ECB rate hike expectations are gaining traction in markets, with growing speculation that tightening could begin as early as April. Major institutions including Barclays and J.P. Morgan are now forecasting an initial move next month, followed by additional hikes in June and July, reflecting a rapid shift in policy expectations amid rising inflation risks.

Other banks remain slightly more cautious on timing but not direction. Morgan Stanley and Deutsche Bank both expect hikes starting in mid-year, while Goldman Sachs’ adverse scenario outlines a cumulative 75bps tightening path, with the possibility that April could still mark the beginning if energy-driven inflation intensifies further.

This repricing comes even as the ECB kept its deposit rate unchanged at 2.00% in the latest meeting. However, the updated projections told a different story, with 2026 inflation revised up to 2.6% while growth was cut sharply to 0.9%. This marks a clear shift away from the previous “goldilocks” environment toward a more challenging stagflation backdrop.

The ECB’s communication also underscored this transition. By publishing adverse and severe scenarios, policymakers effectively signaled readiness to act if energy prices remain elevated. The message was clear: while the baseline does not yet justify an immediate hike, contingency plans are firmly in place.

Within the Governing Council, three distinct camps have emerged. The hawks, led by Bundesbank President Joachim Nagel, are increasingly concerned about inflation expectations becoming unanchored and have openly warned that a more restrictive stance may soon be required.

In contrast, centrists such as France’s Francois Villeroy de Galhau and Finland’s Olli Rehn are urging caution. They emphasize the need to avoid overreacting to supply-side shocks, arguing that short-term energy-driven inflation should not automatically trigger aggressive tightening.

Meanwhile, the data-dependent camp, represented by Spain’s Jose Luis Escriva, continues to advocate a meeting-by-meeting approach. This group highlights the high degree of uncertainty surrounding the persistence of the energy shock and its transmission into core inflation.

Despite these internal divisions, markets are clearly leaning toward the hawkish interpretation. The shift in rate expectations has provided support for the Euro, which is among the stronger performers this week, particularly against the Swiss Franc.

The Franc’s weakness is partly policy-driven, as the SNB has stepped up its intervention rhetoric to prevent excessive appreciation. This has created a favorable backdrop for EUR/CHF, amplifying Euro strength beyond what ECB expectations alone would justify.

However, against the Dollar, the Euro’s gains remain more tentative. Price action is still capped below key resistance levels, suggesting the move may be corrective rather than the start of a sustained uptrend. For a more decisive shift, The market might need to see the ECB actually step closer to execute one of those 25 bps hikes.

In Europe, at the time of writing, FTSE is up 0.10%. DAX is up 0.07%. CAC is up 0.19%. UK 10-year yield is up 0.085 at 4.869. Germany 10-year yield is up 0.01 at 2.973. Earlier in Asia, Japan was on holiday. Hong Kong HSI fell -0.88%. China Shanghai SSE fell -1.24%. Singapore Strait Times fell -0.38%.

Canada retail sales rise 1.1% mom but miss expectations

Retail sales rose 1.1% in January, missing forecasts, but core spending remained firm with solid gains in general merchandise. February data points to continued steady momentum. Read more.

EU trade contracts sharply, US exports drag

Eurozone trade weakens: Exports fell -7.6% yoy, imports -7.3% yoy, resulting in a EUR 1.9B deficit; intra-Eurozone trade also declined, signaling soft internal demand. Read more.

NZ exports hit by soft China and Japan demand

NZ’s trade balance slipped into deficit as exports to China and Japan declined while imports surged. Soft Asian demand and rising external imbalance could weigh further on NZD. Read more.

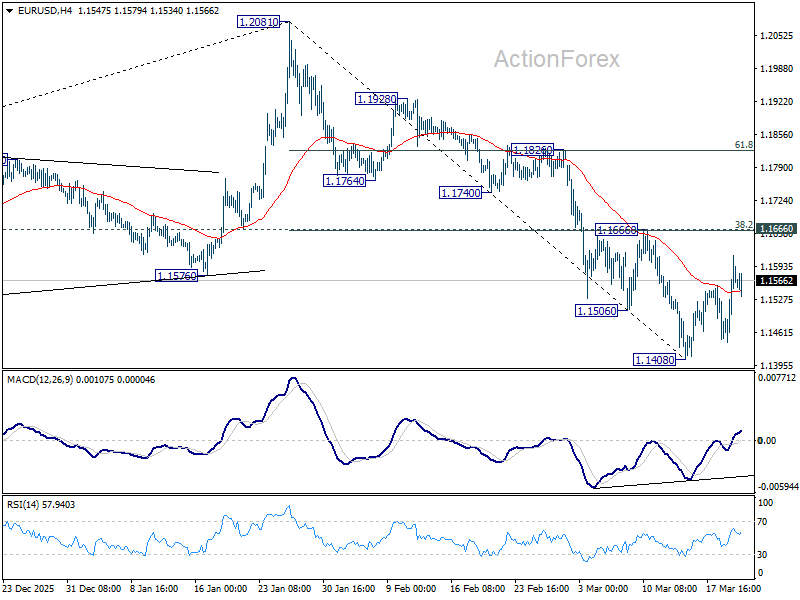

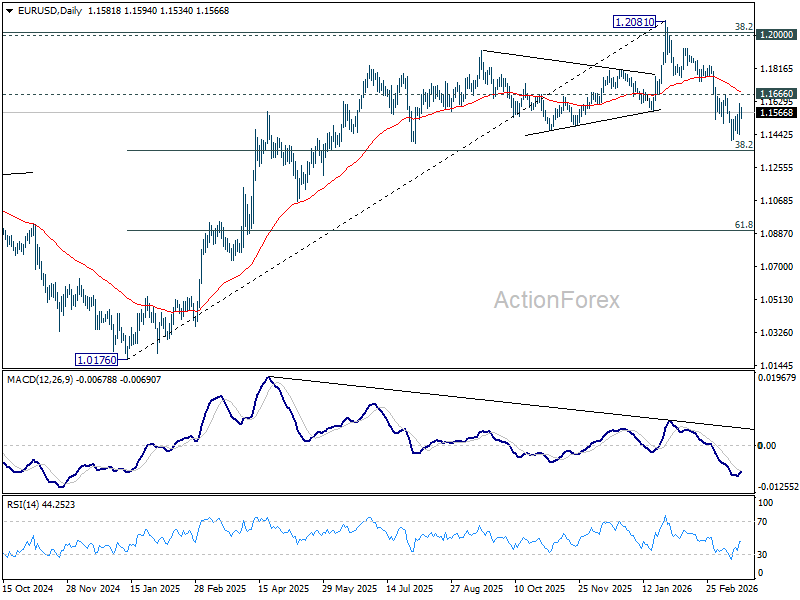

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1488; (P) 1.1518; (R1) 1.1570; More….

EUR/USD is still bounded in established range trading and intraday bias remains neutral. Further decline is in favor as long as 1.1666 resistance holds. On the downside, below 1.1408 will resume the fall from 1.2081 to 38.2% retracement of 1.0176 to 1.2081 at 1.1353. However, decisive break of 1.1666 will argue that the fall from 1.2081 has completed, and turn bias back to the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824.

In the bigger picture, the break of 55 W EMA (now at 1.1495) confirms rejection by 1.2 key cluster resistance level. The whole up trend from 0.9534 (2022 low) might have completed as a three wave corrective rise too. In either case, deeper fall is now expected to long term channel support (now at 1.0528. Risk will stay on the downside as long as 1.2081 holds, in case of recovery.

{kind=link}