ECB President Mario Draghi’s full press conference statment below:

Ladies and gentlemen, the Vice-President and I are very pleased to welcome you to our press conference. We will now report on the outcome of today’s meeting of the Governing Council.

Based on our regular economic and monetary analyses, we decided to keep the key ECB interest rates unchanged. We continue to expect them to remain at their present levels for an extended period of time, and well past the horizon of our net asset purchases.

Regarding non-standard monetary policy measures, we confirm that our net asset purchases, at the current monthly pace of €30 billion, are intended to run until the end of September 2018, or beyond, if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim. The Eurosystem will continue to reinvest the principal payments from maturing securities purchased under the asset purchase programme for an extended period of time after the end of its net asset purchases, and in any case for as long as necessary. This will contribute both to favourable liquidity conditions and to an appropriate monetary policy stance.

Following several quarters of higher than expected growth, incoming information since our meeting in early March points towards some moderation, while remaining consistent with a solid and broad-based expansion of the euro area economy. The underlying strength of the euro area economy continues to support our confidence that inflation will converge towards our inflation aim of below, but close to, 2% over the medium term. At the same time, measures of underlying inflation remain subdued and have yet to show convincing signs of a sustained upward trend. In this context, the Governing Council will continue to monitor developments in the exchange rate and other financial conditions with regard to their possible implications for the inflation outlook. Overall, an ample degree of monetary stimulus remains necessary for underlying inflation pressures to continue to build up and support headline inflation developments over the medium term. This continued monetary support is provided by the net asset purchases, by the sizeable stock of acquired assets and the ongoing and forthcoming reinvestments, and by our forward guidance on interest rates.

Let me now explain our assessment in greater detail, starting with the economic analysis. Real GDP increased by 0.7%, quarter on quarter, in the fourth quarter of 2017, following similar growth in the previous quarter. This resulted in an average annual growth rate of 2.4% in 2017 – the highest since 2007. The latest economic indicators suggest some moderation in the pace of growth since the start of the year. This moderation may in part reflect a pull-back from the high pace of growth observed at the end of last year, while temporary factors may also be at work. Overall, however, growth is expected to remain solid and broad-based. Our monetary policy measures, which have facilitated the deleveraging process, should continue to underpin domestic demand. Private consumption is supported by ongoing employment gains, which, in turn, partly reflect past labour market reforms, and by growing household wealth. Business investment continues to strengthen on the back of very favourable financing conditions, rising corporate profitability and solid demand. Housing investment continues to improve. In addition, the broad-based global expansion is providing impetus to euro area exports.

The risks surrounding the euro area growth outlook remain broadly balanced. However, risks related to global factors, including the threat of increased protectionism, have become more prominent.

Euro area annual HICP inflation increased to 1.3% in March 2018, from 1.1% in February. This reflected mainly higher food price inflation. On the basis of current futures prices for oil, annual rates of headline inflation are likely to hover around 1.5% for the remainder of the year. Measures of underlying inflation remain subdued overall. Looking ahead, they are expected to rise gradually over the medium term, supported by our monetary policy measures, the continuing economic expansion, the corresponding absorption of economic slack and rising wage growth.

Turning to the monetary analysis, broad money (M3) continues to expand at a robust pace, with an annual growth rate of 4.2% in February 2018, slightly below the narrow range observed since mid-2015. M3 growth continues to reflect the impact of the ECB’s monetary policy measures and the low opportunity cost of holding the most liquid deposits. Accordingly, the narrow monetary aggregate M1 remained the main contributor to broad money growth, continuing to expand at a solid annual rate.

The recovery in the growth of loans to the private sector observed since the beginning of 2014 is proceeding. The annual growth rate of loans to non-financial corporations stood at 3.1% in February 2018, after 3.4% in January and 3.1% in December 2017, while the annual growth rate of loans to households remained unchanged at 2.9%. The euro area bank lending survey for the first quarter of 2018 indicates that loan growth continues to be supported by increasing demand across all loan categories and a further easing in overall bank lending conditions for loans to enterprises and loans for house purchase.

The pass-through of the monetary policy measures put in place since June 2014 continues to significantly support borrowing conditions for firms and households, access to financing ‒ notably for small and medium-sized enterprises ‒ and credit flows across the euro area.

