Dollar is coming under renewed pressure as traders move to lighten long positions ahead of the FOMC meeting this week. The move reflects reluctance among traders to hold long USD exposure into an event that is seen as carrying downside risks for the currency.

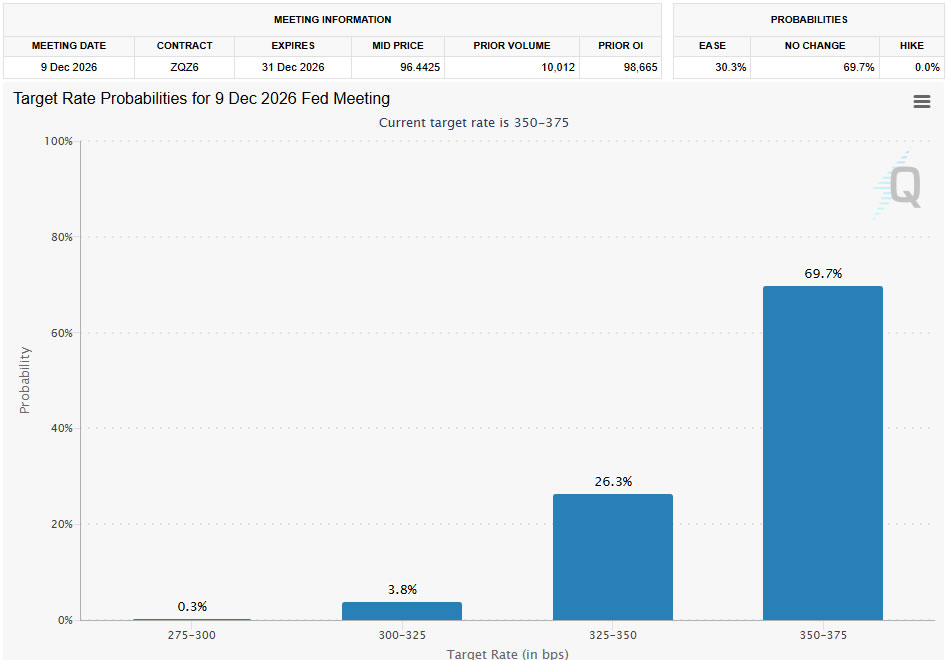

The outcome of the meeting is largely a foregone conclusion, with rates expected to remain unchanged at 3.50%–3.75%. Rather than expecting a policy surprise, markets are focused on the risk of a less-hawkish message that could also be interpreted as a dovish tile. .

The inflation backdrop is central to this shift. Headline CPI rose from 3.0% to 3.3% in March, but the increase was driven almost entirely by a 10.9% surge in energy costs. Core CPI, by contrast, eased from 2.8% to 2.6%, reinforcing the argument that underlying inflation pressures are still relatively contained.

This distinction allows the Fed to treat the recent inflation spike as transitory. With oil prices stabilizing at elevated levels rather than accelerating further, the urgency for a hawkish shift has diminished.

Labor market signals add to the case for caution. The sharp contrast between strong hiring in January/March and deep contraction in February highlights ongoing volatility, while the broader picture suggests a low hiring, low firing environment. This suggests a fragile equilibrium, where the Fed may prefer to avoid aggressive policy moves that could disrupt stability.

Market pricing reflects this outlook clearly. Fed funds futures are assigning virtually no probability to a rate hike this year, while indicating around a 30% chance of a cut by the end of the year.

Meanwhile, the updated projections will also be key. Inflation forecasts are likely to be revised higher in the short term, while growth projections may be trimmed. The net result could be a dot plot that still points to one rate cut this year—hardly a hawkish signal.

The leadership transition adds another dimension to the story. As Powell prepares to hand over to Kevin Warsh on May 15, markets expect him to avoid setting a new policy direction at this stage. A balanced tone, intended to leave flexibility for the incoming chair, could instead be interpreted as confirmation that the Fed is moving away from a hawkish stance.

