The global financial markets are treading water as the Hormuz reopening deadline looms, with U.S. Donald Trump warning of severe escalation if Iran does not comply. The mood across financial markets is one of “calculated dread,” as investors await a decisive signal while avoiding aggressive positioning. Equities are mixed, currencies largely range-bound, and volatility subdued.

At the center of this tension is the deepening deadlock over the control of the Strait of Hormuz. Diplomatic efforts have failed to gain traction, and both sides appear entrenched, leaving little room for a near-term resolution. For markets, the focus remains on one key variable—oil. Crude prices are now the ultimate trigger for how this conflict is interpreted.

A decisive break above the 120 escalation threshold in both WTI and Brent would imply that traders are beginning to factor in a structural, permanent loss of supply from the roughly 20 million barrels per day that typically flow through the Strait. This would mark a transition toward generational energy risk, with far-reaching implications.

In that scenario, Treasury yields would likely surge alongside Dollar. This is not just a traditional safe-haven move. Instead, higher yields would reflect expectations that central banks must keep policy tight to combat energy-exported inflation.

Conversely, for markets to price out the war premium, oil would need to fall decisively below 100. Anything above that level suggests that uncertainty remains elevated and that markets are still in a “wait-and-see” mode.

While markets remain focused on immediate price signals, the broader economic outlook is already deteriorating. IMF Managing Director Kristalina Georgieva warned that the conflict has triggered the worst disruption in global energy supply on record. Even in the event of a swift resolution, the IMF expects the stagflationary effects to stay. “All roads now lead to higher prices and slower growth,” said Georgina.

Recent data is already validating this shift. Eurozone Sentix sentiment has plunged, with recession risks re-emerging and inflation concerns accelerating. PMI data points to a rising risk of GDP contraction in Q2, while UK surveys show the sharpest input cost inflation in nearly a year.

This raises a critical question: even if the conflict is resolved quickly, can the economic damage be reversed? The answer increasingly appears to be no. The destruction of infrastructure and the erosion of trust mean energy markets may remain tight for an extended period. In this context, markets are not just reacting to current events—they are adjusting to a structural shift. The era of cheap energy may be ending, and oil’s next move will determine how quickly that reality is priced in.

In the currency markets, Aussie is the strongest performer so far this week, followed by Euro and Sterling. At the other end, Yen is the weakest, trailed by Dollar and Swiss Franc, while Loonie and Kiwi sit in the middle. However, this ranking offers limited signal at this stage, as positioning remains fluid and could shift sharply in the coming hours depending on developments around the Hormuz deadline and oil price reaction.

In Europe, at the time of writing, FTSE is up 0.03%. DAX is down -0.06%. CAC is up 0.42%. UK 10-year yield is up 0.021 at 4.798. Germany 10-year yield is up 0.044 at 3.040. Earlier in Asia, Nikkei rose 0.03%. Hong Kong was on holiday. China Shanghai SSE rose 0.26%. Singapore Strait Times fell -0.29%. Japan 10-year JGB yield fell -0.022 to 2.410.

Gold Price Eyes 4,500 Springboard as Break Above 4,800 Targets 5,000+

A dip toward 4500 may confirm a springboard setup for Gold, but sustained gains toward 5000+ depend on a break above 4800 and lower yields. Read More.

Eurozone Sentix Slumps as Recession Risk Returns and Inflation Fears Surge

Eurozone sentiment has taken a sharp hit as Sentix data points to rising recession risk and a fresh surge in inflation concerns. With oil above $110 and supply disruptions intensifying, investors are bracing for a stagflationary environment. Read More.

Eurozone PMI Signals Rising Q2 GDP Contraction Risk as War Shock Hits Growth

Eurozone growth is nearing a stall, with PMI data pointing to rising Q2 GDP contraction risk as energy shock, weak demand, and supply disruptions take hold. With inflation rising at the same time, stagflation risks are building quickly. Read More.

UK PMI Signals Economic Growth Slowdown and Sharp Inflation Surge

UK growth is slowing sharply while inflation is accelerating, with PMI data pointing to rising stagflation risks as energy costs surge and demand weakens. With confidence falling, the outlook is becoming increasingly fragile. Read More.

