Euro rebounds strongly and broadly today as the markets cheer political turmoils in Italy. On the other hand, Swiss Franc and Japanese Yen are trading as the weakest as sentiments improved. There appears to be some breakthrough again between US and North Korea as South Korean President Moon Jae-in successfully pulled the two parties back to the table. The economic calendar is light today with UK and US on holiday. So trading could be relatively subdued. Nonetheless, a large batch of heavy weight economic data are lining up ahead to make it a jam packed week.

Technically, while EUR/USD rebounds, it’s held below 1.1750 minor resistance so far. There is no indication of bottoming yet. This 1.1750 resistance will be watched ahead. USD/JPY despite last week’s sharp pull back, was held above 108.82 near term support. Rebound above this level will help re-confirm near term bullishness. Meanwhile, USD/CAD, despite last week’s rebound, is held below 1.2996 resistance. This have to be taken out firmly to confirm rally resumption.

Euro rebounds as formation of eurosceptic Italy government collapsed

Italy is in fresh political turmoil again as the formation of the new eurosceptic government collapsed. Nonetheless, the Euro is lifted mildly higher today as that’s seen as a positive development for the common currency.

President Sergio Mattarella vetoed Paolo Savona as the as economy minister. Savona is an 81-year-old eurosceptic economist who’s a vocal critic of the common currency. Mattarella said in a televised speech that “the uncertainty over our position (on euro) has alarmed investors and savers both in Italy and abroad.” And, he emphasized that “membership of the euro is a fundamental choice. If we want to discuss it, then we should do so in a serious fashion.” Mattarella added that “I asked for that ministry an authoritative political figure from the coalition parties who was not seen as the supporter of a line that could provoke Italy’s exit from the euro.”

Prime Minister-designate Giuseppe Conte promptly abandoned the effort to form a new government. The far-right League and anti-establishment Five Star Movement, accused Mattarella of abusing his authority and working under the orders of European powers. Five Star leader Luigi D Maio even demanded that parliament impeach Mattarella. League chief Matteo Salvini threatened mass protests unless snap elections were called.

Former IMF director of fiscal affairs Carlo Cottarelli was called in to head a stopgap government. But he’s unlikely to have enough support from the parliament. So, that’s only a short-term solution and an election is now likely to be held to solve the political crisis, possibly in September or October.

Abe to tell Trump Japanese carmakers made huge contributions to the US economy

Japan Prime Minister Shinzo Abe was asked in the parliament today about Trump intention to impose tariffs on car imports using national security as excuse. Abe said he would seek to convince Trump that Japan carmakers are important in boosting the US economy.

He noted that Japan auto makers have “created jobs and made huge contributions to the U.S. economy.” And he added that the number of cars Japanese automakers produce in the US is double the number it exports to the country.

And he emphasized that “as a country that prioritizes a rule-based, multilateral trade system, Japan believes that any steps taken on trade must be in line with World Trade Organization rules.”

Separately, he added that “Japan has explained to the United States its stance that TPP is the best format for both countries. We will continue to talk with the United States based on this view.”

South Korea Moon revived the Kim-Trump summit. He could join to make it three-way

South Korean president Moon Jae-in had a surprised meeting with North Korean leader Kim Jong-un on Saturday, regarding the summit with the US. Moon’s office said after the meeting that the leaders “exchanged views and discussed ways to implement the Panmunjom Declaration and to ensure a successful US-North Korea summit.”

Moon added in a press conference that “should the North Korea-US summit succeed, I would like to see efforts to formally end the (Korean) war through a three-way summit of the South, the North and the US.” Moon added in a press conference that “should the North Korea-US summit succeed, I would like to see efforts to formally end the (Korean) war through a three-way summit of the South, the North and the US.” Moon also sought agreement from Kim that the summit must be held.

A South Korean official said that “the discussions are just getting started, so we are still waiting to see how they come out, but depending on their outcome, the president could join President Trump and Chairman Kim in Singapore.”

White House spokeswoman Sarah Sanders also said that “the White House pre-advance team for Singapore will leave as scheduled in order to prepare should the summit take place.” Also, Trump himself tweeted that the US teams is now in North Korea to discuss the meeting.

BoC to stand pat, economic data to drive the week

Looking ahead, the calendar is very light today with no notable release. UK and US are on bank holiday so volatility could be subdued. But a jam packed week will start on Tuesday. BoC rate decision is a highlight but based on current uncertainties around trade, there is little chance for the central bank to act.

Economic data, on the other hand, will come back to spotlights. US will release consumer confidence, personal income and spending as well as PCE inflation, ISM manufacturing and non-farm payroll. We’ll have a rather comprehensive look at the US economy on inflation, wage growth, manufacturing and job market.

May CPI will be the major focus in Eurozone. It’s expected to bounce back from 1.2% to 1.6% yoy. Core CPI is also expected to rebound from 0.7% yoy to 1.0% yoy. Such development would give ECB policymakers more confidence to end the asset purchase program this year. But another miss will give them a lot of headaches.

For BoE, the chance of a rate hike in August got slimmer after last week’s CPI miss. But a November hike is still on the table.

UK PMI manufacturing will show some lights on how the economy is bouncing back on Q2.