In FX markets, the reaction is already clear—Dollar is the weakest performer of the day so far, while Kiwi and Aussie lead gains, followed by Euro, reflecting a broader shift toward risk-sensitive currencies.

In Europe, at the time of writing, FTSE is down -0.27%. DAX is up 0.49%. CAC is up 0.14%. UK 10-year yield is down -0.176 at 4.985. Germany 10-year yield is up 0.024 at 3.022. Earlier in Asia, Nikkei rose 1.38%. Hong Kong HSI fell -0.20%. China Shanghai SSE rose 0.16%. Singapore Strait Times fell -0.61%. Japan 10-year JGB yield rose 0.0387 to 2.479.

ECB Survey Signals Inflation Reacceleration Risk as Firms Lift Price and Cost Expectations

Eurozone firms are raising prices again. The ECB’s SAFE survey shows a sharp jump in selling price and cost expectations following the Middle East energy shock, while wages remain contained—signaling a renewed inflation pulse with limited second-round effects. Read More.

German Consumer Confidence Sinks to Two-Year Low as Inflation and War Fears Hit Sentiment

German consumer sentiment is deteriorating sharply, with the GfK index falling to its lowest level since 2023. Inflation is crushing income expectations while geopolitical tensions linked to Iran are darkening the economic outlook, raising fresh concerns over consumption and growth. Read More.

Oil Stalls as ‘Frozen Conflict’ Replaces Escalation Fears in US–Iran Standoff

Oil trades in a tight range as US–Iran tensions enter a “frozen conflict” phase. With Brent testing key near term channel resistance and traders reluctant to chase headlines, the next directional move will depend on a break above $110 or rejection lower. Read More.

AUD/JPY Eyes Breakout Toward 120 as BoJ Decision and Australia CPI Set Up High-Stakes Week

AUD/JPY is approaching a breakout point as BoJ policy and Australia CPI set the tone for the week. With yen weakness risks rising and inflation expected to accelerate, the pair could push toward 120 if key catalysts align. Read More.

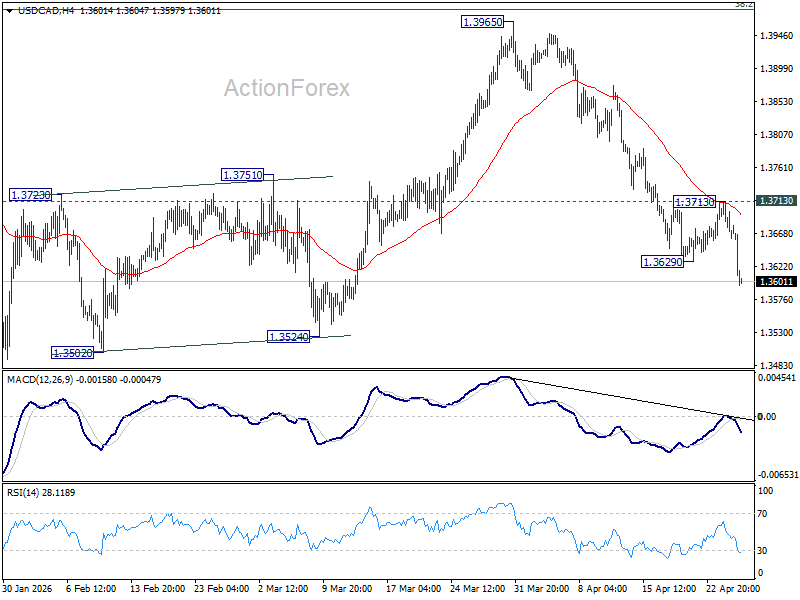

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3651; (P) 1.3683; (R1) 1.3705; More…

USD/CAD’s fall from 1.3965 resumed by breaking through 1.3629 temporary low. Intraday bias is back on the downside for retesting 1.3480 low. Firm break there will resume larger down trend. For now, risk will stay on the downside as long as 1.3713 resistance holds, in case of recovery

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

{kind=link}