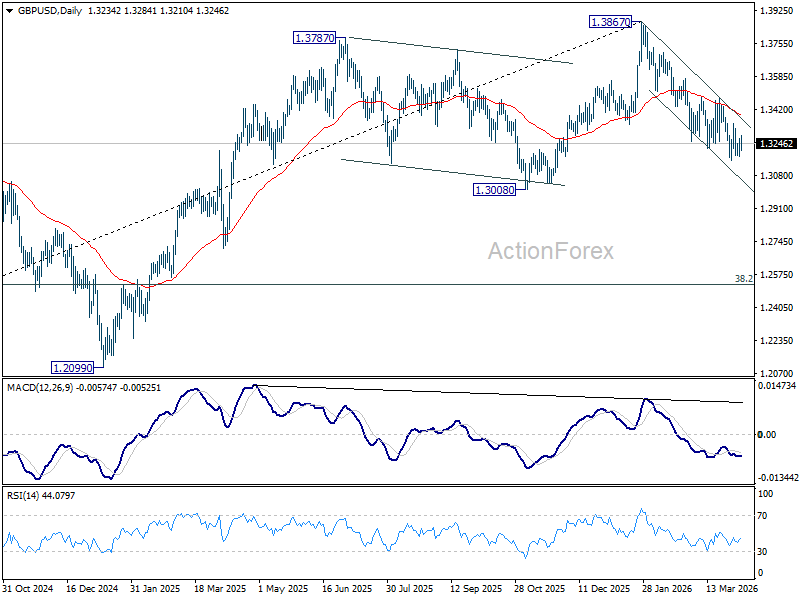

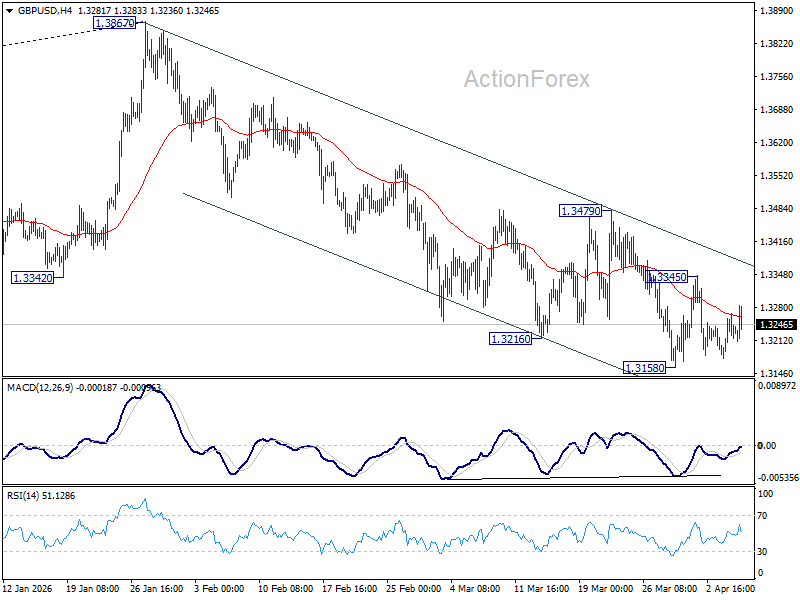

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3187; (P) 1.3228; (R1) 1.3278; More…

GBP/USD is still bounded in range trading and intraday bias remains neutral. With 1.3479 resistance intact, further decline is still in favor. Below 1.3158 will resume the fall from 1.3867 to 1.3008 structural support. However, firm break of 1.3479 will indicate that the fall from 1.3867 has completed, and turn bias back to the upside for stronger rally.

In the bigger picture, considering bearish divergence condition in both D and W MACD, a medium term top should be in place at 1.3867. Firm break of 1.3008 support will argue that fall from 1.3867 is at least correcting the rise from 1.0351 (2022 low) with risk of bearish reversal. That would open up further decline to 38.2% retracement of 1.0351 to 1.3867 at 1.2524. For now, medium term outlook will be neutral at best as long as 1.3867 resistance holds, or until further development.

{kind=link}