Fed left federal funds rate unchanged at 1.50-1.75% as widely expected. And the decision was made with unanimous vote. Fed maintained tightening bias and noted that “the Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate”.

Descriptions on the economy are slightly upbeat as “job gains have been strong” and “business fixed investments continued to growth strongly”. But “household spending moderated”. While core inflation moved “close to 2percent”, “market-based measures of inflation compensation remain low”.

The tone is cautiously upbeat and give no hints of more than three hikes this year.

Here is the full statement:

Information received since the Federal Open Market Committee met in March indicates that the labor market has continued to strengthen and that economic activity has been rising at a moderate rate. Job gains have been strong, on average, in recent months, and the unemployment rate has stayed low. Recent data suggest that growth of household spending moderated from its strong fourth-quarter pace, while business fixed investment continued to grow strongly. On a 12-month basis, both overall inflation and inflation for items other than food and energy have moved close to 2 percent. Market-based measures of inflation compensation remain low; survey-based measures of longer-term inflation expectations are little changed, on balance.

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee expects that, with further gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace in the medium term and labor market conditions will remain strong. Inflation on a 12-month basis is expected to run near the Committee’s symmetric 2 percent objective over the medium term. Risks to the economic outlook appear roughly balanced.

In view of realized and expected labor market conditions and inflation, the Committee decided to maintain the target range for the federal funds rate at 1-1/2 to 1-3/4 percent. The stance of monetary policy remains accommodative, thereby supporting strong labor market conditions and a sustained return to 2 percent inflation.

In determining the timing and size of future adjustments to the target range for the federal funds rate, the Committee will assess realized and expected economic conditions relative to its objectives of maximum employment and 2 percent inflation. This assessment will take into account a wide range of information, including measures of labor market conditions, indicators of inflation pressures and inflation expectations, and readings on financial and international developments. The Committee will carefully monitor actual and expected inflation developments relative to its symmetric inflation goal. The Committee expects that economic conditions will evolve in a manner that will warrant further gradual increases in the federal funds rate; the federal funds rate is likely to remain, for some time, below levels that are expected to prevail in the longer run. However, the actual path of the federal funds rate will depend on the economic outlook as informed by incoming data.

Voting for the FOMC monetary policy action were Jerome H. Powell, Chairman; William C. Dudley, Vice Chairman; Thomas I. Barkin; Raphael W. Bostic; Lael Brainard; Loretta J. Mester; Randal K. Quarles; and John C. Williams.

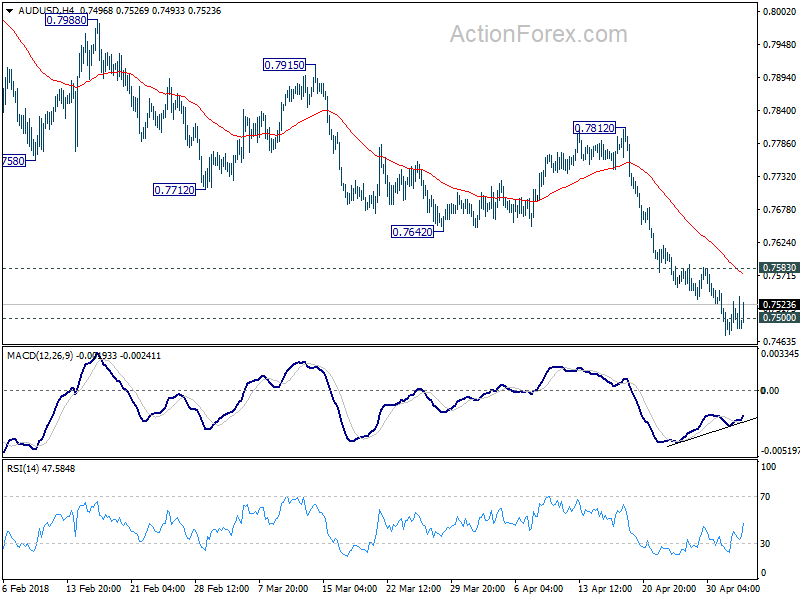

Non-farm payroll and wage growth missed expectations, unemployment rate dropped to lowest since 2000

US non-farm payrolls rose 164k in April, below expectation of 194k. Prior month’s figure was revised up from 103k to 135k.

Unemployment rate dropped to 3.9% , down from 4.1% and beat expectation of 4.0%. That’s the lowest level since the end of 2000.

Average hourly earnings rose 0.1% mom only, below expectation of 0.2% mom.

Notable buying is seen in the Japan yen after the report, with USD/JPY driving to as low as 108.65 so far. But Dollar is steady against Euro, Swiss, Sterling, Aussie and Canadian, in tight range.