Here are the latest developments in global markets:

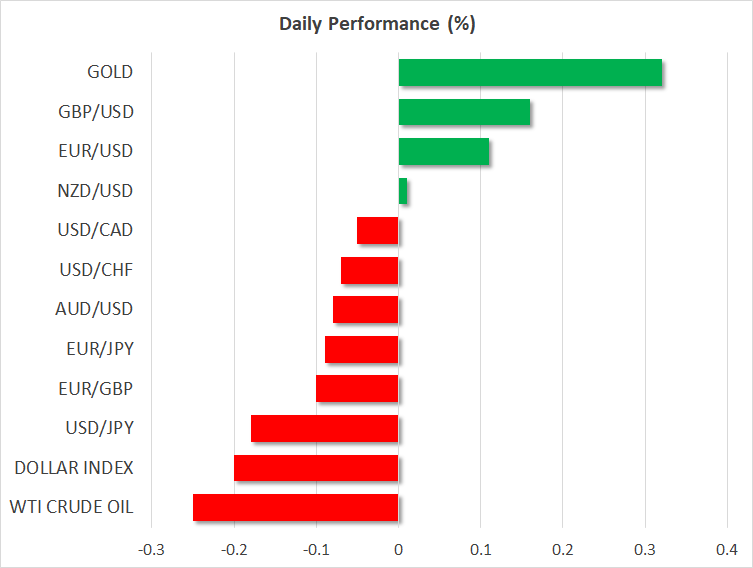

FOREX: The US dollar index – which tracks the greenback’s performance versus a basket of six major currencies – was down by 0.2% on Thursday, extending the losses it posted the previous day. The pullback was mainly owed to a rebound in the euro, the currency that holds more than 50% of the weight in the dollar index. Meanwhile, the Canadian dollar surged following some hawkish hints from the nation’s central bank.

STOCKS: US markets rebounded sharply on Wednesday, as concerns surrounding the European political saga eased somewhat. The S&P 500 and the Dow Jones climbed by 1.27% and 1.26% respectively, with the recovery in both led by the energy and financial sectors, while the tech-heavy Nasdaq Composite rose by 0.89%. That said, sentiment seems to have soured today, as futures tracking the S&P, Dow, and Nasdaq 100, are all pointing to a slightly lower open. Asia was a sea of green on Thursday, with Japan’s Nikkei 225 and Topix gaining 0.83% and 0.65% correspondingly, while in Hong Kong, the Hang Seng advanced by 0.98%. Meanwhile in Europe, futures following all the major benchmarks are well-into positive territory, signaling a notably higher open for these indices today.

COMMODITIES: Oil prices recovered notably yesterday alongside investors’ risk appetite, though the precious liquid is on the back foot again on Thursday. WTI is down by 0.25% and Brent by 0.4% today, following the release of the private API inventory data overnight that showed a build in crude stockpiles, instead of the projected drawdown. The official EIA inventory data are due out today, at 1500 GMT. In precious metals, gold is up by 0.3% today – most probably due to the pullback in the US dollar – and is currently trading near the $1,305 per ounce mark. The yellow metal is now just below its 200-day moving average, located at $1,307, and it will be crucial to see whether the bulls can break above it; price advances were rejected from that hurdle three times now over the past week.

Major movers: Loonie surges as BoC lays groundwork for July hike; euro rebounds

The Bank of Canada (BoC) remained on hold yesterday, as was widely anticipated. In the statement accompanying the decision, the Bank adopted a clearly more hawkish stance, noting that “developments since April further reinforce (the) Governing Council’s view that higher interest rates will be warranted”. Equally, or perhaps more importantly, it erased a repeated reference in prior statements that it will remain “cautious” in raising rates. Overall, policymakers maintained a relatively upbeat tone, laying the groundwork for a rate increase as soon as at their next meeting in July, which market pricing currently assigns a 64% probability to.

The loonie surged against the US dollar, with the move also aided by a rebound in oil prices. Assuming Canadian data hold up over the next weeks, and that there is no negative news on the NAFTA front or another pullback in oil prices, it wouldn’t be a surprise to see the currency continue to recover ground as investors move to fully factor in a move in July.

