{kind=link}

Dollar trades broadly softer in Asian session today as yesterday’s rebound attempt lost steam. Traders are also turning more cautious ahead of FOMC rate decision. While Fed is widely expected to hike, the main question remains on whether there will be three or four hikes this year. Also, Jerome Powell will also make his debut and hold the first post meeting press conference as Fed chair. Elsewhere in the forex markets, while Sterling dipped yesterday following lower than expected CPI, lost was limited. The Pound will look into today’s employment data, and then tomorrow’s BoE rate decision. Canadian Dollar is notable higher as lifted by news on positive development in NAFTA talks.

In other markets, DOW closed higher by 0.47% overnight while S&P 500 gained 0.15%. NASDAQ also gained 0.27% but stayed below Monday’s gap. 10 year yield closed up 0.034 at 2.879 as recent range trading continued between 2.8 and 2.95. Nikkei is trading down -0.47% at the time of writing while HK HSI is up 1.2%.

Fed to hike in Powell’s debut

Fed is widely expected to raise federal funds rate by 25bps to 1.50-1.75% today. Fed fund futures are pricing in near 95% chance of that. There is no reason for Fed to give market a surprise. The main question in everybody’s mind is whether Fed will hike a total of three times this year, or four. Fed fund futures are pricing more than 80% chance of another hike in June already, and close to 60% chance of another in September. But for now, it’s only pricing less than 40% chance of the fourth in December.

As usual with a March FOMC meeting, new economic projections will be released. Given that the Republican’s tax cuts were done, there could be upward revisions in growth. Unemployment rate forecast might be left unchanged. PCE core at 1.5% in January, is still way off Fed’s median projection of 1.9% in 2018. There is little chance of a change in that figure. Meanwhile, any slight change in the federal funds rate projection would be market moving.

Fed’s December projections:

The event also bears additional significance as it’s Powell’s first press conference as Fed chair. His Congressional testimony was seen by some as more hawkish and upbeat than expected. Recapping that he said “my personal outlook for the economy has strengthened since December.” And, “we’ve seen some data that will in my case add some confidence to my view that inflation is moving up to target.” Powell might maintain the tone today and indicate his confidence in continuing the tightening cycle.

The event also bears additional significance as it’s Powell’s first press conference as Fed chair. His Congressional testimony was seen by some as more hawkish and upbeat than expected. Recapping that he said “my personal outlook for the economy has strengthened since December.” And, “we’ve seen some data that will in my case add some confidence to my view that inflation is moving up to target.” Powell might maintain the tone today and indicate his confidence in continuing the tightening cycle.

G20 stressed importance of trade, urged further dialogue, nothing more

G20 finance ministers and central bank governors ended the summit in Buenos Aires with a joint communique that emphasized the importance of international trade. And they urged for the need for “further dialogue and actions”. But the communique fell short of anything else to push back protectionism.

The communique noted “International trade and investment are important engines of growth, productivity, innovation, job creation and development.” And, “we reaffirm the conclusions of our Leaders on trade at the Hamburg Summit and recognise the need for further dialogue and actions.” They pledged to work to “strengthen the contribution of trade to our economies.”

Below is the full communique covering areas like technology, infrastructure, global financial system, cross-border capital flow, debts, international tax system and even Cryto-assets. But trade wasn’t mentioned beyond the first paragraph.

Trump to announce tariffs on Chinese goods on Thursday, but will seek industry input before finalizing

US President Donald Trump is set to announce the package of tariffs against Chinese goods on Thursday, a day earlier than rumored. It’s believed that the total amount of targeted goods adds up to USD 30-60b. We believe that it will be on the higher side on the range. Additionally, there will be new restrictions on Chinese investments in the US. Treasury will be directed to outline the rules regarding Chinese investments.

But, it’s reported that the tariffs won’t take effect immediately. Instead, businesses are given a chance to comment on the list of tariffed products. The final decision will come after industry input. This is seen as an act of Trump bowing down to pressure from business leaders. Earlier this week, 45 of largest American trade groups wrote an open letter to Trump, warning Trump not to respond to unfair Chinese practices and policies by measures that will “harm U.S. companies, workers, farmers, ranchers, consumers, and investors.”

GBP finds footing as UK employment data eyed

For now, Sterling is still trading as the second strongest major currency for the week despite yesterday’s post CPI dip. Employment data will be a main focus today. Markets expect claimant counts to dropped -3.1k in February. ILO unemployment rate is expected to stay unchanged at 4.4% in January. A key focus is on wage growth as average weekly earnings is expected to rise 2.6% 3moy in January. Still, with CPI at 2.7% yoy, wage is still playing catch up.

Reaction to the job data could be muted though as the major focus is on tomorrow’s BoE rate decision. BoE is widely expected to keep bank rate unchanged at 0.50% and asset purchase target at GBP 435b. No updated economic projections will be delivered as they were published back in February’s Inflation Report already. Instead, eyes will be on whether BoE would turn more upbeat in the statement, given that a Brexit transition deal is already done. In addition, known hawks Michael Saunders and Ian McCafferty could come back with a vote on rate hike. All in all, focus in on gauging the chance of a May hike.

Public sector net borrowing will also be released from the UK.

CAD rebounds as US dropped one of the toughest protectionist demand in NAFTA talks

Canadian Dollar rebounds strongly on news that US will drop contentious auto-content proposal in NAFTA talks. It’s seen as clearing and important road block in NAFTA renegotiation. The Loonie is trading as the strongest major currency in Asian session. There was a demand for vehicles made in Canada and Mexico for export to the US contain at least 50% US content. But Canada’s Globe and Mail reported that this contentious demand was dropped during NAFTA meeting in Washington last week. This is seen by some as one of the US toughest protectionist demand.

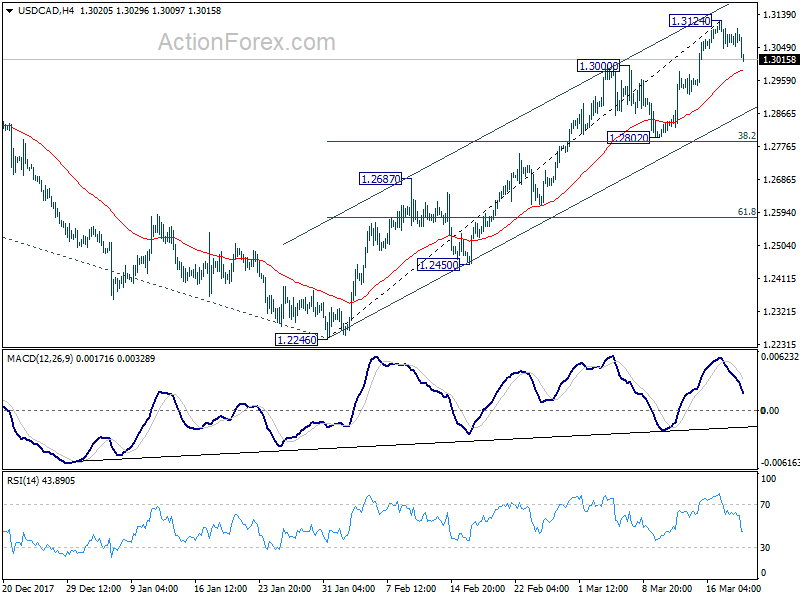

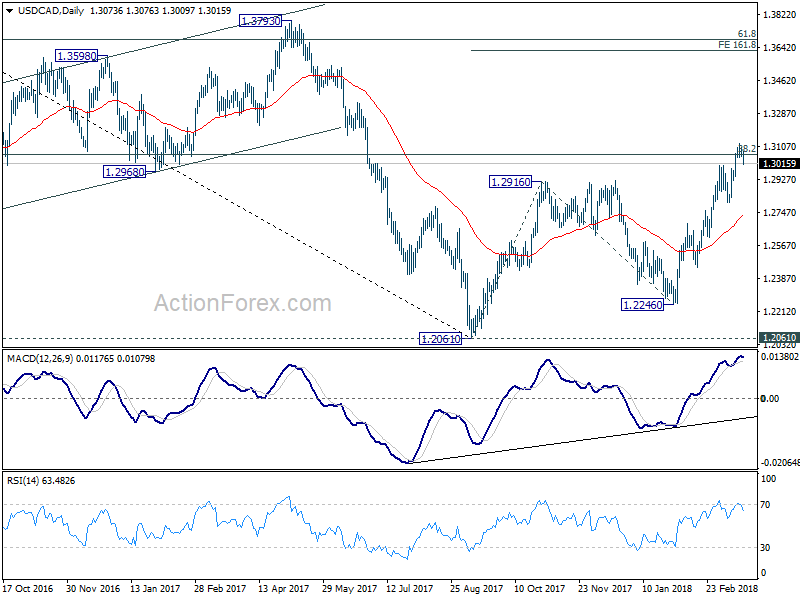

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3047; (P) 1.3075; (R1) 1.3098; More….

USD/CAD’s retreat from 1.31214 extends lower today and reaches 1.3009 so far. Deeper fall could be seen to 4 hour 55 EMA (now at 1.2986). But strong support should be seen above 1.2802 cluster (38.2% retracement of 1.2246 to 1.3124 at 1.2789) to contain downside and bring rally resumption. On the upside, break of 1.3124 will extend recent rally to 161.8% projection of 1.2061 to 1.2916 from 1.2246 at 1.3629 next.

In the bigger picture, we’re favoring the medium term bullish case. That is larger down trend from 1.4689 has completed at 1.2061 as a correction, drawing support from 50% retracement of 0.9406 (2011 low) to 1.4689 (2015 high) at 1.2048. Sustained break of 38.2% retracement of 1.4689 to 1.2061 at 1.3065 will pave the way to 61.8% retracement at 1.3685. This will be the preferred case now as long as 1.2802 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | AUD | Westpac Leading Index M/M Feb | 0.30% | -0.24% | -0.30% | |

| 09:30 | GBP | Jobless Claims Change Feb | -3.1K | -7.2K | ||

| 09:30 | GBP | Claimant Count Rate Feb | 2.30% | |||

| 09:30 | GBP | Average Weekly Earnings 3M/Y Jan | 2.60% | 2.50% | ||

| 09:30 | GBP | ILO Unemployment Rate 3Mths Jan | 4.40% | 4.40% | ||

| 09:30 | GBP | Public Sector Net Borrowing Feb | -0.4B | -101B | ||

| 14:00 | USD | Existing Home Sales Feb | 5.41M | 5.38M | ||

| 14:30 | USD | Crude Oil Inventories | 5.0M | |||

| 18:00 | USD | FOMC Rate Decision | 1.75% | 1.50% | ||

| 18:30 | USD | FOMC Press Conference | ||||

| 20:00 | NZD | RBNZ Rate Decision | 1.75% | 1.75% |