The completion of US-China trade deal phase one was well received by investors. There was an additional bonus of scrapping the label of China as currency manipulator by the US Treasury. The is no time frame for the phase two negotiations yet. But the US is already working with EU and Japan to push WTO changes regarding subsidies and forced technology transfers. The USMCA passed the Senate, and is now waiting for Canada’s ratification. Situation regarding trade tensions seems to be moving in the right direction.

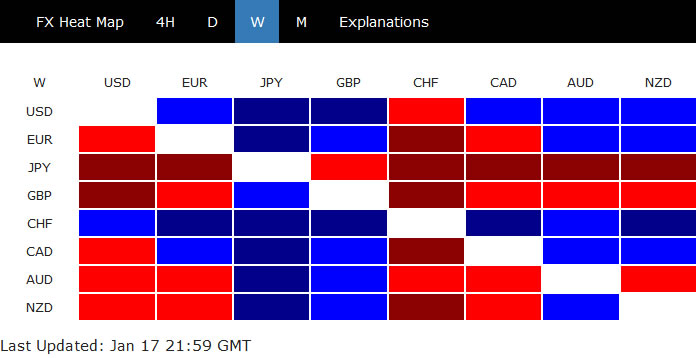

In the currency markets, Swiss Franc ended as the strongest one, as US put Switzerland back in currency manipulator monitoring list. Political uncertainty in Russia also triggered some safe haven flow. The greenback followed as the second strongest. Late rally in Dollar index adds to the case of near term bullish reversal. Yen was the weakest one on risk appetite in stocks markets. Sterling was second weakest on increasing bet on BoE rate cuts.

S&P 500 in upside acceleration, targeting 3500 handle

US stocks responded positively to the developments last week, with all major indices closing at new record highs. The development in S&P 500 confirmed strong break of long term channel resistance. That’s a solid sign of upside acceleration in medium term long term. Current up trend should target 100% projection of 1810.10 to 2940.91 from 2346.58 at 3477.39 next. 3500 psychological might be the level for topping, but let’s see. For now, near term outlook will stay bullish as long as 3214.63 support holds, in case of retreat.

Dollar index’s correction could have completed

Dollar index’s rebound from 96.35 resumed last week and closed at 97.60, above 55 day EMA. The development is favoring the case that corrective fall from 99.66 has completed with waves down to 96.35. Focus will now be on 97.81 resistance this week. Break there will affirm this bullish case and target 98.54 resistance for confirmation. However, break of 97.08 will likely extend the correction from 99.66 through 96.35, possibly to 38.2% retracement of 88.26 to 99.66 at 95.30, before completion.

Swiss Franc surged on US and Russia

Swiss Franc ended as the strongest one last week on two developments. Firstly, US Treasury put Switzerland back into the monitoring list for currency manipulation. That might limit SNB’s currency intervention to curb the Franc’s strength. Secondly, we believe there was some safe haven flows into Swissy, and to a lesser extent Euro, on political uncertainty in Russia.

Former Prime Minister Dmitry Medvedev resigned after President Vladimir Putin laid how his reform plan to shift powers to the parliament. Little-known tax chief, Mikhail Mishustin was quickly reappointed as the Prime Minister. Putin’s plan after ending his term in 2024 is uncertain. Some see him as preparing to stay in power as Prime Minister. But some see his move as limiting power of Medvedev if he becomes then next President.