Turning to Europe, the common currency rebounded across the board yesterday, as the extreme moves in European bond markets retraced. Yields on Italian and other EU peripheral bonds fell back somewhat, indicating that investors were willing to hold those nations’ debt again as the risks surrounding the European political scene appeared to have eased a little, for now.

Italy’s President announced he will allow the two populist parties more time to attempt to form a government, which was likely seen as diminishing the likelihood for early elections – an event that could see the popularity of anti-establishment parties surge further. A surprisingly strong set of inflation readings across European countries probably aided the euro’s recovery, on speculation for a similar reaction in the bloc’s headline CPI rate today. That said, with the Italian situation still up in the air and the prospect of Spanish PM Rajoy facing a no-confidence vote soon, politics could remain the overarching theme for the euro over the next weeks, with price action likely to remain volatile and headline-driven.

On the trade front, reports on Wednesday suggested China is looking to line up other Asian and European nations against the US. This follows the recent announcement from the White House that it may still impose import tariffs on $50bn goods, unless China addresses the issue of alleged US intellectual properly theft.

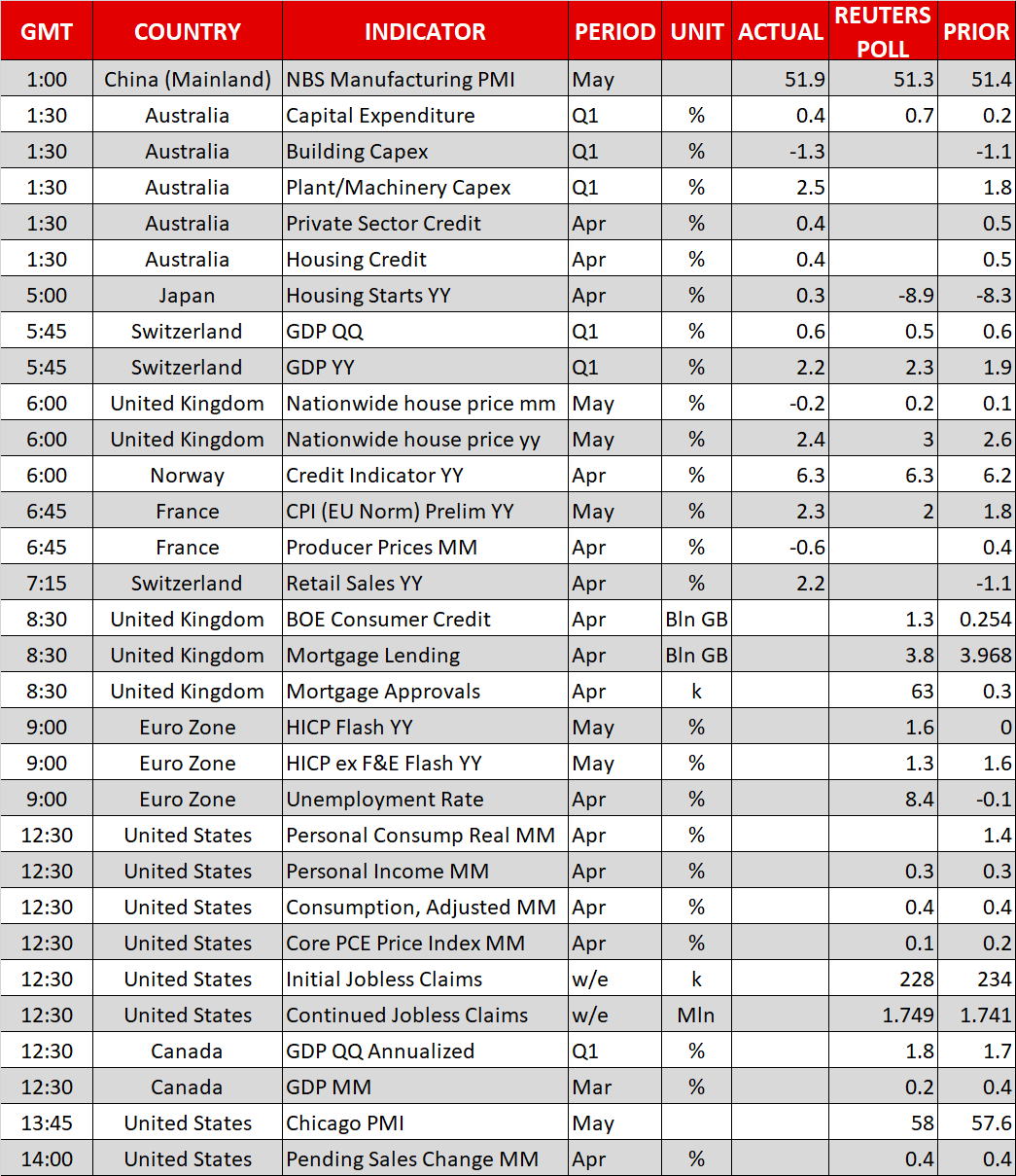

Day ahead: Eurozone inflation, US core PCE and Canadian GDP on the agenda; politics and trade developments eyed

Thursday’s calendar features numerous important releases, including eurozone inflation data and US figures on personal income and consumption, as well as the core PCE inflation gauge. Beyond these, political and trade developments remain on the forefront.

At 0830 GMT, UK data on consumer credit, as well as on mortgage lending and approvals, all relating to the month of April, will be made public.

Having much greater potential to move markets though, are May’s flash inflation figures out of the eurozone due at 0900 GMT. The headline Harmonised Index of Consumer Prices (HICP) that uses a common methodology across EU countries, is forecast to accelerate to 1.6% y/y, up from April’s 1.2%. Core inflation, that excludes volatile food and energy items, is anticipated to grow by 1.3%, a higher pace relative to April’s 1.1%. A data beat might increase expectations for a faster tightening cycle by the ECB, consequently supporting the euro. April’s unemployment rate out of the eurozone will be released at the same time and it is expected to tick down to 8.4%, its lowest since late 2008.

