Market sentiment showed tentative signs of stabilization today as Brent crude slipped back below the psychological $100 per barrel level. The modest pullback in energy prices helped European equities recover from earlier losses while U.S. futures also moved back into positive territory.

However, the shift appears to reflect stabilization rather than a genuine improvement in risk appetite. The underlying geopolitical backdrop remains tense, with no clear end in sight for the Iran war, leaving markets reluctant to fully embrace risk.

Comments from U.S. President Donald Trump reinforced that uncertainty. In a social media post, Trump said the US has “unparalleled firepower, unlimited ammunition, and plenty of time.” Rather than calming markets, the message was interpreted by some investors as a signal that the conflict could drag on for an extended period.

Against this uncertain backdrop, Yen has emerged as the strongest performer in currency markets today. Yet the rally is being driven by a complex set of forces rather than a straightforward safe-haven move. One key factor supporting the yen is rising intervention risk as USD/JPY approaches the psychologically important 160 level, widely seen by markets as a potential line in the sand for Japanese authorities.

Japan’s Finance Minister Satsuki Katayama said today that the government is in “closer contact with U.S. authorities,” while also highlighting the impact of rising crude oil prices on household finances. Such language is typically interpreted as Tokyo seeking tacit approval from Washington for currency intervention.

At the same time, speculation is growing that the Bank of Japan could accelerate its policy normalization path. According to a Reuters report citing sources familiar with the central bank’s thinking, the inflationary impact of Middle East supply shocks may increase the likelihood of another rate hike as soon as April.

Despite Yen’s strength, Dollar is also attracting strong demand. Risk aversion tied to the ongoing Middle East conflict is supporting safe-haven flows into U.S. assets, while fading expectations for Fed rate cuts are further underpinning the greenback.

These opposing forces have effectively trapped USD/JPY in a narrow range. Intervention fears prevent the pair from moving significantly higher, while Dollar strength keeps it from falling decisively. As a result, traders are expressing Yen demand through cross instead. The market is actively selling currencies such as Euro and Pound against Yen, creating a steep decline in Yen crosses even while USD/JPY remains largely unchanged.

Sterling is particularly under pressure following disappointing UK economic data released earlier today. January GDP showed no growth on the month, missing expectations for a 0.2% expansion and reinforcing concerns that the UK economy entered 2026 with limited momentum. For the BoE, with oil prices elevated due to the Iran conflict, the risk of a stagflation scenario—sluggish growth combined with rising energy-driven inflation—has become a central concern for policymakers.

Loonie is also underperforming after a sharply weaker labor market report. Employment plunged by -83.9k in February, far worse than expectations for a modest increase, while the unemployment rate rose to 6.7%. The sudden deterioration in employment conditions raises questions about the underlying strength of the Canadian economy. The BoC is widely expected to remain on hold next week, but today’s data increases the risk that policymakers may eventually need to consider additional support if labor market weakness persists.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.20%. CAC is up 0.02%. UK 10-year yield is up 0.003 at 4.716. Germany 10-year yield is down -0.010 at 2.951. Earlier in Asia, Nikkei fell -1.16%. Hong Kong HSI fell -0.98%. China Shanghai SSE fell -0.82%. Singapore Strait Times fell -0.27%. Japan 10-year JGB yield rose 0.057 to 2.245.

US core PCE rises 0.4% mom in January as consumer spending stays strong

US inflation data for January presented a mixed picture, with price pressures remaining firm even as the headline annual pace eased slightly. The headline PCE price index rose 0.3%om, while the core measure—which excludes food and energy—increased by 0.4% min. Both readings matched market expectations and indicate that underlying inflation remains somewhat sticky.

On an annual basis, headline PCE inflation slowed modestly from 2.9% to 2.8%, coming in slightly below forecasts. However, core inflation edged higher from 3.0% to 3.1% year-on-year, highlighting persistent price pressures in the broader economy and reinforcing the view that the disinflation process remains uneven.

Consumer demand remained resilient during the month. Personal spending increased by USD 81.1B, or 0.4% mom, exceeding expectations of 0.3% mom. Meanwhile, personal income rose by USD 113.8B, also translating into a 0.4% monthly gain but falling slightly short of 0.5% mom forecasts.

Canada jobs plunge -83.9k in February as unemployment rate climbs to 6.7%

Canada’s labor market suffered a sharp setback in February, with employment plunging by -83.9k, far worse than expectations for a modest gain of around 10k. The decline marks a significant deterioration in labor conditions.

The drop in employment was broad-based across sectors. Services-producing industries shed around -56k jobs, while goods-producing sectors lost roughly -28k positions. The deterioration pushed the unemployment rate higher to 6.7% from 6.5%, while the participation rate edged down slightly to 64.9%.

Despite the sharp decline in employment, wage growth accelerated noticeably. Average hourly wages rose 3.9% yoy in February, up from 3.3% in January.

Eurozone industrial production drops -1.5% mom as manufacturing weakness deepens

Eurozone industrial production fell sharply in January, highlighting renewed weakness in the region’s manufacturing sector. Output declined by -1.5% month-on-month, well below expectations for a 0.7% increase, suggesting that industrial momentum at the start of 2026 was significantly weaker than anticipated.

The decline was broad-based across most categories. Production of intermediate goods dropped by -1.9%, while capital goods output fell by -2.3%. Durable consumer goods production also declined by -1.9%, and non-durable consumer goods saw the steepest fall with a -6.0% drop. Energy output was the only bright spot, rising by 4.7% during the month and partially cushioning the overall decline.

