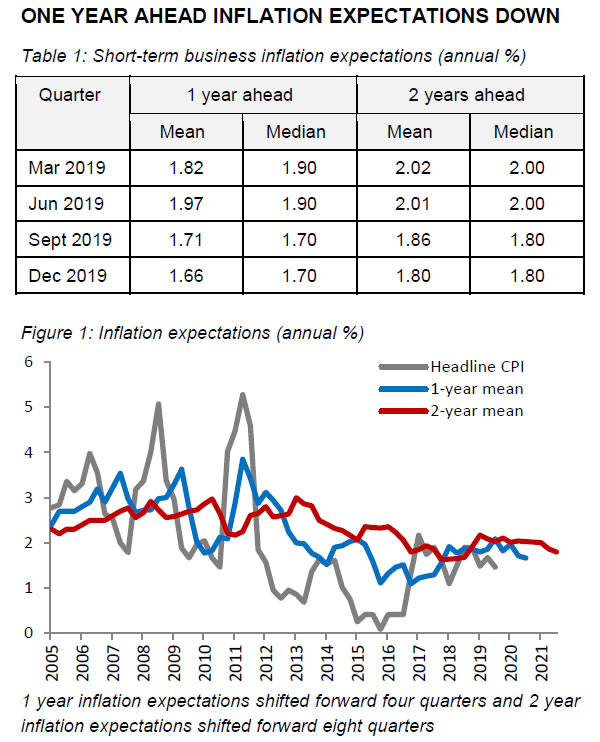

In RBNZ’s quarterly Survey of Expectations report, inflation expectation for one year ahead dropped from 1.71% to 1.66%. Expectations for two years ahead also dropped from 1.86% to 1.80%. Mean expectation for the end of quarter OCR dropped from 1.32% to 0.79%. One year expectations also dropped form 1.13 to 0.61%.

The release solidify the case for another RBNZ rate cut to 0.75% tomorrow. The key now is whether RBNZ would give any indication of easing bias, even after the cut. In particular, traders would look for phrase like “there is scope for further fiscal and monetary easing if necessary.”

UK employment dropped -58k, largest contraction in four years

UK total employment dropped -58k in the three months to September. That’s the biggest contraction in the job markets in four years, taking employment total down to 32.75m. Unemployment rate dropped to 3.8% in September, down from 3.9%, and beat expectation of 3.9%. Unemployment also dropped -23k ti 1.31m. The set of data suggests that more people have dropped out of the labor market and stopped looking for work.

Wage growth also slowed notably. Average weekly earnings including bonus rose 3.6% 3moy, missed expectation of 3.8% 3moy. Average weekly earnings excluding bonus also slowed to 3.6% 3moy, down from 3.8% 3moy, missed expectations.

Full release here.