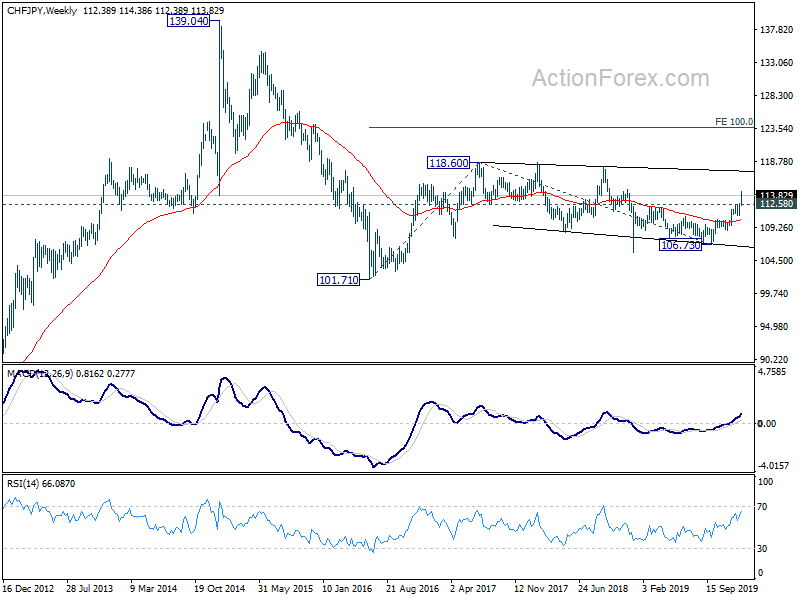

CHF/JPY was surprisingly the top move last week, up 1.13%. Technically, the rise from 106.73 is clearly in acceleration, as seen in weekly MACD. Further rally is expected as long as 112.58 support holds, towards 118.60 key resistance. At this point, it’s uncertain whether the rise from 101.71 is ready to resume. Or, CHF/JPY is still engaging in medium term range trading. Reactions from 118.60 will unveil the picture. Firm break there will pave the way to 100% projection of 101.71 to 118.60 from 106.73 at 123.62.

Sterling sold off as on BoE rate cut bets

Sterling was the second weakest last week as bets on BoE rate cut surged. Comments from outgoing BoE Governor Mark Carney as well as other policy makers hinted that policy easing is in the MPC’s mind already. Economic data were also poor. UK GDP surprisingly contracted -0.3% mom in November. CPI closed to 1.3% yoy in December, hitting the lowest level since December 2016. Retail sales also contracted by -0.8% in December.

At this point, opinions are divided on whether BoE would cut interest rate at the January 30 meeting. The decision could very much depend on incoming data, including employment and PMIs to be featured this week. It would also take some more time for BoE to prepare the updated economic projections to be released at the meeting. Before that, the Pound would at least struggle to extend post-election rally.

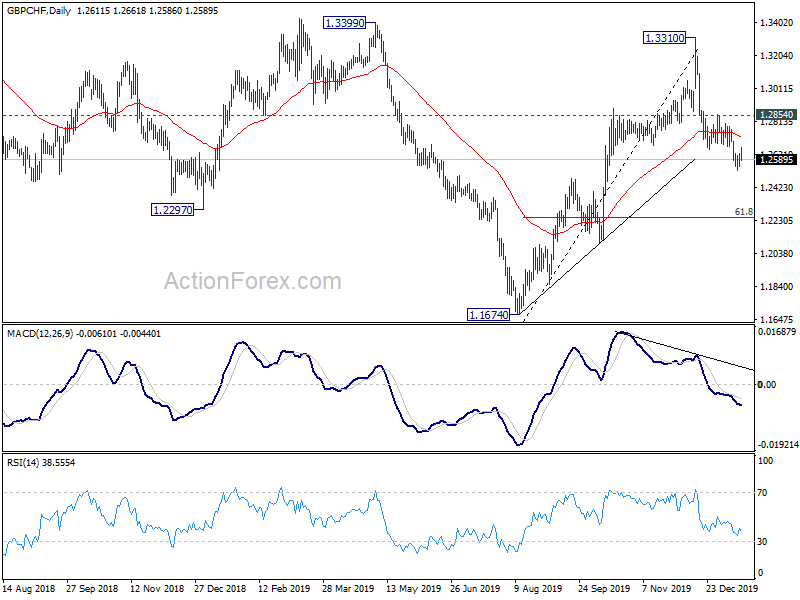

GBP/CHF was the second biggest mover last week, losing -0.94%. Fall from 1.3310 is currently seen as a correction to whole rise from 1.1674. Deeper decline is expected as long as 1.2854 resistance holds, towards 61.8% retracement of 1.1674 to 1.3310 at 1.2299. GBP/CHF might bottom there and rebound.