Across the broader European Union, industrial production fell by -1.6% month-on-month. Ireland recorded the largest contraction with a -9.8% drop, followed by Luxembourg (-4.3%) and Sweden (-4.1%). In contrast, a few smaller economies posted gains, with Portugal leading the increases at +4.2%, followed by Latvia (+3.3%) and Lithuania (+2.7%).

UK GDP flat in January as services stall, production contracts

UK economic growth stalled at the start of the year, with GDP showing no expansion in January, falling short of expectations for a modest 0.2% mom rise. Sector data showed a mixed picture beneath the headline reading. Services output, which accounts for the largest share of the UK economy, was flat during the month. Production declined slightly by -0.1%

Construction posted 0.2% mom growth, but the sector remains under sustained pressure following a prolonged period of contraction driven by high borrowing costs and subdued investment.

Looking at the broader trend, the UK economy still managed a modest expansion of 0.2% in the three months to January, an improvement from the 0.1% growth recorded in the three months to December. Services output rose by 0.2% over the period, while production delivered stronger growth of 1.3%. However, construction was a significant drag, contracting by -2.0% over the same period.

New Zealand BNZ manufacturing holds firm at 55 in February

New Zealand’s manufacturing sector continued to expand in February, with BusinessNZ Performance of Manufacturing Index edging slightly lower from 55.1 to 55.0. While the headline reading dipped marginally, the index remains comfortably above the 50 breakeven level, signaling ongoing growth in the sector.

Underlying components showed mixed but generally positive trends. Production rose modestly from 56.5 to 56.7, while new orders strengthened from 56.6 to 57.6, indicating improving demand conditions. Employment, on the other hand, fell notably from 52.6 to 50.4.

Survey responses pointed to improving business sentiment, with the share of positive comments rising to 55.5% in February from 47.7% in January. Manufacturers reported stronger orders, enquiries, and sales, helped by firmer export demand and improving conditions across certain sectors.

BNZ Senior Economist Doug Steel noted that while geopolitical tensions in the Middle East are dominating market attention, February’s PMI reading provides a solid starting point for the manufacturing sector heading into an uncertain global environment.

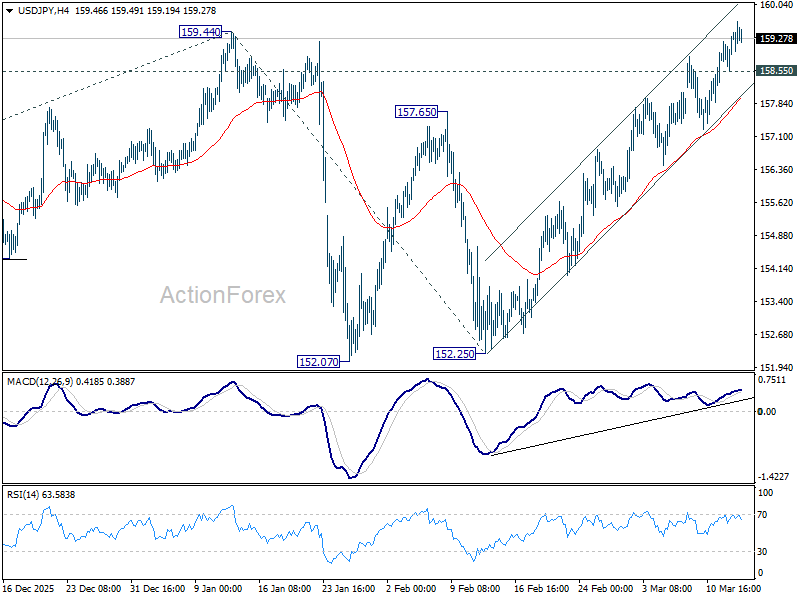

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 158.81; (P) 159.12; (R1) 159.67; More…

Intraday bias in USD/JPY remains on the upside at this point. rise from 139.87 is resuming and should target a retest on 161.94 high. Firm break there will confirm larger up trend resumption. Next target is 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34. On the downside, below 158.55 minor support will turn intraday bias neutral first.

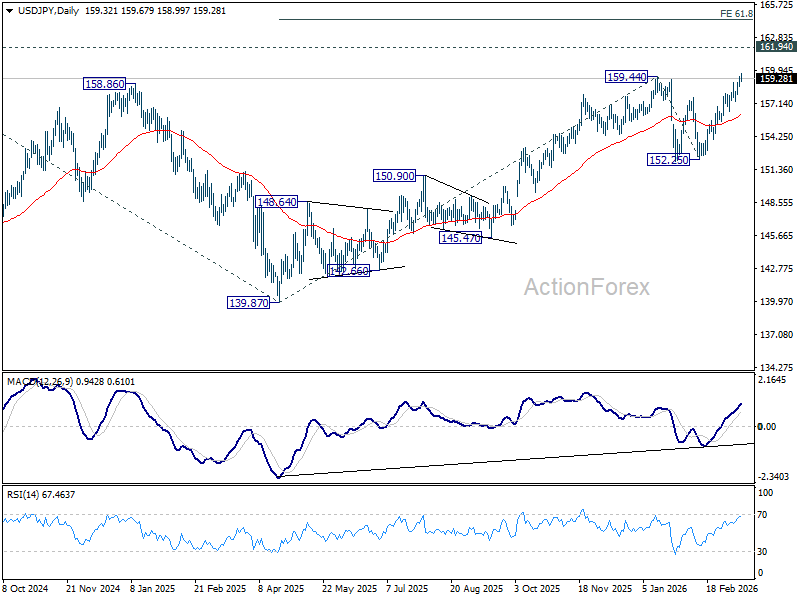

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 152.16) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

{kind=link}