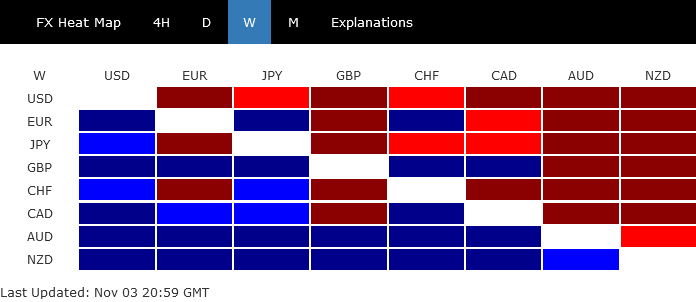

In a week marked by a significant shift in investor sentiment, Dollar found itself at the bottom of the currency heap. A rapid shift to a risk-on attitude was catalyzed by sharp decline in benchmark Treasury yields, fueling an aggressive uptick in stock prices. The surge in equity investments was further amplified when the latest non-farm payroll data bolstered the belief that Fed might have reached the peak of its tightening cycle. Market participants are now keenly watching the extent of the stock market’s rally and the depth of the decline in 10-year yield, which will likely be pivotal factors for Dollar’s short-term direction.

Japanese Yen trailed closely behind Dollar in terms of weak performance, suffering from the dual forces of robust risk appetite and BoJ’s (BoJ) decision to maintain its yield curve control with just tweak, contrary to some investors’ expectations for a significant policy adjustment. Swiss Franc also succumbed to the uplifted risk mood, ranking as the third weakest.

Conversely, New Zealand and Australian Dollars emerged as frontrunners in the currency race, propelled by the narrowing yield gap and escalating risk tolerance. British Pound also capitalized on the upbeat market mood, though to a slightly lesser degree. Meanwhile, Euro and Canadian Dollar displayed a mixed finish.

Optimism abounds as markets cheer dipping yields and goldilocks job data

The mood in financial markets was decidedly bullish last week, with investors piling into stocks, propelling major US indexes to their most robust rally in a year. This surge in risk appetite followed spurred by a substantial decline in Treasury yields from their recent highs. Increased expectation that Fed interest have peaked was further reinforced by weaker than expected job data.

DOW concluded the week with a substantial gain of 5.07%, marking its best performance since October of 2022. S&P 500 and NASDAQ followed suit, jumping 5.85% and 6.61%, respectively, charting their best weeks since November 2022. 10-year Treasury yield nosedived to a low of 4.484% before ending the week slightly higher at 4.558%. This decline in yields was stark, considering the flirtation with 5% level just a week prior. Simultaneously, Dollar Index retreated steeply to a six-week trough, buffeted by a combination of shifting Fed expectations, burgeoning risk-on sentiment, and descending yields.

The spark for the market’s bullish turn was first ignited by the Treasury Department’s announcement of smaller-than-anticipated increases in the issuance of longer-dated Treasury securities. When the Fed maintained its interest rate unchanged at 5.25-5.50% for the second month in a row and Chair Jerome Powell refrained from signaling any additional hawkish intent, it only bolstered the prevailing risk-on mood.

Moreover, the latest non-farm payroll report delivered a surprise to the markets with its underwhelming job growth numbers, a slight uptick in the unemployment rate, and wage growth that lagged expectations. These indicators are seen as signs that Fed’s rigorous efforts to temper the economy and curb inflation are bearing fruit, reducing the need for further rate hikes.

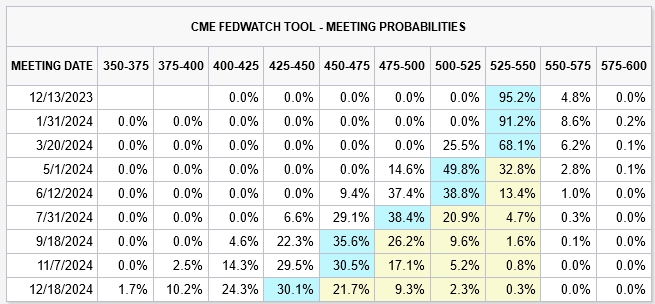

In the aftermath, Fed funds futures are now indicating a mere 4.8% likelihood of a 25 basis point hike at the December meeting. Market conversations are progressively turning towards the prospects of a rate cut, with futures markets pricing in a 64% chance of a cut by May next year, and an 86% probability by June.

