A cloud of recession fears dominated a week full of significant events, with disappointing PMI data, particularly from Eurozone and US, dampening sentiment towards the end. Investors also grappled with mismatched expectations concerning Chinese fiscal stimulus, which added additional pressure on global stock indexes, driving them lower by the end of the week. Nevertheless, the retreat in US market was relatively mild in comparison.

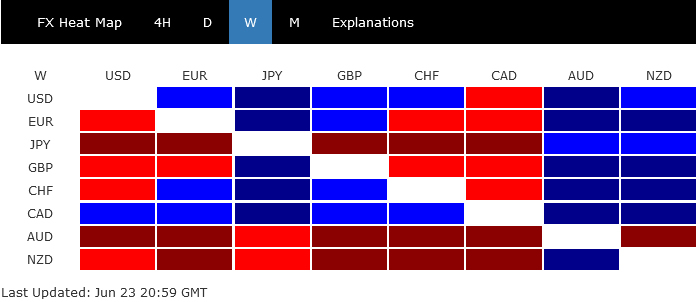

In the Forex market, Australian and New Zealand Dollars faced a rough week, ending as the worst performers. While Japanese Yen continued its near-term downtrend, triggering verbal interventions from the Japanese government, it stood as only the third weakest. Canadian Dollar emerged as the top performer, backed by strong retail sales data. Dollar clinched the second spot, followed by Swiss Franc – a clear reflection of the overall risk sentiment. Meanwhile, Euro and Sterling showed mixed results for the week.

Dollar Index finds respite amid risk-off sentiment

Boosted by an increasing risk-off sentiment, particularly following a series of weak PMI data released last Friday from various countries, Dollar Index closed on a high note. Despite this uptick, the prevailing analysis remains unchanged; price action from 100.82 appears to be a consolidation pattern, which may have completed with three waves to 104.69.

Short-term bearish outlook was neutralized somewhat by breach of 55 D EMA, now at 102.96. Yet, any failure to sustain above the EMA, followed by a dip below last week’s low of 101.92, could trigger resurgence of bearish sentiment and bring deeper decline to retest 100.82 low. On the flip side, sustained trading above the EMA might fuel a more robust rise to 104.69 and potentially higher, elongating the consolidation from 100.82.

For the near term, the developments in risk markets could be a key factor shaping the trajectory of the greenback, at least until release of PCE inflation data this coming Friday. Last week’s dip in S&P 500, was relatively shallow, and didn’t threaten the rise from 3808.86. Still, extended correction could provide some support for Dollar.

As it stands, near-term outlook for S&P 500 remains bullish as long as 4261.07 support level holds. A break above 4448.47 would reignite the broader rally from 3491.58 towards 161.8% projection of 3491.58 to 4100.51 from 3808.86 at 4794.11, which is just shy of the record high at 4818.62.

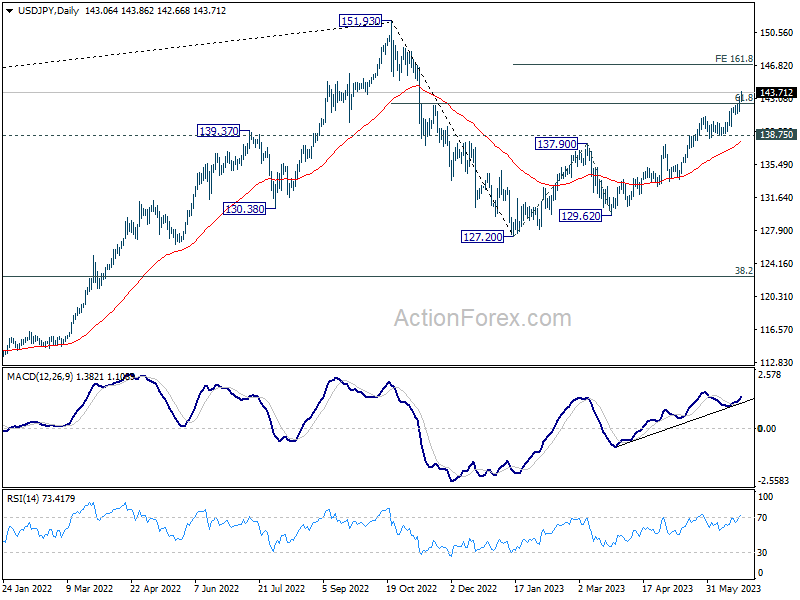

US 10-year yield trades sideways while USD/JPY rallies: awaiting potential catalysts

US 10-year yield continued to trade in sideway trading below 3.859 resistance last week. Breach of 55 D EMA (now at 3.653) cannot be ruled out consolidation extends. But further rally will remain in favor as long as 3.570 support holds. Corrective fall from 4.333 could have completed with three waves down to 3.253 already. Above 3.859 will target 4.091 resistance next. Firm break there should confirm this case and bring retest of 4.333 high.

USD/JPY’s rally from 127.20 extended to as high as 142.66 last week. From a pure technical point of view, the strong break of 61.8% retracement of 151.93 to 127.20 at 142.48 could now set the stage for retesting 151.93 high. In particular, USD/JPY could accelerate from here if 10-year yield manages to break through 3.859 resistance to resume recent rally. And in case of retreat, near term bullish should be retained as long as 138.75 support holds. But then of course, there is risk of intervention by Japan.

Aussie down with Hong Kong HSI and Copper

Australian Dollar ended the week as the worst performer, reversing nearly half of the gains made this earlier this month, on a couple of developments. RBA minutes indicated that a hold was indeed considered at last meeting, and the arguments were finely balanced. That raised some doubts regarding the chance of another rate hike in July, and made the coming monthly CPI reading crucial.

Then Aussie was dragged down by selloff in Yuan and stocks in China and Hong Kong. The impact of PBoC’s rate cut has been very brief and mild. The rumors regarding massive stimulus from the Chinese government didn’t really realize.

Hong Kong HSI’s steep decline last week suggests that rebound from 18044.85 has completed at 20155.92, after rejection by medium term channel resistance. More importantly, the down trend from 22700.85 is probably still in progress, and it’s now in favor to continue through 18044.85 to 61.8% retracement of 14597.31 to 22700.85 at 17692.86 before completion.

In corresponding development, Copper also tumbled notably on worries regarding China’s economic recovery. While rebound from 3.5393 was stronger than expected, it appeared to have faced strong resistance from 50% retracement of 4.3556 to 3.5393. Immediate focus is back on 3.7341 support in the coming days. Break there will argue that whole down trend from 4.3556 is ready to resume through 3.5393 low.

Extended decline in HSI and Copper will put additional pressure to Aussie.