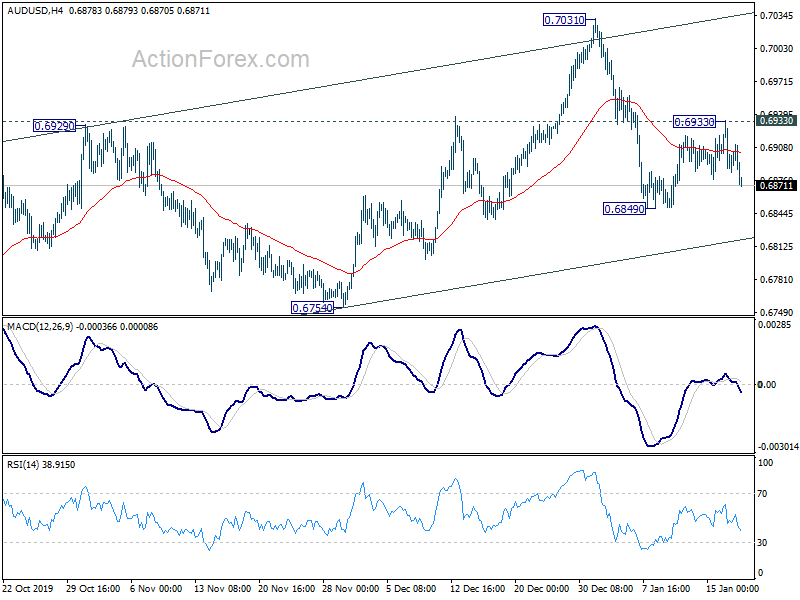

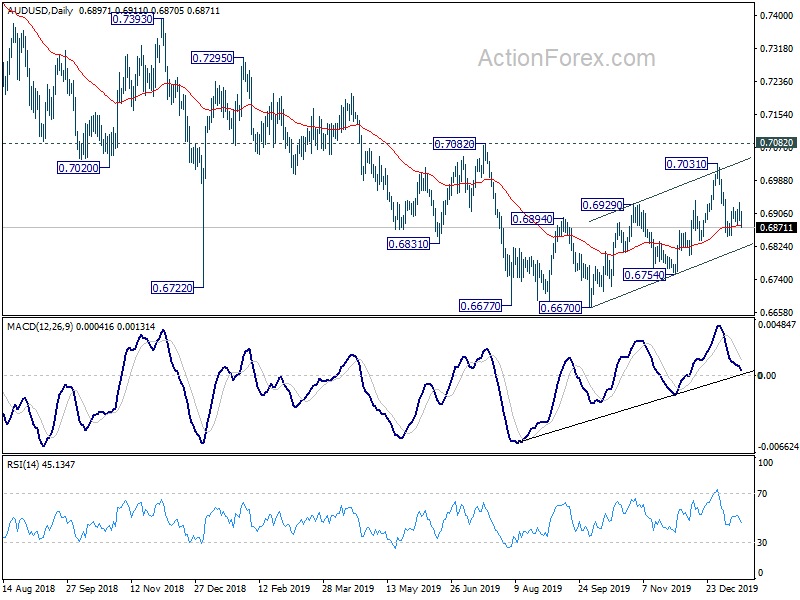

AUD/USD Weekly Outlook

AUD/USD recovered to 0.6933 last week but quickly reversed. As it’s staying in consolidation above 0.6849, initial bias remains neutral this week first. Outlook is unchanged that rebound from 0.6670 could have completed with three waves up to 0.7031. Break of 0.6849 will turn bias to the downside for 0.6754 support. Decisive break there will confirm this bearish case. On the upside, however, break of 0.6933 will turn focus back to 0.7031 resistance instead.

