The forex market are starting to ignore economic data release today and tread water, just ahead of long weekend. Dollar is trading in black across the board for the week. But better than expectation job data doesn’t the greenback a boost to extend its rally. Canadian Dollar also shrugs off worse than expected GDP data and stays as the second strongest for the week. Meanwhile, Yen and Swiss France are the weakest.

US jobless claims dropped to lowest since 1973, Canada GDP missed expectations

US personal income rose 0.5% in February, spending rose 0.2% and both met expectations. Headline CPI accelerated to 1.8% yoy while core PCE also accelerated to 1.6% yoy. Initial jobless claims dropped -12k to 215k in the weekended March 254. That’s notably below expectation of 231k. That’s also the lowest level since January 1973. Four week moving average of initial claims dropped 0.5k to 224.5k. Continuing claims rose 35k to 1.87m in the weekended March 17.

Canadian data are generally disappointingly. GDP contracted -0.1% mom in January versus expectation of 0.1% mom. IPPI rose 0.1% mom in February versus expectation of 0.4% mom. RMPI dropped -0.3% mom versus expectation of 2.8% mom rise.

Philadelphia Fed Harker expects three hikes this year on “some firming of inflation”

Philadelphia Fed President Patrick Harker said in a WSJ interview that he now expects three Fed rate hike this year. Harker is seen as on the dovish side of the spectrum as he previously projected just two hikes in 2018. He pointed to “some firming of inflation” as he reason for the upgrade is his own forecast. He also clarified that he placed more emphasis on inflation than fiscal policy. Nonetheless, Harker also sounded cautious on trade tensions. He noted that risk of increasing trade tariffs as a source of uncertainty for both economic projections and monetary policy.

ECB Knot: Market expectations and ECB policy actions converged into a “sweet spot”

ECB Governing Council member, Dutch central bank Governor Klaas Knot talked about monetary policy as he presented his bank’s annual report in Amsterdam today. He emphasized that the top priority for ECB now is to “normalize monetary policy and strengthen the economic and monetary union”. And, market expectations of ECB’s policy action “have more or less converged at what I call a sweet spot”, with ” a fair degree of consensus around these expectations.”Therefore, the likelihood of being “too cautious” is a bit larger than being “too bold”.

Regarding trade relationship with the US, he said “he question is if Europe will come with countermeasures which could make us slip into a trade war.” But he also emphasized that ” if the US were to implement trade restrictions on say steel, it will be the American consumer paying the price.”

Released from Eurozone, German unemployment dropped -19k to 2.373m in March, more than expectation of -15k. Unemployment rate dropped from 5.4% to 5.3%, met expectation. That’s also the lowest level on record. Also from Germany, CPI rose 0.4% mom, 1.6% yoy in March, up from prior’s 1.4% yoy but missed expectation of 1.7% yoy.

Swiss KOF: Dropped but still indicates above average growth

Swiss KOF economic barometer dropped to 106.0 in March, down from 108.4, below expectation of 107.2. KOF noted in the release that “notwithstanding this decline, the present position is still on a level clearly above its long-term average.” This indicates that in the near future the Swiss economy should continue to “grow at rates above average”.

UK Gfk Consumer Confidence: Definitely a movement in the right direction

UK Gfk consumer confidence rose to -7 in March, up from -10 and above expectation of -10. All five of the constituent measures recorded higher values. Personal financial situation over the past 12 months rose 3 pts to 3. Personal financial situation over next 12 months rose 5 pts to 10. General economic situation over the last 12 month rose 3 pts to -26. General economic situation over next 12 months rose 4 pts to -22. Major purchase index rose 2 pts to 2. Saving index rose 1 pt to 13.

Gfk noted in the release that “the prospect of wage rises finally outstripping declining inflation, high levels of employment with low-level interest rates, and finally some movement on the Brexit front appear to have boosted our spirits.” While it’s “still a little early to be talking about green-shoots”, “this is definitely a movement in the right direction”.

Also from UK, Q4 GDP was finalized at 0.4% qoq, unrevised. Current account deficit narrowed to GBP -18.4b in Q4. Index of serves rose 0.6% 3mo3m in January. M4 money supply dropped -0.4% mom in February. Mortgage approvals dropped to 64k in February.