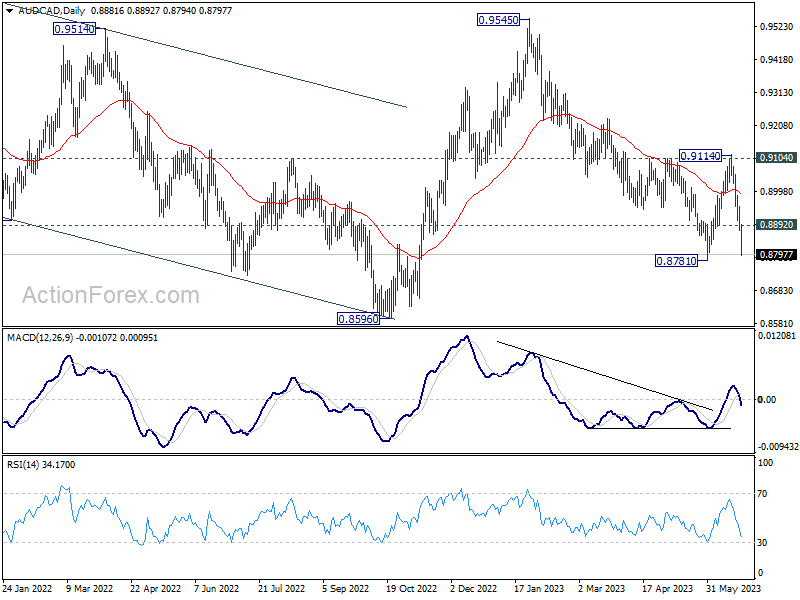

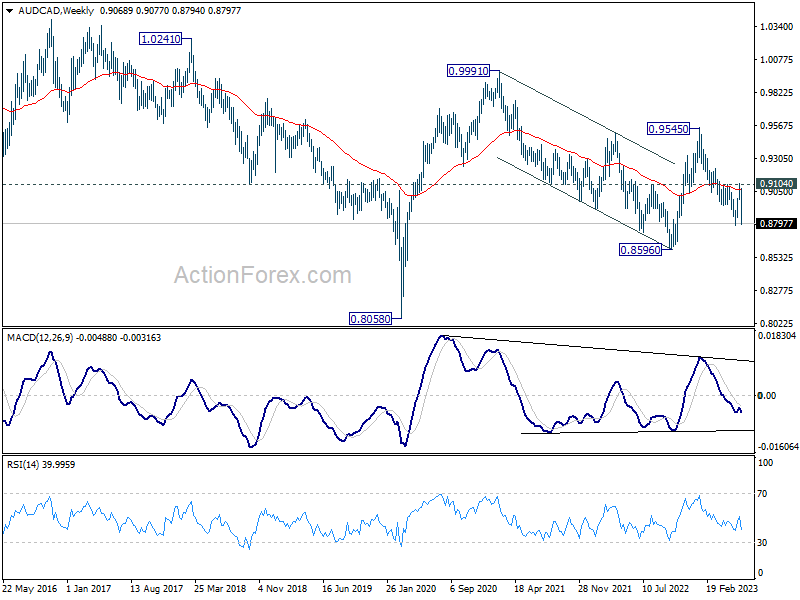

AUD/CAD was the top mover last week, losing as much as -3.15%. the development should confirmed that rebound from 0.8781 has completed at 0.9114, after rejection by 0.9104 resistance.

Immediate focus is now on 0.8781 support in the coming days. Firm break there will resume whole down trend from 0.9545 to retest 0.8595 low. There is prospect of resuming whole down trend from 0.9991 (2021 high) in this bearish scenario.

Nevertheless, rebound from current level, followed by break of 0.8892 minor resistance will turn bias neutral first.

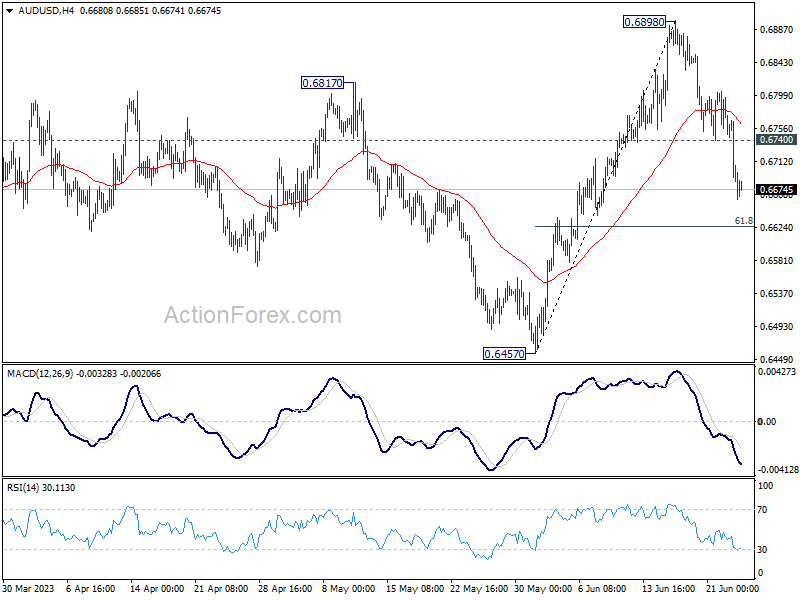

AUD/USD Weekly Report

AUD/USD’s steep decline last week mixed up the near term outlook. But for now, further fall is in favor this week as long as 0.6740 minor resistance holds. Next target is 61.8% retracement of 0.6457 to 0.6898 at 0.6625. On the upside, above 0.6740 will turn intraday bias neutral first.