In terms of euro trading, developments in Italy, and to a lesser extent Spain, should be kept in mind. Yesterday, concerns over Italy eased and allowed the euro to rally. In this respect though, it is interesting how quickly markets can move from one narrative – one of existential threats to the eurozone – to one projecting a rosier picture; to put it differently, markets may be running ahead of themselves.

US data on personal income and consumption, as well as the core PCE price index, all for April, will be in focus at 1230 GMT. The latter is the Federal Reserve’s preferred inflation gauge. An acceleration in the measure could push back up market expectations for more rate hikes in 2018 by the US central bank. For the record, core PCE is expected to expand by 1.8% y/y, down from March’s 1.9%. This compares to the Fed’s target for annual inflation of 2%. Weekly initial and continued jobless claims data are also due at the same time, while later in the day the US will see the release of the Chicago PMI for May (1345 GMT), and data on pending home sales for April (1400 GMT).

The loonie, which surged yesterday on what was interpreted as a hawkish message by the Bank of Canada, might prove sensitive to today’s Canadian GDP data pertaining to the month of March, as well as the first quarter of the year. The numbers are scheduled for release at 1230 GMT.

The EIA weekly report on crude oil inventories is due at 1500 GMT. Crude stocks are projected to have declined by 1.0 million barrels during the week ending May 25, after rising by around 5.8m in the previously tracked week.

Any updates on global trade are also likely to prove of significance during today’s trading. Just days before US Commerce Secretary Wilbur Ross visits Beijing for talks, the US and China appear to be getting confrontational again, while sources suggest the US will announce plans on the imposition of tariffs on steel and aluminum imported from the EU.

A G7 meeting on “Investing in Growth that Works for Everyone” that features finance ministers and central bankers will be running until June 2. Meanwhile, Bank of Canada Deputy Governor Sylvain Leduc will be giving a speech at 1635 GMT.