Japan at beginning of consumer spending recovery

Japan retail sales rose 0.4% mom, 1.6% yoy in February, slightly higher than expectation of 0.6% mom, 1.7% yoy. And it’s marked improvement from January’s -1.6% mom, 1.5% yoy. It’s noted that consumer spending could be at the beginning of mild recovery. Improvement is also seen lately in the labor market. Overall picture suggests that consumption is going to pick up momentum. And that should eventually help lift inflation. But for now, core inflation is still way off BoJ’s 2% target and it will take some more time for BoJ to start considering stimulus exit.

Japan FM Aso: No bilateral trade negotiations with US

Japan finance minister Taro Aso said in the parliament that historically, US Dollar always rise against Japanese Yen when interest rate differentials widened to 3%. Aso added that US interest rates will “undoubtedly rise ahead”. And therefore, there won’t be “one-sided” Yen appreciation that could hurt the economy.

Regarding trade, Aso emphasized that Japan should “definitely avoid” bilateral trade negotiations with the US. He added that “When two countries negotiate, the stronger country gets stronger. That’s unnecessary (for Japan) so we’ve been saying all along that we would definitely avoid” bilateral trade talks with the United States.

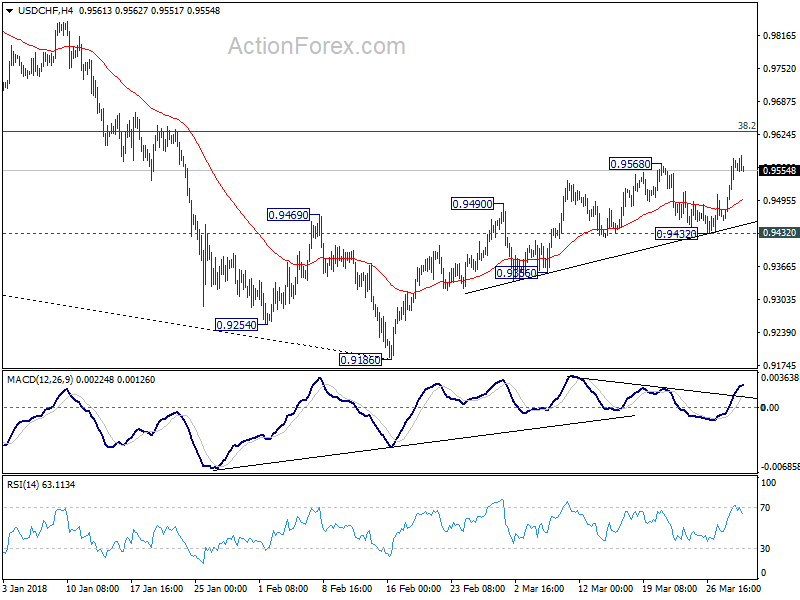

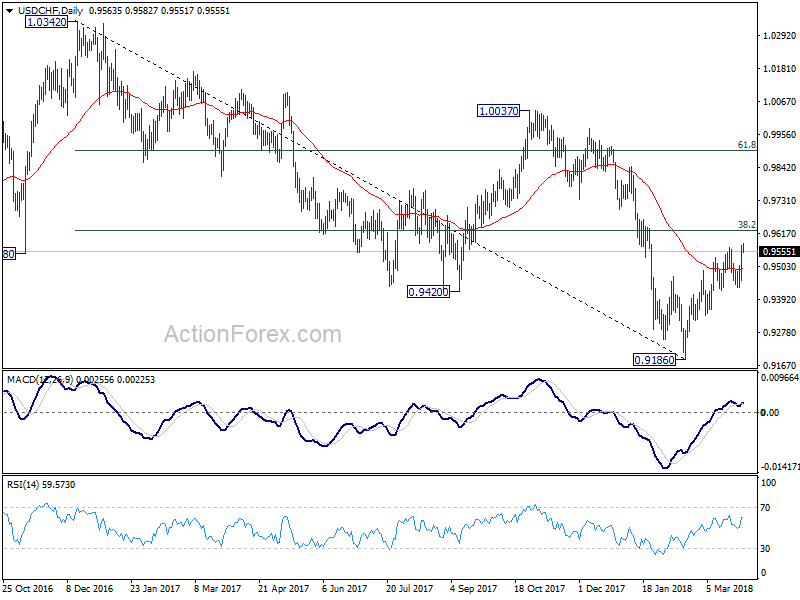

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9431; (P) 0.9470; (R1) 0.9505; More…

