Dollar ended last week broadly higher except versus the Japanese Yen. While economic data from the US were generally disappointing, they were not bad enough to alter Fed’s path of three rate hikes this year. Just that, the data didn’t add to the chance of the fourth hike in December. On the other hand, data from Eurozone and UK re-confirmed the slowdown in Q1 and the lack of solid momentum in the rebound in Q2. Such development added to the case for ECB to exit stimulus later, and for BoE to delay the next rate hike. The change in ECB and BoE expectations continued to be reflected in France, Germany and UK stock markets. And equally importantly, German bund yield and UK Gilt yield ended deeply lower. Together with retreat in US treasury yields, they provided the boost to Yen, which ended as the strongest one. And not surprisingly, Sterling and Euro were the biggest losers last week.

Hawkish Fed offset data disappointment, Fed rate path pricing largely unchanged

To recap, US headline PCE accelerated from 1.7% yoy to 2.0% yoy in March. Core PCE also accelerated from 1.6% yoy to 1.9% yoy. That was the main positive set of data last week. ISM manufacturing dropped to from 59.3 to 57.3 in April. ISM services dropped to 56.8, down from 58.8 and missed expectation of 58.1. Finally, non-farm payrolls reports showed only 164k job growth in April, below expectation of 194k. Unemployment rate did drop from 4.0% to 3.9%. But wage growth was disappointing, with average hourly earnings risen merely 0.1% mom versus expectation of 0.2% mom.

Nonetheless, the FOMC statement showed slightly more hawkish tone on inflation. Fed noted that “both overall inflation and inflation for items other than food and energy have moved close to 2%”. That’s somewhat an upgrade fro March description that those barometers “have continued to run below 2%”. Additionally, the members judged that “Inflation on a 12-month basis is expected to run near the Committee’s symmetric 2% objective over the medium- term”. In March, they expected inflation to “move up in coming months” and “to stabilize around the Committee’s 2% objective over the medium- term”. They viewed the risks are “roughly balance” in both meetings. Yet, the reference that “the Committee is monitoring inflation developments closely” was removed in May. This evidenced the members growing confidence that inflation would reach the target as expected. More in FOMC More Hawkish on Inflation, June Rate Hike a Done Deal

After a week of heavy weight events, Fed fund futures are still pricing in 100% odds of a June Fed hike. Chances priced in for September and December rates are largely unchanged. September odd at around 73-4%, December odd at only around 42-43%.

10 year yield extended retreat from 3.035

10 year yield extended the pull back from 3.035 short term top as expected. And thus, it provided little support to Dollar over the week. Stocks were also mainly driven by earnings as DOW engaged in very volatile trading inside recently established range. The pattern from 3.035 so far argues that it’s only in a near term correction. That is, we’re now leaning towards the case of strong support from 55 day EMA (now at 2.845), which is also close to channel support, to contain downside. Retest of 3.036 (2013 high) key resistance could be seen earlier then we originally thought.

Dollar index showed impulsive rally

Dollar index’s solid rally last week was mainly driven by selloff in EUR/USD. But after all, the firm break of 100% projection of 88.25 to 90.29 from 89.22 at 91.90 argues that rise from 88.25 is an impulsive move. That adds to the case of medium term trend reversal. The loss of momentum in some dollar pairs suggests that a near term retreat is possibly due in greenback. But in any case, near term outlook in DXY will remains bullish as long as 90.93 resistance turned support holds. We’d expect further rise ahead to 161.8% projection at 93.55 next. That could hinge on the April CPI figures to be released on Wednesday.

CAC and DAX surged on receding ECB exit expectations

Eurozone GDP growth slowed to 0.4% qoq in Q1, down from prior 0.6% qoq. Headline CPI slowed from 1.3% yoy to 1.2% yoy in April, below expectation of 1.3% yoy. Core CPI was even worse, slowed from 1.0% yoy to 0.7% yoy, below expectation of 0.9% yoy. Would the data give ECB President Mario Draghi and his colleagues better ideas on the factors behind Q1 slowdown? We may get some hints from their comments later. But for now, April’s fall in inflation will definitely trigger some deep thinking in their minds. The questions in the markets remain. That is, will ECB stop the EUR 30B monthly asset purchase program after September? We may not get the answer in June meeting.

The speculation that ECB could extend the asset purchase program, even tapered, drove European stocks high. France CAC 40 is a clear example. It should be noted that French data were not too bad. Yes, Q1 GDP slowed more than expected from 0.7% qoq to 0.4% qoq in France. However, France PMI composite hit a 2-month high in April at 56.9. On the other hand, German PMI composite hit 19-month low at 54.6. France maybe enjoying a stronger rebound in Q2 than others in the region. And that could explain the better performance in CAC 40 than DAX.

CAC 40 extended recent rally from 5038.12 to as high as 5538.73 last week before closing slightly lower at 5516.04. As long as 5388.66 support holds, further rise is expected to 5567.02 high. Based on current momentum, CAC will likely take out this resistance to resume larger up trend.