S&P 500 index sidestepped the much-feared “October Crash”, with last week’s strong rally suggesting that correction from 4607.07 has possibly concluded 4103.78. Immediate focus is now on 4393.57 resistance. Decisive break there will strengthen near term bullishness, to push S&P 500 through 4607.07 resistance to resume the whole up trend from 3491.58 (2022 low).

Even if this year-end “Santa Claus rally” realizes, it’s uncertain whether bullish momentum is strong enough to push S&P 500 through 4818.62 (2022 high). We’ll leave the assessment for a later stage until there’s clearer evidence of the index’s ability to maintain its upward course.

10-year yield’s break of 4.532 support last week suggests that rise from 3.253 has completed at 4.997, failing to conquer 5% level. It’s now turned into a period of consolidation, with deeper decline in favor. Nevertheless, strong support could emerge around 4.330/333 (38.2% retracement of 3.253 to 4.997 at 4.330). Should TNX find solid ground and rebound from these levels, the current pattern could be interpreted as a mere sideways consolidation, setting the stage for another attempt at challenging the 5% mark in the future. However, sustained break of 4.330 will argue that TNX is already in a larger scale correction, with target on 55 W EMA (now at 3.865) in the medium term.

While Dollar Index’s decline was deep, price actions from 107.34 could still be seen as a correction to the rise from 99.57 only. As long as 38.2.% retracement of 99.57 to 107.34 at 104.37 holds, rise from 99.57 should still resume through 107.34 at a later stage. However, firm break of 104.37 will raise the chance of bearish reversal, or as a correction, drag DXY through 55 W EMA (now at 103.89) to 61.8% retracement at 102.53.

BoJ’s tepid policy tweaks fail to support Yen, NZD/JPY soars

Last week’s highly anticipated BoJ policy meeting concluded with results that fell short of market expectations. Despite widespread speculation of a significant shift in its yield curve control policy, the central bank limited its actions to a minor adjustment in its language, effectively softening the previously rigid cap on the 10-year bond yield. This move was seen as a bid to permit a moderate rise in long-term borrowing costs, diverging slightly from the strict ceiling imposed just a quarter ago.

Governor Kazuo Ueda held firm on BoJ’s longstanding dovish stance, committing to “patiently” maintain its stimulative monetary approach. The underwhelming response from BoJ disappointed investors who had bet on a more substantial policy shift, and as a result, Yen experienced renewed selling pressure. This decline was further exacerbated by the prevailing risk-on mood in global markets.

NZD/JPY was among the top movers in the week, up 2.95%. Current development argues that rise from 80.42 is ready to resume. Further rise is expected as long as 88.45 support holds, to retest 90.18 first. Firm break of 90.18 will confirm this bullish case, and target 61.8% projection of 80.42 to 89.67 from 86.75 at 92.46 next.