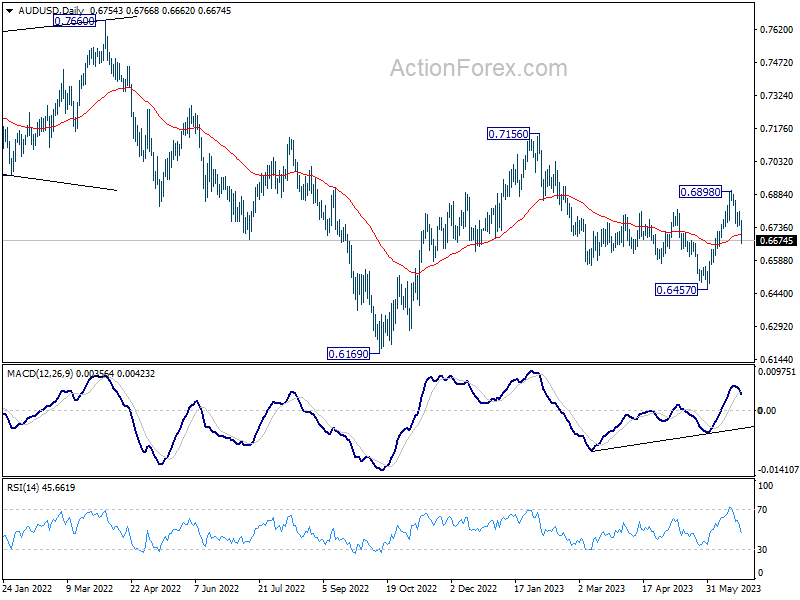

In the bigger picture, price actions from 0.7156 are seen as a correction to the rebound from 0.6169 for now. Break of 55 D EMA (now at 0.6701) raises the chance that it’s in progress. Break of 0.6457 will resume the fall form 0.7156. On the upside, though, break of 0.6898 resistance will argue that rise form 0.6169 is ready to resume through 0.7156.

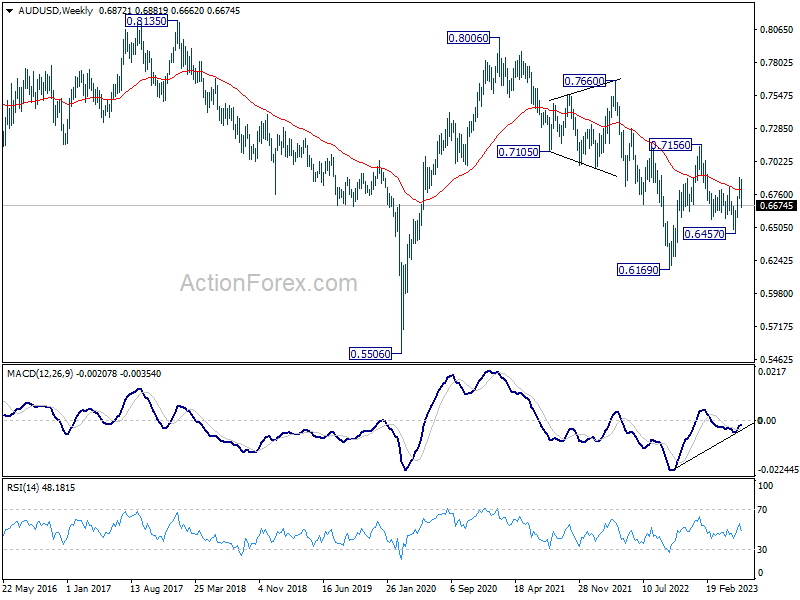

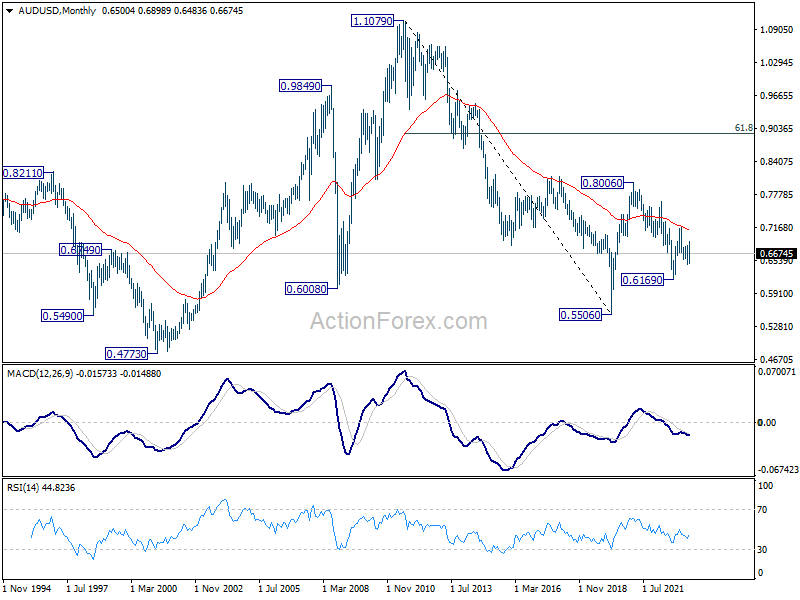

In the long term picture, focus is back on 55 M EMA (now at 0.7119), which is relatively close to 0.7156 resistance. Rejection by this level will maintain medium term bearishness for resuming the down trend from 0.8006 (2021 high) at a later stage. However, sustained break there will argue that the trend has reversed, and rise from 0.5506 (2020 low) might be on track to resume.

{kind=link}