{kind=link}

After trading almost solely on politics over the past few days, financial markets will probably turn their gaze back to economics on Friday, when the US releases its employment data at 1230 GMT. Forecasts point to a solid report overall, which could cement market expectations for a June hike – that has come under some doubt lately – and perhaps help the dollar extend its winning streak.

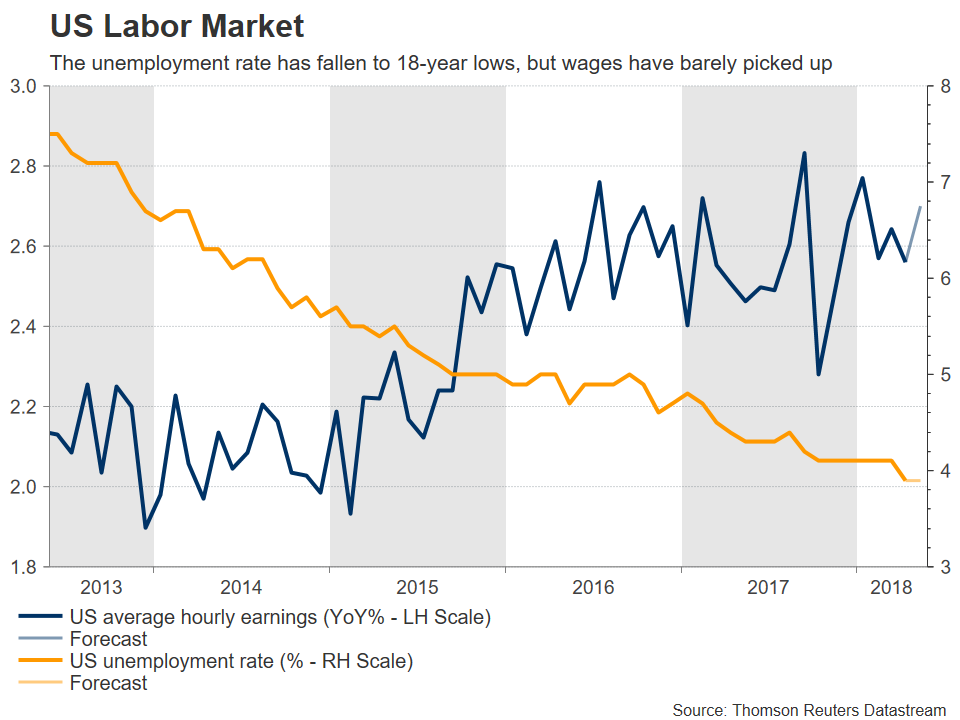

The US labor market is expected to have printed another decent month in May. Nonfarm payrolls (NFP) are forecast to have risen 188k, more than April’s mildly disappointing 164k, and a print consistent with further tightening in the jobs market. The unemployment rate is projected to have held steady at April’s 18-year low of 3.9%, while average hourly earnings are expected to have picked up some speed. In yearly terms, wages are anticipated to have clocked in at 2.7%, from 2.6% in April, and on a monthly basis the print is expected to have risen by 0.2%, up from 0.1% previously.

Similar to recent employment reports, the lion’s share of attention will probably fall on earnings. While payrolls and the unemployment rate are of course extremely important, a strong set of numbers on those fronts would simply confirm what markets and policymakers already know; that jobs growth remains robust. Conversely, wage growth is the missing piece of the puzzle for the Fed; it has long been expected to pick up drastically as the labor market continued to tighten and workers found it easier to demand a pay increase, but it has accelerated only slightly. Remember that higher wages are considered a precursor to higher inflation down the road, so the Fed keeps a very close eye on them. In this light, stronger-than-expected earnings figures could stoke speculation for a more aggressive rate-hike path by the central bank, which would likely be positive for the dollar, and vice versa.

Looking at market pricing, investors have recently become much more skeptical regarding how many hikes the Fed will deliver this year. Whereas just a few weeks ago markets had fully priced two more 25bps rate hikes by the Fed and also saw a 20% probability for a third one, now that pricing has slipped materially; only one 25bps rate hike is fully factored in, and the Fed funds futures imply an 85% likelihood for a second one. Thus, although the debate until lately was whether the Fed would deliver two or three additional hikes this year, now even the prospect of two more has come under some doubt. Correspondingly, the probability for a rate increase at the June meeting has slipped to 82%, from nearly 100% previously.

Turning to gauges of the labor market, initial jobless claims remained quite low for most of May, supporting the case for a strong NFP number. Something similar was signaled by the Markit preliminary Composite PMI, which showed that “a solid rate of employment growth was maintained across the private sector in May”. The ISM surveys – which markets typically pay more attention to – haven’t been released yet. Meanwhile, the private ADP employment report that is traditionally considered a tracker of the official NFP print also came in at a solid 178k, though it should be noted that the correlation between the two figures has not been that strong lately.

