Despite all the political pressure, Fed is widely expected to raise federal funds rate by 25bps to 2.25-2.50% today. The meeting bears much more importance then just the rate hike, as investors would be eager to know Fed’s rate path in 2019, which has become pretty unsure recently. The statement, voting, and economic projections could all play a part in shaping market expectations.

In the November statement, Fed concluded by saying that “In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its maximum employment objective and its symmetric 2 percent inflation objective. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments.”

That is, Fed based its decision on a wide range of meaningful data rather than just a few pieces of them. While Chair Jerome Powell might put more emphasis on data dependency, the statement itself is clear and comprehensive enough that doesn’t warrant a change.

Fed’s Septemebr projections.

On economic projections, the most important part is federal funds rate projections. As a recap, back in September, the longer run federal funds rate was estimated to be at 3.0%, with central tendency at 2.8-3.0% and 2.5-3.5%. Despite financial market volatility and signs of peaking growth momentum, it still a consensus among fed policies to lift rate to neutral. And if we take the central tendency as consensus, there should be at least one to two more rate hikes onwards.

But timing is the question. For 2019, the median federal funds rate projection was at 3.1%, with central tendency at 2.9-3.4%. That means, members leaned towards two to three more hikes in 2019, if economic conditions favored. At the same time, that would mean interest rate would go pass neutral a little.

While we won’t expect many changes to the projections, we won’t be surprised to see some. And changes or not, Dollar would be volatile on the figures.

Suggested readings on FOMC:

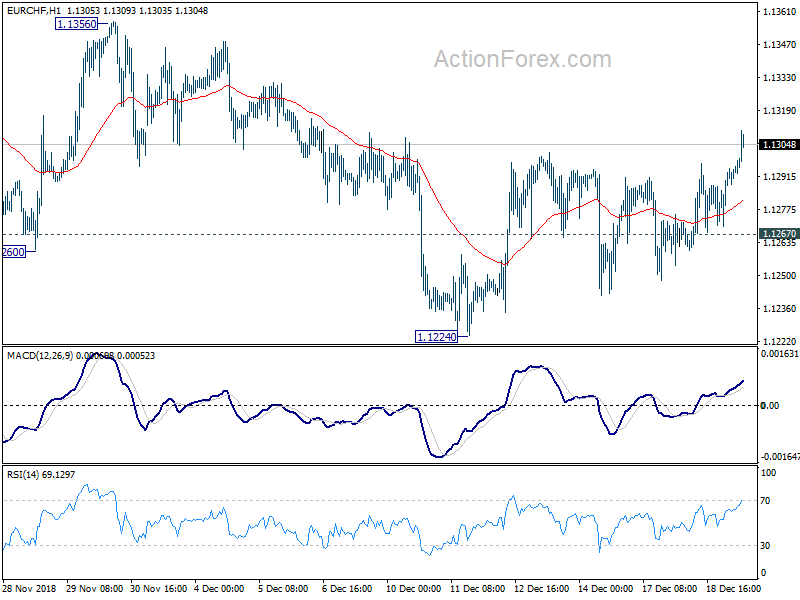

Into US session: Euro strongest as Italian budget deal made, Dollar soft ahead of FOMC

Entering US session, Euro is trading as the strongest one today. European Commission finally agreed with Italy on its 2019 budget, thus the so called “Excessive Deficit Procedure”. Italian 10 year yield tumble to as low as 2.778. German-Italian spread also narrowed to 253. Swiss Franc is, as a result of relief rally in European stocks too, trading as the weakest one for today. Dollar is the second weakest as markets await FOMC rate decision.

In short, Fed is widely expected to raise federal funds rate by 25bps to 2.25-2.50% today. The question is on the rate path in 2019 after all the political pressures Fed policymakers faced. The new economic projections will provide the key guidance to market expectations. More on the projections here.

Also, here are some suggested readings on FOMC:

In European markets, at the time of writing:

Earlier in Asia: