{kind=link}

Mid-Day Report: Dollar Unmoved after ADP Grew 190k, Sterling and Aussie Staying Weak

Quick update: CAD is sold off after BoC said in the statement that Governing "Council will continue to be cautious, guided by incoming data in assessing the economy’s sensitivity to interest rates, the evolution of economic capacity, and the dynamics of both wage growth and inflation." The language suggests BoC will stay in wait-and-see mode in near term, practically rule out a hike in January.

Dollar continues to trade with a mixed today as economic data released from US provide little inspiration. Sterling weakness remains the main theme in rather directionless markets. Misalignment within UK politicians remain the key issue in Brexit negotiation and Prime Minister Theresa is still struggling to put things back under control. Meanwhile, Australian Dollar stays as the second weakest one after today’s GDP mixed. On other hand, Yen is extending its rebound, in particular against Europeans. Canada Dollar follow closely as markets await BoC rate decision. The Loonie would be given a boost if BoC signals that it’s back in tightening path again.

Release from US, ADP report showed 190k growth in private sector jobs in November, just 1k below expectation of 191k. Non-farm productivity was finalized at 3.0% in Q3, unit labor costs at -0.2%. From Canada, labor productivity dropped -0.6^ qoq in Q3. Release earlier today, Eurozone retail PMI rose to 52.4 in November. German factory orders rose 0.5% mom in October. Swiss CPI was rose to 0.8% yoy in November.

UK PM May insist on making very good progress after talking to DUP leader

In UK, Prime Minister Theresa May finally had a phone call with North Ireland DUP leader Arlene Foster today. Foster, who interrupted May’s talk with European Commission President Jean Claude Juncker, initially refused to answer the call. May said afterwards that "very good progress" was made in Brexit negotiation, but a DUP spokesman sounded indifferent and said that there was "more work to be done". May is expected to go back to Brussels to resume the negotiation with EU and targets to complete "sufficient" progress by Sunday at most. But so far, the issue of Irish border remain a key showstopper and there isn’t any positive development seen yet.

ECB Mersch urged to plan for QE exit

ECB Executive Board member Yves Mersch urged the central bank to start planning for ending the asset purchase program. He said that "while a too quick end to the buying program could lead to excessive market reactions, we should not forget that the longer the programme lasts, … the greater the risks will become." And, "a credible perspective for an exit from QE is therefore key in curbing risks."

Greek 10 year yield dropped to 8 year low

Greece 10 year government bond year drops to as low as 4.802% today, hitting the lowest level in eight years since November 2009. This is partly a reflection on the preliminary agreement with Eurozone regarding the reforms of the bailout program. That kept Greece on course for ending financial aids next year in August. Also, it reflects general optimism within Eurozone as investors are back taking more risks and yields. It’s also seen as a factor keeping the Swiss Franc soft.

Australia GDP showed weak spending growth

Australian Dollar tumbles broadly today as weighed down by disappointing GDP data. Q3 GDP rose 0.6% qoq 2.8%, below expectation of 0.7% qoq, 3.0% yoy. Despite the miss, the headline numbers are not bad at all. Treasurer Scott Morrison described the figures as indicating "solid" economic growth. And he said that "this is above the OECD average and puts Australia back up towards the top of the pack for major advanced economies around the world." However, weak household consumption is seen as the most worrying part of the details. Consumer spending grew just 0.1% qoq and was at the lowest rate in more than a decade since 2005. Sluggish wage growth, as pointed out by RBA rate statement released yesterday, was a key factor and would likely continue to be.

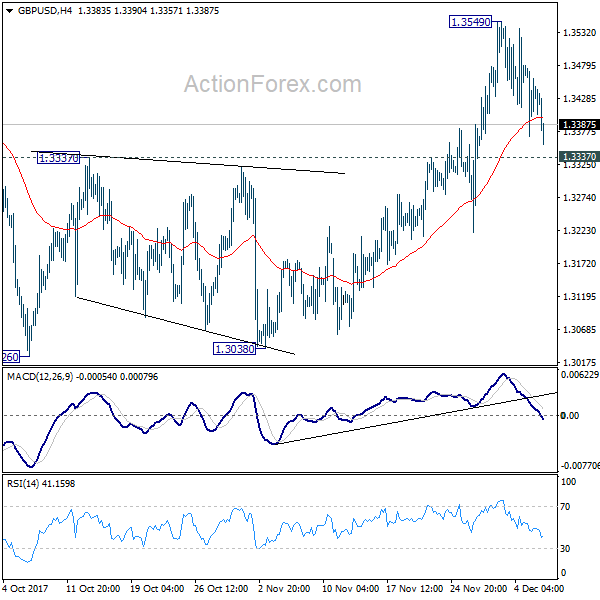

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3381; (P) 1.3429; (R1) 1.3489; More….

GBP/USD’s pull back from 1.3549 extends to as low as 1.3357 so far today. But the pair is still staging above 1.3337 resistance turned support. Intraday bias remains neutral and another rise is still expected. Break of 1.3549 will target 1.3651 high and above. However, decisive break of 1.3337 will argue that rise from 1.3038 has completed and turn bias back to the downside for this support.

In the bigger picture, while the medium term rebound from 1.1946 low is strong, it’s still limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we’d view such rebound as a correction. That is, we’d expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | GDP Q/Q Q3 | 0.60% | 0.70% | 0.80% | 0.90% |

| 07:00 | EUR | German Factory Orders M/M Oct | 0.50% | -0.20% | 1.00% | 1.20% |

| 08:15 | CHF | CPI M/M Nov | -0.10% | 0.00% | 0.10% | |

| 08:15 | CHF | CPI Y/Y Nov | 0.80% | 0.80% | 0.70% | |

| 09:10 | EUR | Eurozone Retail PMI Nov | 52.4 | 51.1 | ||

| 13:15 | USD | ADP Employment Change Nov | 190K | 191K | 235K | |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -0.60% | -0.40% | -0.10% | -0.20% |

| 13:30 | USD | Nonfarm Productivity Q3 F | 3.00% | 3.30% | 3.00% | |

| 13:30 | USD | Unit Labor Costs Q3 F | -0.20% | 0.30% | 0.50% | |

| 15:00 | CAD | BoC Rate Decision | 1.00% | 1.00% | 1.00% | |

| 15:30 | USD | Crude Oil Inventories | -5.6M | -3.2M | -3.4M |