping routes in the Gulf region.

Saudi Arabia normally exports about 6.4 million barrels per day. By rerouting supplies through alternative channels, Aramco aims to bring roughly 5 million barrels per day back to the global market almost immediately, significantly reducing the scale of the potential supply shock.

The primary workaround is the East–West Pipeline, also known as the Petroline. The 1,200-kilometer pipeline connects Saudi Arabia’s eastern oil fields with the Red Sea port of Yanbu, allowing shipments to bypass the Strait of Hormuz entirely.

This emergency activation of the pipeline has helped reassure markets that oil exports from the world’s largest crude exporter can continue flowing even while the conflict disrupts traditional shipping lanes.

Nevertheless, Saudi Aramco Chief Executive Amin Nasser warned that the global economy would still struggle to sustain a prolonged closure of the Strait. Global oil inventories are already sitting near five-year lows, leaving limited buffer if disruptions persist.

The easing of supply fears has also triggered a reversal in safe-haven flows across currency markets. Dollar has come under broad pressure as investors unwind defensive positions built during the height of the oil panic.

For the week so far, the Dollar is now among the worst-performing major currencies alongside Japanese Yen and Swiss Franc. Commodity-linked currencies have benefited the most from improving sentiment, with Australian Dollar leading gains, followed by New Zealand Dollar.

Aussie has also been supported by domestic factors after RBA Deputy Governor Andrew Hauser reiterated that the upcoming policy meeting remains “live,” signaling that policymakers will engage in a genuine debate about whether another rate hike may be needed.

In Europe, at the time of writing, FTSE is up 1.20%. DAX is up 1.69%. CAC is up 1.12%. UK 10-year yield is down -0.026 at 4.561. Germany 10-year yield is up 0.013 at 2.875. Earlier in Asia, Nikkei rose 2.88%. Hong Kong HSI rose 2.17%. China Shanghai SSE rose 0.65%. Singapore Strait Times rose 2.19%. Japan 10-year JGB yield closed flat at 2.186.

RBA’s Hauser signals “genuine debate” at March policy meeting

RBA Deputy Governor Andrew Hauser signaled that policymakers face a difficult decision at next week’s board meeting, warning that the recent surge in oil prices is adding new uncertainty to the inflation outlook. Speaking in an interview with The Conversation, Hauser said there will be “a lot for the board to discuss” when it meets later this month.

Hauser emphasized that a “very genuine debate” is likely among board members as they weigh competing risks. While inflation remains too high and rising energy prices could push it higher, policymakers must also consider broader economic conditions. “Inflation is too high. Higher prices don’t help that debate,” Hauser said, adding that arguments exist on both sides of the policy discussion.

The RBA’s current projections already point to headline inflation reaching 4.2% by June, but Hauser acknowledged that the recent oil spike linked to the Middle East conflict could push inflation above that forecast. However, he downplayed the likelihood of inflation climbing as high as 5% in the near term, noting that such projections assume oil prices remain around the USD 100 level.

Hauser stressed that the central bank has not yet updated its formal forecasts and will only revise them in May, after the upcoming policy meeting. For now, the key takeaway is that inflation risks are clearly tilted to the upside.

Australia Westpac consumer sentiment edges Up, but war fears slam late responses

Australia’s Westpac Consumer Sentiment index edged up 1.2% mom to 91.6 in March. While sentiment remains firmly in pessimistic territory, the survey indicates that consumers have responded less negatively than expected to the RBA’s 25 bps increase in February.

However, daily responses collected during the survey week point to steep deterioration in confidence as geopolitical conflicts intensified. According to Westpac, responses gathered in the final three days of the survey were consistent with a much weaker sentiment reading of around 84.

Looking ahead to the RBA’s March 16–17 policy meeting, a rate hike remains possible but is not the base case. While policymakers are likely to be concerned about how rising petrol prices could feed into domestic inflation, the rapidly evolving global situation may encourage caution. Westpac expects the central bank to hold rates steady this month, with the next rate increase more likely to come in May once the external environment becomes clearer.

Australia NAB business confidence turns negative after RBA hike

Australia’s NAB Business confidence fell sharply by five points to -1 February, slipping into negative territory for the first time in eleven months. In contrast, business conditions held steady at +7, roughly in line with the long-run average. The split suggests that firms are still experiencing stable trading conditions but are becoming increasingly cautious about the outlook.

Cost pressures also showed signs of firming again during the month. Labour costs rose to 1.5% on a quarterly equivalent basis. Retail price growth accelerated to 1.0% from just 0.3% previously. The rebound in price indicators suggests that underlying inflation pressures in the business sector may still be present.

The deterioration in sentiment has largely been attributed to the RBA’s 25 basis point rate hike in February to 3.85%, which marked the first increase in two years. NAB analysts noted that the survey only partially captured the subsequent escalation in Middle East tensions and the surge in global energy prices, meaning business confidence could face additional pressure in the months ahead.