No change in USD/CHF’s outlook. Rebound from 0.9186 is still in progress but it’s seen as a corrective move. Hence, we’d expect strong resistance from 0.9626 key fibonacci level to limit upside. On the downside, break of 0.9432 support will indicate near term reversal and completion of rebound from 0.9186. In this case, intraday bias will be turned back to the downside for retesting 0.9186 low. However, sustained break of 0.9626 will be another evidence of larger reversal. In this case, further rise would be seen to next fibonacci level at 0.9900.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Main focus is on 38.2% retracement of 1.0342 (2016 high) to 0.9186 (2018 low) at 0.9626. Sustained break there will add to the case of trend reversal and target 61.8% retracement at 0.9900 and above). However, rejection from 0.9626 will maintain medium term bearishness for another low below 0.9186.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Building Permits M/M Feb | 5.70% | 0.20% | 0.00% | |

| 23:01 | GBP | GfK Consumer Confidence Mar | -7 | -10 | -10 | |

| 23:50 | JPY | Retail Trade Y/Y Feb | 1.60% | 1.70% | 1.60% | 1.50% |

| 07:00 | CHF | KOF Leading Indicator Mar | 106 | 107.2 | 108 | 108.4 |

| 07:55 | EUR | German Unemployment Mar | -19K | -15K | -22K | -23K |

| 07:55 | EUR | German Unemployment Claims Rate Mar | 5.30% | 5.30% | 5.40% | |

| 08:30 | GBP | Mortgage Approvals Feb | 64K | 66K | 67K | |

| 08:30 | GBP | Money Supply M4 M/M Feb | -0.40% | 1.30% | 1.50% | |

| 08:30 | GBP | Current Account Balance Q4 | -18.4B | -23.7B | -22.8B | |

| 08:30 | GBP | Index of Services 3M/3M Jan | 0.60% | 0.60% | 0.60% | |

| 08:30 | GBP | GDP Q/Q Q4 F | 0.40% | 0.40% | 0.40% | |

| 12:00 | EUR | German CPI M/M Mar P | 0.40% | 0.50% | 0.50% | |

| 12:00 | EUR | German CPI Y/Y Mar P | 1.60% | 1.70% | 1.40% | |

| 12:30 | CAD | GDP M/M Jan | -0.10% | 0.10% | 0.10% | 0.20% |

| 12:30 | CAD | Industrial Product Price M/M Feb | 0.10% | 0.40% | 0.30% | 0.40% |

| 12:30 | CAD | Raw Materials Price Index M/M Feb | -0.30% | 2.80% | 3.30% | 3.40% |

| 12:30 | USD | Personal Income Feb | 0.40% | 0.40% | 0.40% | |

| 12:30 | USD | Personal Spending Feb | 0.20% | 0.20% | 0.20% | |

| 12:30 | USD | PCE Deflator M/M Feb | 0.20% | 0.20% | 0.40% | |

| 12:30 | USD | PCE Deflator Y/Y Feb | 1.80% | 1.70% | 1.70% | |

| 12:30 | USD | PCE Core M/M Feb | 0.20% | 0.20% | 0.30% | |

| 12:30 | USD | PCE Core Y/Y Feb | 1.60% | 1.60% | 1.50% | |

| 12:30 | USD | Initial Jobless Claims (MAR 24) | 215K | 231K | 229K | 227K |

| 13:45 | USD | Chicago PMI Mar | 62 | 61.9 | ||

| 14:00 | USD | U. of Mich. Sentiment Mar F | 102 | 102 | ||

| 14:30 | USD | Natural Gas Storage | -86B |

{kind=link}