To sum up, a cross-check of the outcome of the economic analysis with the signals coming from the monetary analysis confirmed the need for an ample degree of monetary accommodation to secure a sustained return of inflation rates towards levels that are below, but close to, 2% over the medium term.

In order to reap the full benefits from our monetary policy measures, other policy areas must contribute decisively to raising the longer-term growth potential and reducing vulnerabilities. The implementation of structural reforms in euro area countries needs to be substantially stepped up to increase resilience, reduce structural unemployment and boost euro area productivity and growth potential. Against the background of overall limited implementation of the 2017 country-specific recommendations, greater reform effort is necessary in euro area countries. Regarding fiscal policies, the ongoing broad-based expansion calls for rebuilding fiscal buffers. This is particularly important in countries where government debt remains high. All countries would benefit from intensifying efforts towards achieving a more growth-friendly composition of public finances. A full, transparent and consistent implementation of the Stability and Growth Pact and of the macroeconomic imbalance procedure over time and across countries remains essential to increase the resilience of the euro area economy. Improving the functioning of Economic and Monetary Union remains a priority. The Governing Council urges specific and decisive steps to complete the banking union and the capital markets union.

We are now at your disposal for questions.

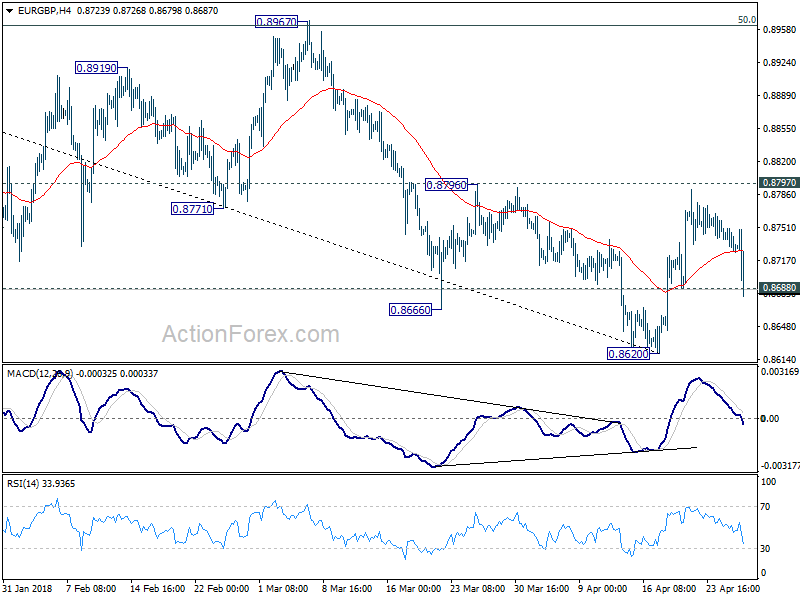

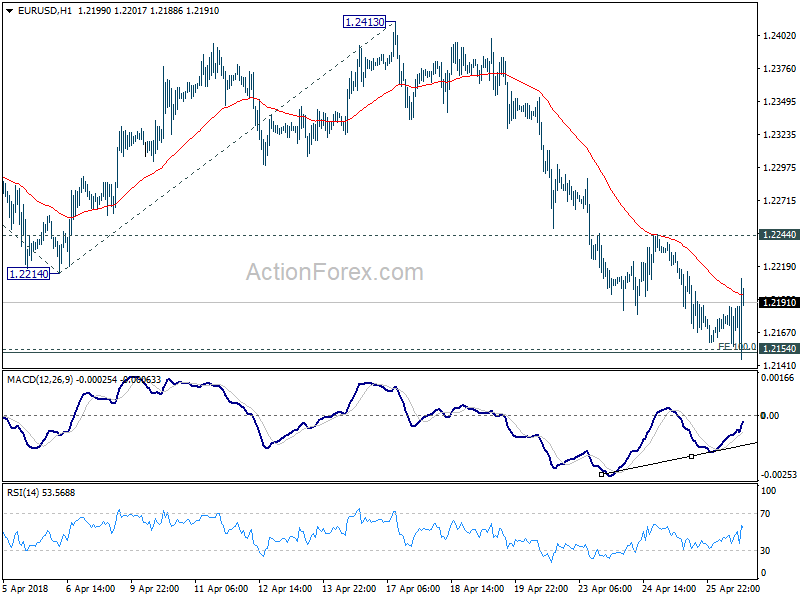

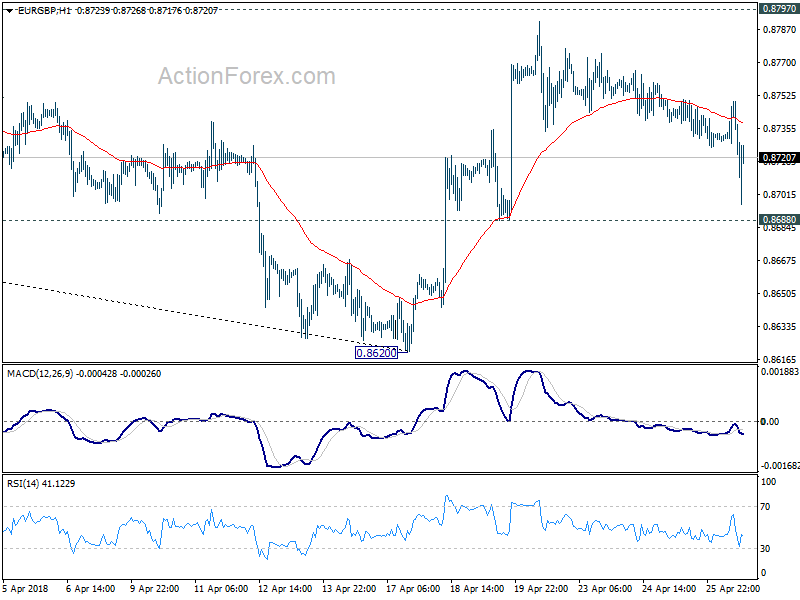

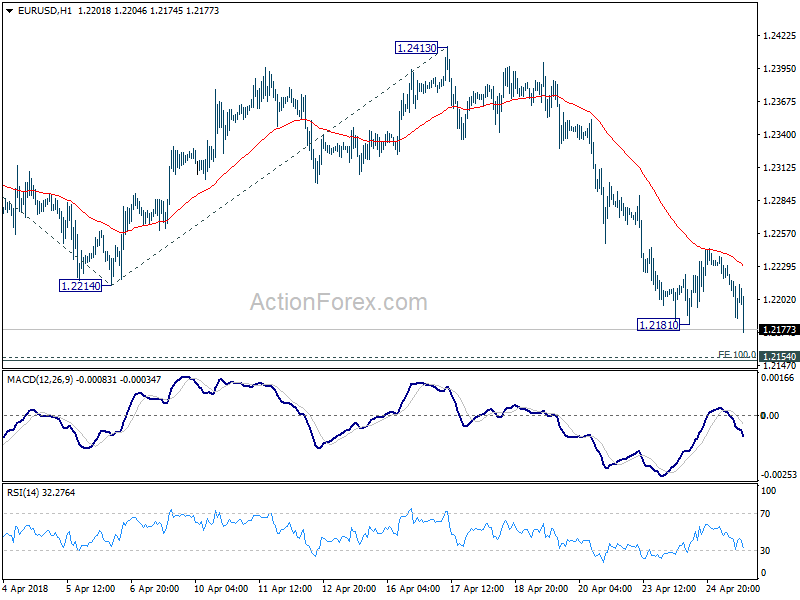

Fresh selling in Euro as France Q1 GDP missed, rose 0.3% qoq only

Fresh selling seen in Euro after French data miss. French GDP growth slowed to 0.3% qoq in Q1, down from prior quarter’s 0.7% qoq and missed expectation of 0.4% qoq. Annual rate decelerated to 2.1% yoy, down from 2.6% yoy, and missed expectation of 2.3% yoy.

The title of this report ECB: Wondering Rather than Worrying summed up yesterday’s ECB press conference rather well. And with French GDP miss, dovish expectation on next week’s Eurozone GDP release could pile up. We’ll see if the coming data clear up the picture for ECB so that policymakers don’t need to wonder any more, but start to worry.

For now, EUR/USD is on course for 1.2 handle. Selling in EUR/USD also spill over to other pairs and lifted the USD. USD/CHF takes out 0.99 and would now be heading back to 1.000. GBP/USD breaks yesterday’s low at 1.3894, just ahead of UK GDP data, an hour away.