China trade surges as exports jump 21.8% and imports beat forecasts

China’s trade activity accelerated sharply in the first two months of 2026, according to data released by the country’s Customs agency. Exports surged 21.8% yoy, far exceeding expectations of a 7.1% increase. Imports climbed 19.8% yoy, also well above the 6.3% consensus forecast.

The stronger-than-expected figures suggest both resilient global demand for Chinese goods and solid domestic consumption of imported materials. China typically combines January and February trade figures to minimize the distortions created by the shifting Lunar New Year holiday period.

Despite the overall strength, trade flows with the US continued to decline. Chinese exports to the U.S. fell about -11% yoy, while imports from the U.S. dropped nearly 27%. In response, Chinese manufacturers have increasingly redirected exports toward emerging markets, particularly Southeast Asia, Africa, and Latin America, highlighting an ongoing reorientation of China’s global trade network.

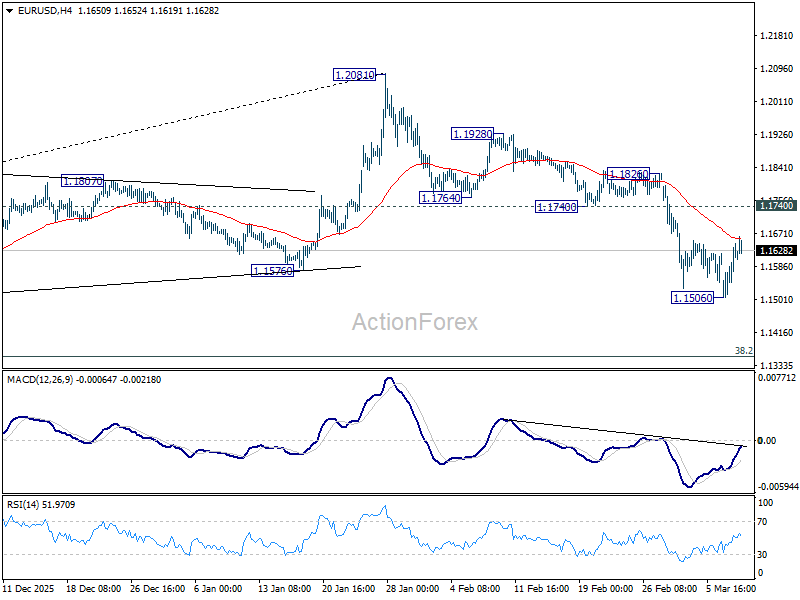

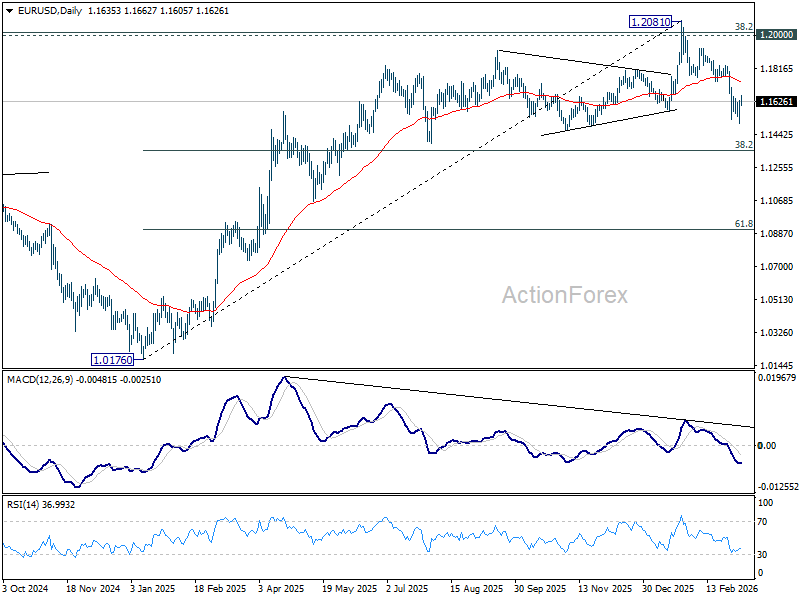

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1548; (P) 1.1594; (R1) 1.1681; More….

EUR/USD’s recovery from 1.1506 continues today, but stays well below 1.1740 support turned resistance. Intraday bias remains neutral, and further decline is still expected. Break of 1.1506 will resume the fall from 1.2081 and target 38.2% retracement of 1.0176 to 1.2081 at 1.1353 next.

In the bigger picture, a medium term top should be in place at 1.2081 on bearish divergence condition in D MACD. Sustained trading below 55 W EMA (now at 1.1500) should confirm rejection by 1.2 key cluster resistance level. That would also raise the chance that whole up trend from 0.9534 (2022 low) has completed as a three wave corrective bounce too. For now, medium term outlook is neutral at best as long as 1.2081 holds, even in case of rebound.

{kind=link}