Euro rises broadly today as lifted by hawkish comments from an ECB official. Sterling closely follow as the second strongest one. On the other hand, New Zealand dollar continues to suffer broad based selling pressure today, in particular against Australian Dollar. Yen follows as the second weakest on optimism of easing trade tension between US and China. Dollar is trading as the third weakest as correction extends. The US economic calendar is empty today. And without any fresh inspirations, activity could drop a bit until tomorrow’s RBA minutes.

Technically, Dollar is staying in corrective mode against other major currencies. In particular, GBP/USD’s recovery has been very weak so far, limited below 1.3617 minor resistance, comparing to last week’s low at 1.3459. A key event that could trigger a range break out is tomorrow’s job and wage data. But some traders could jump the gun ahead of it. So 1.3459 and 1.3617 are two key levels to watch ahead. 86.05 in CAD/JPY is another level to watch today. CAD/JPY lags behind other yen crosses and is help in range of 85.37/86.05 today. But it’s near term bullish outlook is indeed more solid as the rise from March low of 80.52 has just resumed late last week. Break of 86.05 will extend this medium term rally.

ECB Villeroy de Galhau: Rate hike some “quarters” not “years” after ending QE

ECB Governing Council member, Bank of France Governor Francois Villeroy de Galhau said today that “the time when our net asset purchases will end is approaching”. Currently, ECB’s EUR 30B per month asset purchase program is set to end after September. Villeroy de Galhau said whether it will end in September, or December is not “a deep existential question”. Regarding interest rates, he added that “we could give additional guidance on its timing–well past meaning at least some quarters but not years–and its contingency on the inflation outlook.”

Trump offered concession ahead of US-China trade talks

China’s Vice Premier Liu He, President Xi Jinping’s top economic adviser is traveling to Washington to start the second round of trade talks tomorrow, with US Treasury Secretary Steven Mnuchin. Liu and his team will stay from May 15 to 19 according to a Foreign Ministry spokesperson.

Ahead of the meeting, Trump tweeted “President Xi of China, and I, are working together to give massive Chinese phone company, ZTE, a way to get back into business, fast. Too many jobs in China lost. Commerce Department has been instructed to get it done!” This is seen a concession by Trump ahead of the trade talks, which offers some hope of a positive outcome.

White House spokeswoman Lindsay Walters confirmed that US officials were in contact with Beijing about ZTE. And, Commerce Secretary Wilbur Ross is expected to “exercise his independent judgment, consistent with applicable laws and regulations, to resolve the regulatory action involving ZTE based on its facts.”

Cleveland Fed Mester: Fed fund rates could overshoot long run level

In a speech titled “Issues for U.S. Monetary Policy“, Cleveland Fed President Loretta Mester expressed her support for further rate hike. She noted that “the medium-run outlook supports the continued gradual removal of policy accommodation; it seems the best strategy for balancing the risks to both of our policy goals and avoiding a build-up of financial stability risks.

Regarding inflation, she noted that it will take a year or two to stabilize around the 2% target. And, she added that “we want to give inflation time to move back to goal … this argues against a steep path” on tightening. But, “as the expansion continues, it could be that in order to maintain our policy goals, we may need to move the fed funds rate, for a time, a bit above the level of the funds rate that is expected to prevail over the longer run”.

She also pointed to Fed’s March economic projections that fed funds rates could move a bit above the longer-run level at 3% by 2020. She noted that “2020 is a long time away and the policy path actually followed will be responsive to changes in the outlook.

OPEC raised both supply and demand forecasts, concerned with US trade relations

In May’s Monthly Oil Market Report, OPEC rated both 2018 oil supply and demand forecasts. For 2018, oil demand growth is forecast to increase by around 1.65mb/d to average 98.85 mb/d. Growth was revised higher from prior month by 25tb/d. China is anticipated to lead oil demand growth in 2018, followed by Other Asia and OECD Americas. Non-OPEC supply growth was revised up by 0.01mbs in 2018 to 1.75mb/d, averaging 59.62mb/d in total. Meanwhile, OPEC production rose 12tb/d to average 31.93mb/d in April.

In the section regarding world economy, OPEC warned of the risk of development in trade relations. In particular, it “the latest rounds of US sanctions on Russia, tariffs on Chinese products in combination with considerable requests by the US in trade negotiations with China, US tariffs on steel and aluminium, prolonged North American Free Trade Agreement (NAFTA) negotiations, as well as the US withdrawal from the Joint Comprehensive Plan of Action (JCPOA) with IR Iran all point to rising uncertainty.

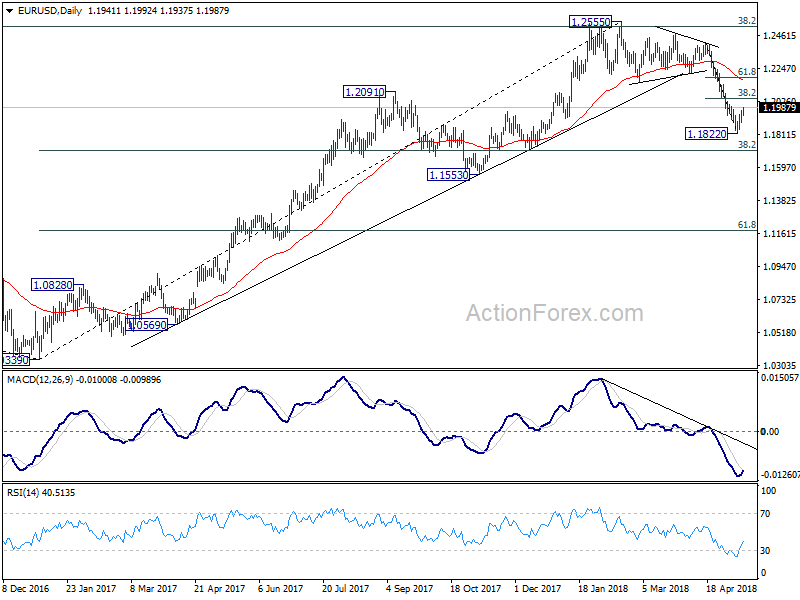

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1897; (P) 1.1932 (R1) 1.1974; More….

EUR/USD’s rebound from 1.1822 short term is still in progress and reaches as high as 1.1992 so far. Intraday bias remains on the upside for 38.2% retracement of 1.2413 to 1.1822 at 1.2048. We’d expect strong resistance from there to limit upside to bring fall resumption. On the downside, below 1.1932 minor support will turn bias to the downside for 1.1822 first. Break will resume the whole decline from 1.2555 and target 1.1708 medium term fibonacci level next.

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term was formed at 1.2555 already. Decline from there should extend further. Break of 38.2% retracement of 1.0339 to 1.2555 at 1.1708 will target 61.8% retracement at 1.1186. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2179) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Domestic CGPI Y/Y Apr | 2.00% | 2.00% | 2.10% | |

| 6:00 | JPY | Machine Tool Orders Y/Y Apr P | 22.00% | 28.10% |

{kind=link}