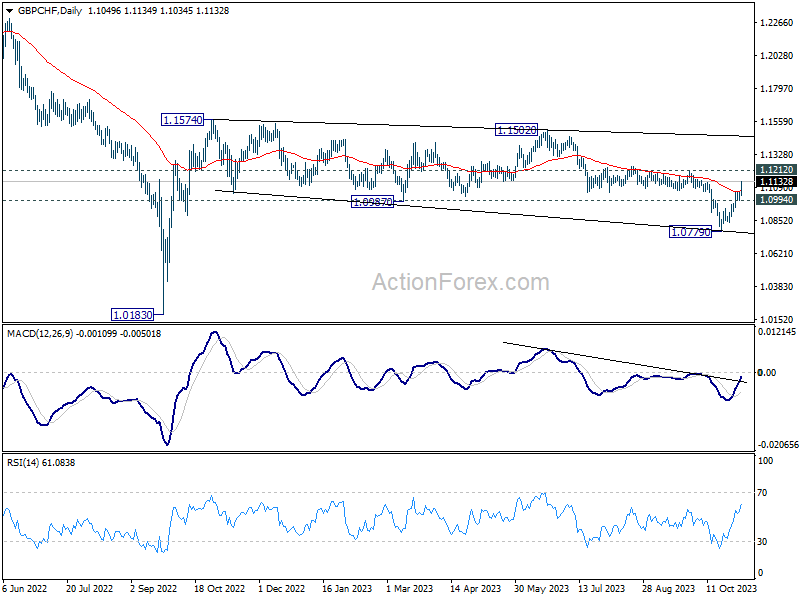

GBP/CHF rallies on risk-on sentiment, overcoming BoE

Sterling has managed to hold its ground amidst a dynamic week in the financial markets, drawing strength from a global risk-on mood which has somewhat cushioned the blow from BoE’s latest policy decision. The MPC concluded with a split 6-3 vote to maintain Bank Rate at its current level of 5.25%. BoE provided a projection path for the Bank Rate, suggesting it would hover around the 5.25% mark until the third quarter of 2024 before anticipating a gradual decline to 4.25% by the end of 2026. The overall announcement aligned with growing consensus that interest rate in the UK have peaked.

GBP/CHF’s strong break of 55 D EMA (now at 1.1065) suggests that fall from 1.1502 has completed at 1.0779. Further rise is expected as long as 1.0994 support holds. Firm break of 1.1212 will bolster the case that whole corrective pattern from 1.1574 has finished too. Stronger rally should then be seen to 1.1502/1574 resistance zone next.

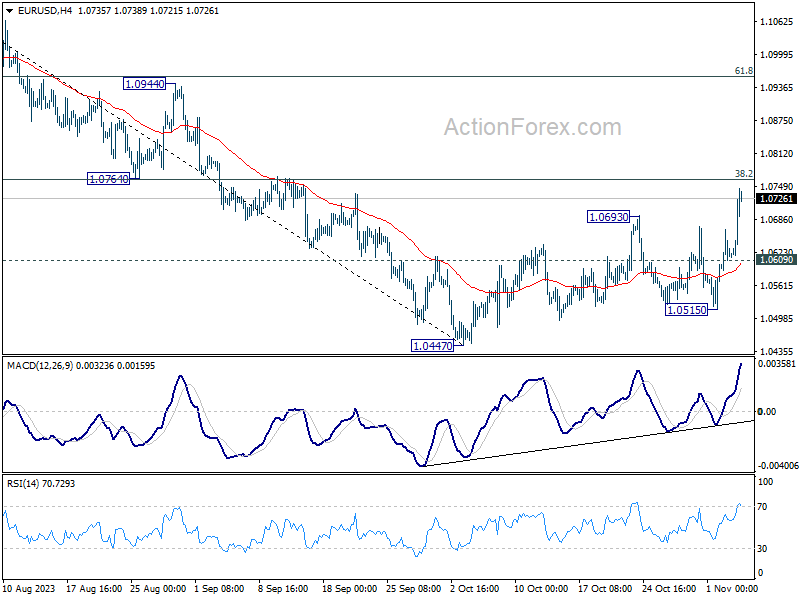

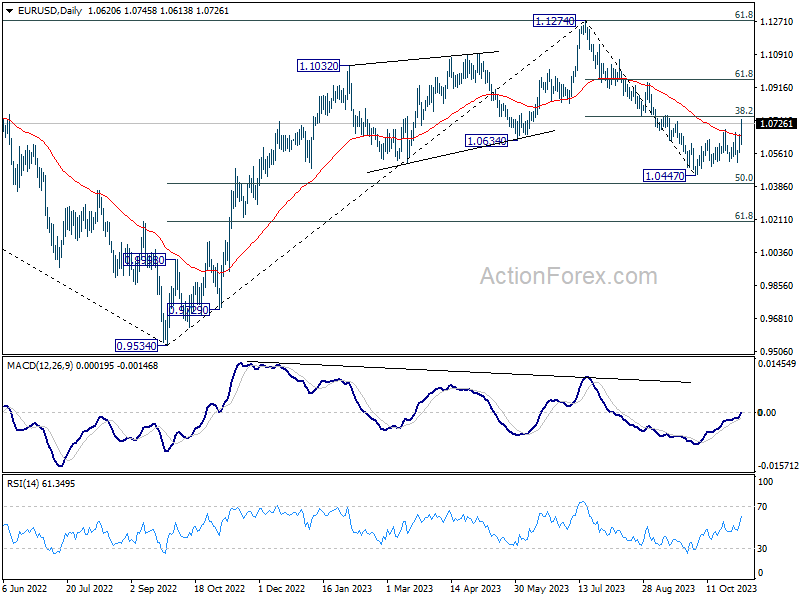

EUR/USD Weekly Outlook

EUR/USD’s rebound from 1.0447 resumed last week and the break of 55 D EMA argues that fall from 1.1274 has completed. Initial bias stays on the upside this week for 1.0764 cluster resistance (38.2% retracement of 1.1274 to 1.0447 at 1.0763). Decisive break there will pave the way to 61.8% retracement at 1.0958 next. On the downside, below 1.0609 minor support will turn intraday bias neutral first.