While DAX underperformed CAC, it did manage to break through 12601.46 resistance firmly. The development suggests that pull back from 13596.89 is completed at 11726.62. And further rise would be seen to retest 13596.89.

BoE projections and voting watched again

UK PMI manufacturing dropped from 55.1 to 53.9 in April, below expectation of 54.8. Construction PMI was a surprise that rose from 47.0 to 52.5 and beat expectation of 50.5. UK Services PMI rose from 51.7 to 51.8, but missed expectation of 53.5. Collectively, the PMI data suggested that rebound in Q2 was far from being strong. And as Markit noted in the release, “the three PMI surveys collectively showed only a muted rebound in business activity after being disrupted by heavy snowfall in March, failing to regain February’s pace of growth to suggest that the underlying performance of the economy has continued to deteriorate.” And the data will ” add to expectations that the MPC will take its finger firmly off the rate hike trigger. Any further slowing will also raise questions as to whether the November rate hike may have been ill-timed.”

BoE is now not expected to raise interest rate in the coming Thursday on May 10. Nonetheless, it could still be market moving. Firstly, BoE will release the quarterly Inflation Report and we’ll see how the data released in the past three months affect the growth and inflation projections. Secondly, it would be interesting to see if the two known hawks, Ian McCafferty and Michael Saunders, would change their mind and refrain from voting for rate hike again.

FTSE’s rally from 6866.93 continued last week and reached as high as 7572.98. With the help of receding BoE hike expectation, and depreciation of Sterling, we’d expect the index to extend such rise to retest 7792.56 high next.

Falling European yields were behind steep fall in EUR/JPY and GBP/JPY

Finally, we’d like to point out that German bund 10 year yield and UK Gilt 10 year yield have been in down trend since since late May. That’s very much due to weak data as well as expectations on ECB and BoE rate path. It’s seems rather apparent that EUR/JPY and GBP/JPY are following the path of bund and gilt yields since the start of the year, rather than risk sentiments. And for the same reason, even though Dollar was strong, Yen was stronger as US 10 year yield retreated.