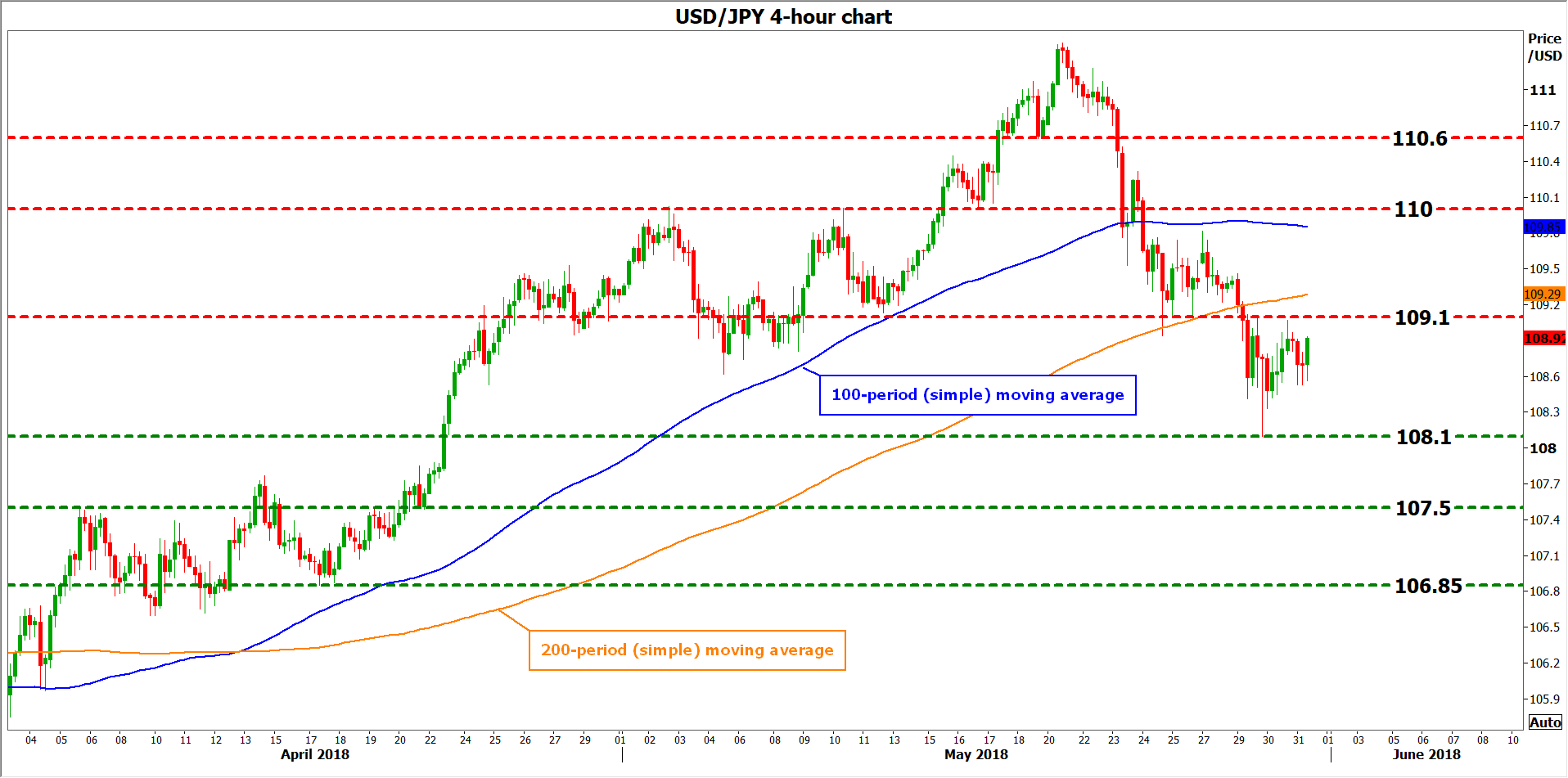

In case these data come in above expectations, particularly on the earnings front, then the dollar could extend its recent gains as investors become more confident in the Fed delivering at least two more rate increases this year. Looking at dollar/yen, immediate resistance to advances could come near 109.10, the low of May 11. An upside break of that zone could aim for the round figure of 110.00, marked by the highs of May 2 and 10. Even higher, attention would shift to the 110.60 line, defined by the low of May 18.

On the downside, and in case a disappointment in these figures casts further doubt on how many hikes the Fed will deliver, support to declines may come at 108.10, the trough of May 29. If the bears manage to break below it, focus would increasingly turn to the 107.50 barrier, identified by the peaks of April 5. Lower still, buy orders may be found around 106.85, the bottom of April 17.