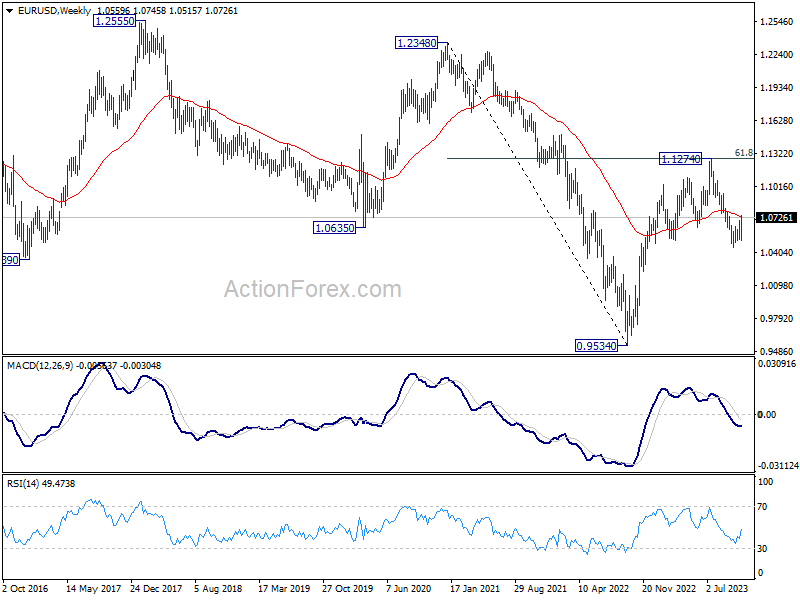

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern to rise from 0.9534 (2022 low). Rise from 1.0447 is tentatively seen as the second leg. Hence while further rally could be seen, upside should be limited by 1.1274 to bring the third leg of the pattern.

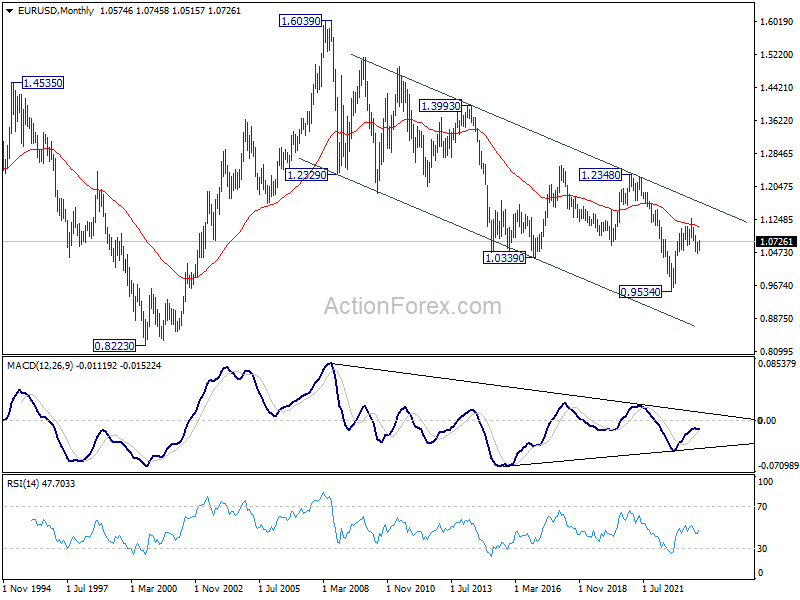

In the long term picture, sustained trading above 55 M EMA (now at 1.1087) is needed to be the first sign of bullish trend reversal. Decisive break of 1.2348 structural resistance is needed to confirm. Otherwise, outlook will be neutral at best.

{kind=link}