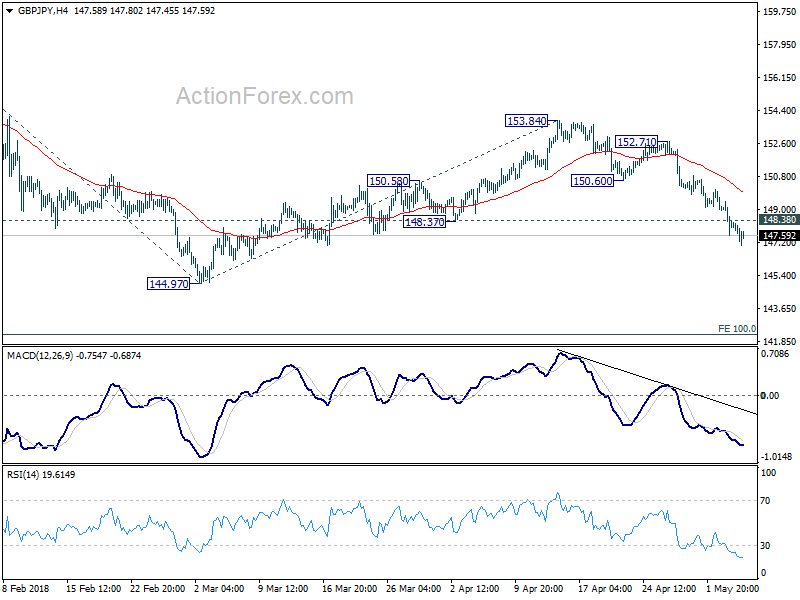

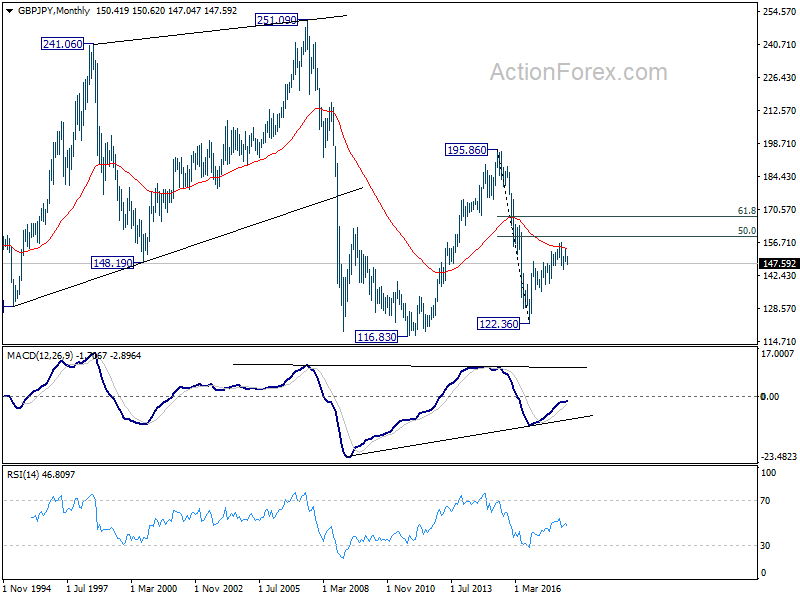

GBP/JPY Weekly Outlook

GBP/JPY’s fall from 153.84 accelerated to as low as 147.04 last week. The development is in line with our view that corrective rise from 144.97 has completed at 153.84 already. And whole fall from 156.59 could be resuming. Initial bias stays on the downside this week for 144.97 low first. Break there will target 100% projection of 156.59 to 144.97 from 153.84 at 142.22 next. On the upside, above 148.38 minor resistance will turn intraday bias neutral and bring recovery. But upside should be limited well below 150.60 support turned resistance to bring another decline.

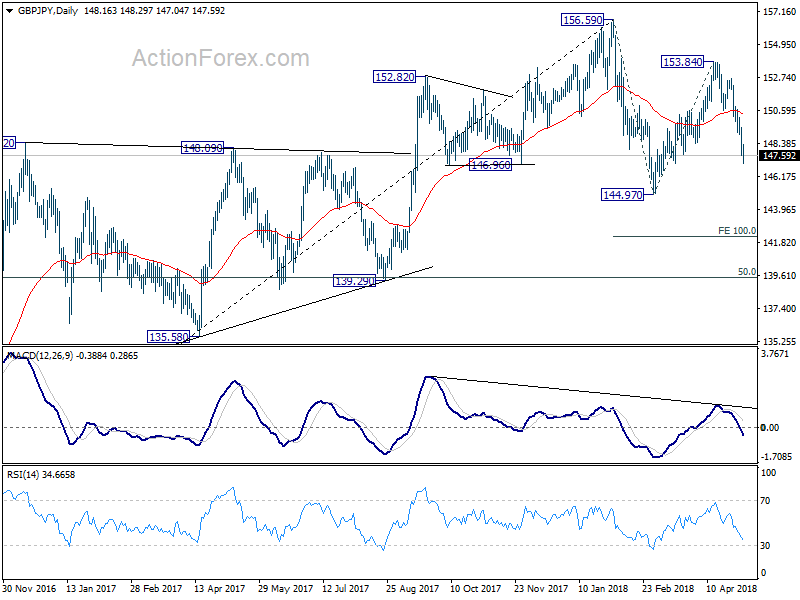

In the bigger picture, for now, we’re treating price actions from 156.59 as a corrective move. Therefore, while deeper fall is expected, strong support should be seen above 139.29 cluster support (50% retracement of 122.36 to 156.59 at 139.47) to contain downside and bring rebound. There is still prospect of extending the rise from 122.36. However, considering that GBP/JPY failed to sustain above 55 month EMA (now at 153.94), firm break of 139.29 will confirm trend reversal and turn outlook bearish.

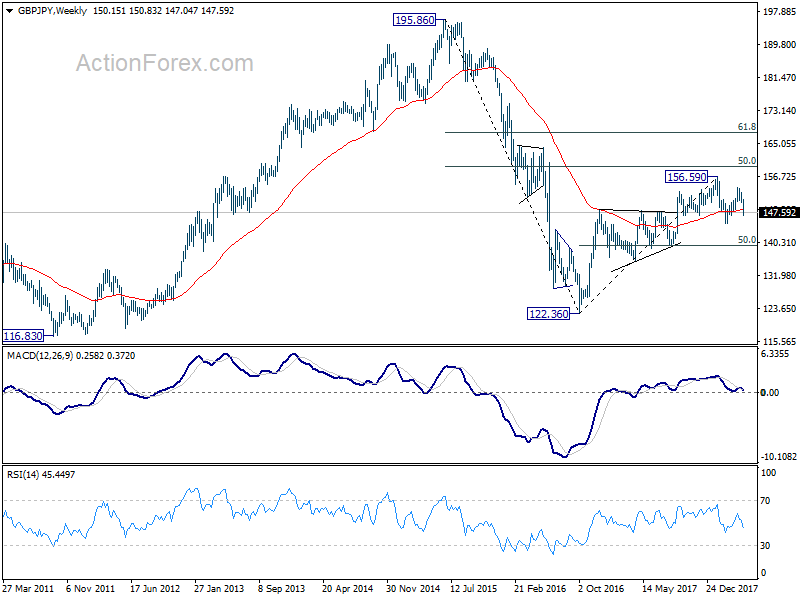

In the longer term picture, the failure to sustain above 55 month EMA (now at 153.94) is mixing up the outlook. Nonetheless, as long as 139.29 holds, rise from 122.26 is in favor to extend to 50% retracement of 195.86 (2015high) to 122.36 (2016 low) at 159.11, and possibly further to 61.8% retracement at 167.78 before completion. However, firm break of 139.29 will turn focus back to 116.83/122.36 support zone instead.

{kind=link}