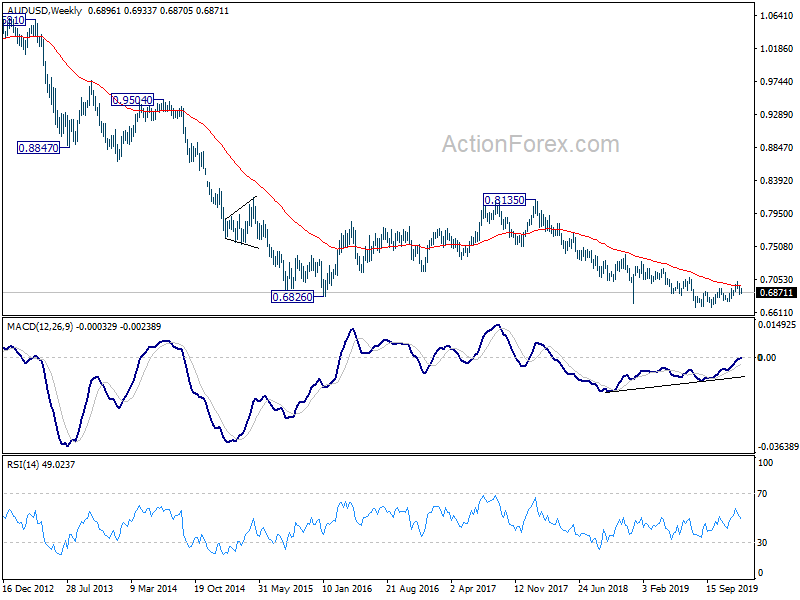

In the bigger picture, with 0.7082 resistance intact, there is no clear confirmation of trend reversal yet. That is, down trend from 0.8135 (2018 high) is still expect to continue to 0.6008 (2008 low). However, decisive break of 0.7082 will confirm medium term bottoming and bring stronger rally back to 55 month EMA (now at 0.7484).

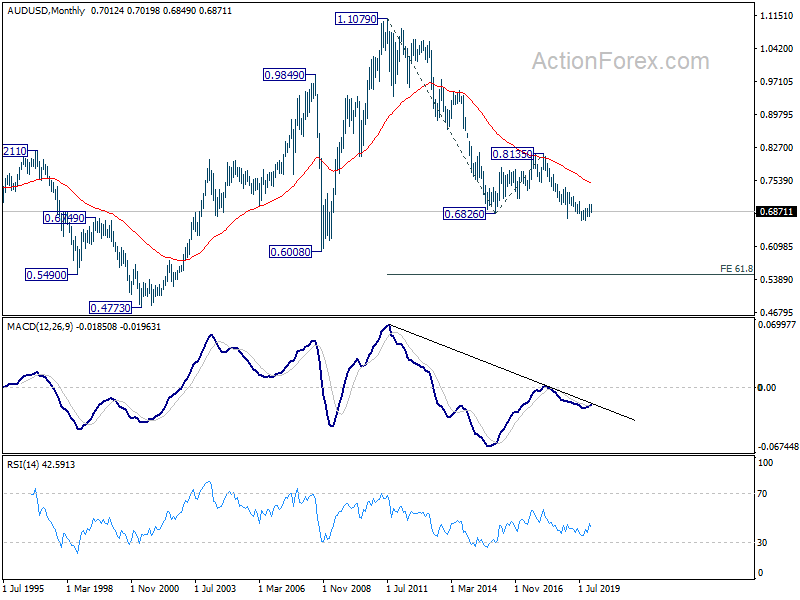

In the longer term picture, prior rejection by 55 month EMA maintained long term bearishness in AUD/USD. That is, down trend from 1.1079 (2011 high) is still in progress. Next downside target is 61.8% projection of 1.1079 to 0.6826 from 0.8135 at 0.5507.

{kind=link}