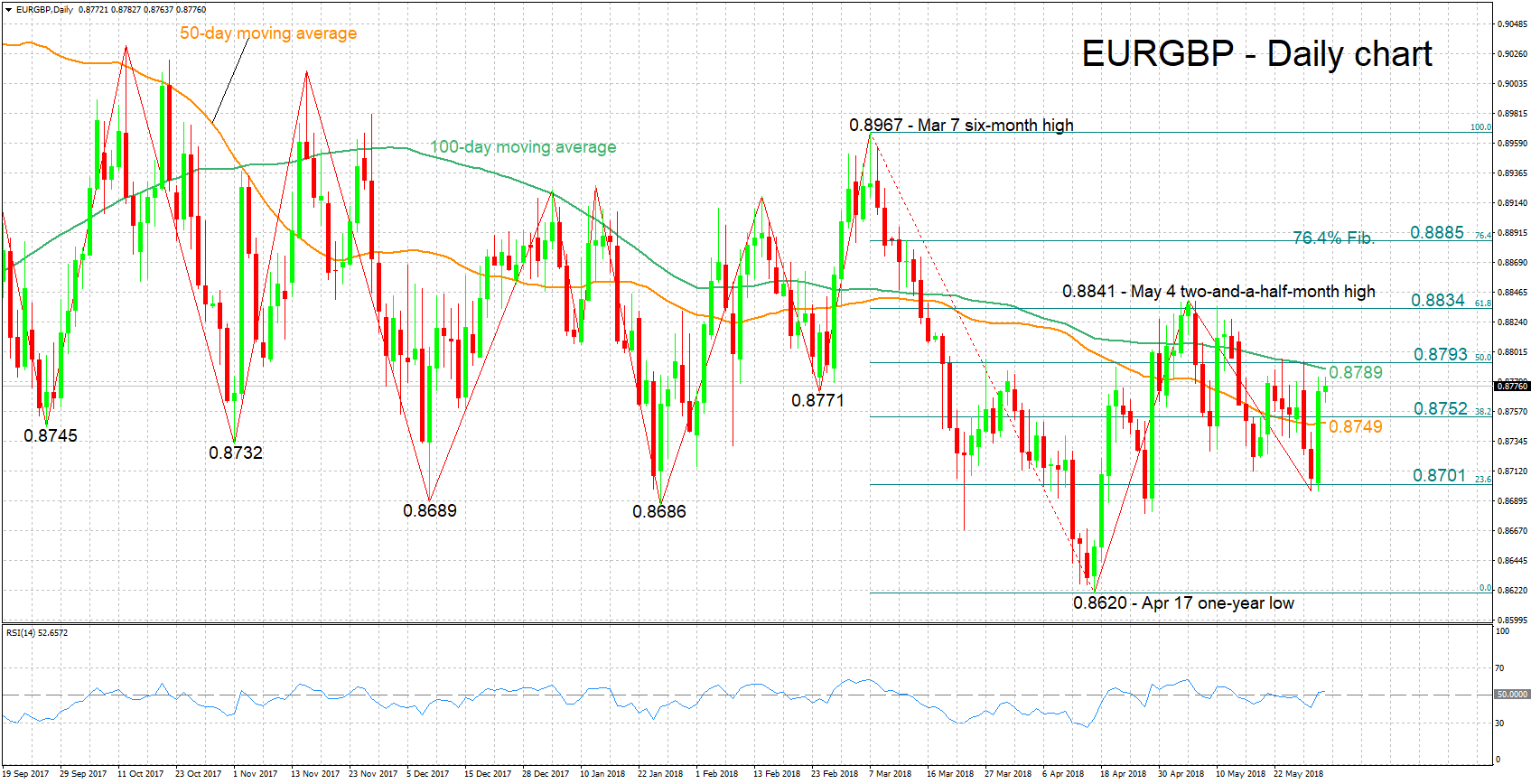

Technical Analysis: EURGBP looking mostly neutral in the short-term

EURGBP added 0.75% on Wednesday, making up for losses from earlier in the week. The RSI has been hovering around the 50 neutral-perceived level recently, projecting a predominantly neutral short-term picture.

A data beat on the eurozone inflation front is likely to boost the pair. Immediate resistance seems to be taking place around the 50% Fibonacci retracement level of the March 7 to April 17 downleg at 0.8793; the current level of the 100-day moving average line at 0.8789 is also part of the area around this level. An upside break would turn the attention to the region around the 61.8% Fibonacci mark at 0.8834.

Weaker-than-anticipated inflation numbers, on the other hand, are expected to push EURGBP lower. Support could come around the 38.2% Fibonacci level at 0.8752 – including the 50-day MA at 0.8749 – and further below from the range around the 23.6% Fibonacci mark at 0.8701.

{kind=link}