Here are some highlights for the week ahead:

- Tuesday: Swiss trade balance; Eurozone M3; UK S&P Case Shiller house price, consumer confidence

- Wednesday; New Zealand building permits, RBNZ financial stability report; Australia building approvals; Japan retail sales, consumer confidence; Germany retail sales, import prices, CPI, unemployment; French GDP; Swiss KoF; US ADP employment, GDP revision, trade balance, wholesale inventories, Fed’s Beige Book; BoC rate decision, Canada current account, IPPI and RMPI

- Thursday: Japan industrial production, housing starts; China official PMIs, New Zealand ANZ business confidence; Australia private capital expenditure; Swiss retail sales; UK M4, mortgage approvals; Eurozone CPI flash, unemployment; Canada GDP; US personal income and spending, pending home sales, jobless claims

- Friday: New Zealand terms of trade; Japan capital spending; China Caixin PMI manufacturing; Swiss PMI manufacturing; Eurozone PMI manufacturing final; UK PMI manufacturing; US non-farm payroll, ISM manufacturing, construction spending; Canada PMI manufacturing

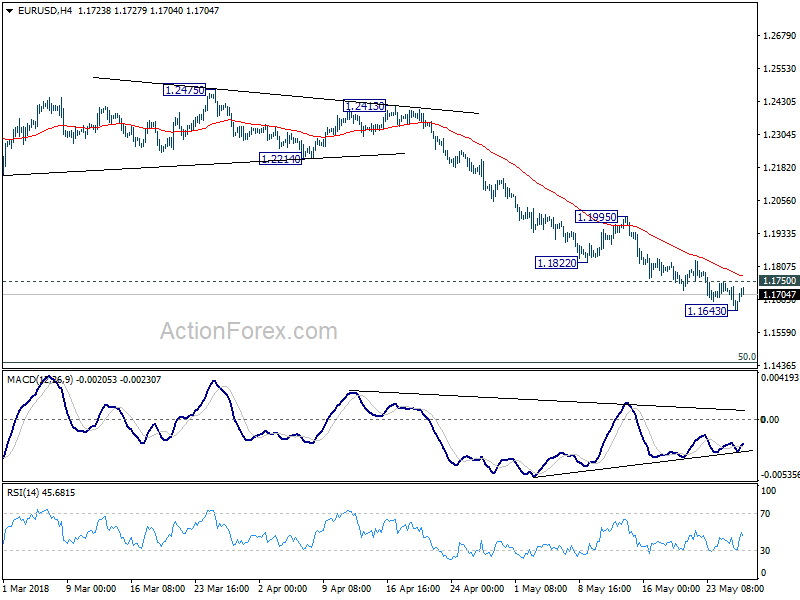

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1618; (P) 1.1676 (R1) 1.1707; More…..

EUR/USD’s recovery today pulled 4 hour MACD above signal line again. A temporary low is in place and intraday bias is turned neutral for consolidations. Even in case of rebound, firm break of 1.1995 resistance is needed to confirm reversal. Otherwise, outlook will remain bearish for deeper decline. Below 1.1643 will resume the fall from 1.2555 and target 50% retracement of 1.0339 to 1.2555 at 1.1447 next.

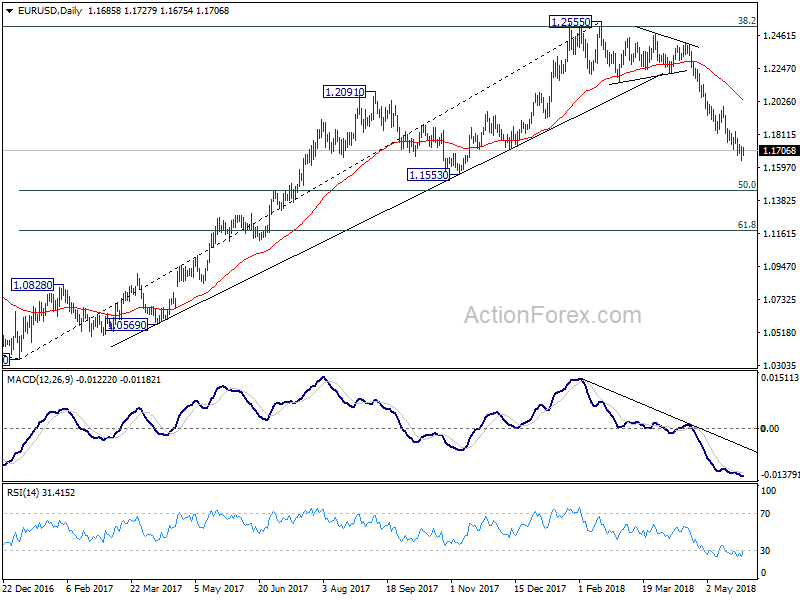

In the bigger picture, current development suggests that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. And, a medium term top was formed at 1.2555 already. Decline from there should extend further to 61.8% retracement of 1.0339 to 1.2555 at 1.1186 and below. For now, even in case of rebound, we won’t consider the fall from 1.2555 as finished as long as 55 day EMA (now at 1.2049) holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Y/Y Apr | 0.90% | 0.50% | 0.50% | |

| 8:00 | CHF | Total Sight Deposits CHF (25 MAY) | 576.4b |

{kind=link}