Here are the latest developments in global markets:

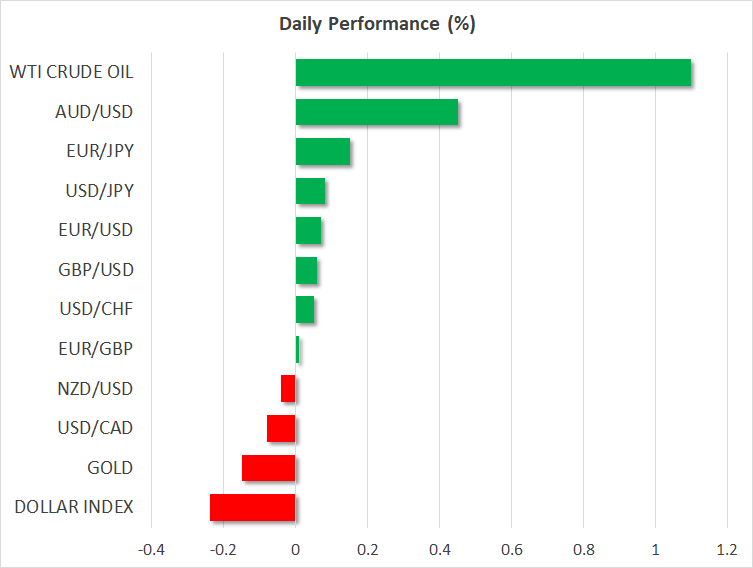

FOREX: The US dollar index is down by 0.24% on Tuesday, giving back some of the gains it posted in the previous session. The euro rebounded somewhat following news that the German political deadlock had been solved, while the aussie gained in the aftermath of the RBA’s policy meeting.

STOCKS :US markets managed to erase earlier losses and close higher on Monday, boosted by a rally in technology stocks. The tech-heavy Nasdaq Composite gained 0.76%, while the S&P 500 and the Dow Jones climbed by 0.31% and 0.15% respectively. The positive sentiment appears to have lingered, as futures tracking the Dow, S&P, and Nasdaq 100, all suggest a higher open today. In Asia, markets were mostly lower. In Japan, the Nikkei 225 and Topix fell by 0.12% and 0.15% correspondingly, while in Hong Kong, the Hang Seng dropped 1.53% on its first day back from holidays. In China, the CSI 300 rose, albeit only by 0.03%. Europe was more cheerful. Futures tracking all the major indices point to a notably higher open today, following news that the political crisis in Germany has been resolved.

COMMODITIES: Oil prices continued to ascend, with WTI crude rising 1.1% to reach a fresh three-and-a-half year high on Tuesday, propelled higher by headlines that oil exports from two of Libya’s largest ports were halted amid military tensions. Reports suggest that as much as 850,000 barrels per day may be removed from the market. Meanwhile, weekly API data (2030 GMT) might offer some short-term direction to oil prices. In precious metals, gold is down by 0.15%, currently trading near $1,244 per troy ounce. It touched a new low for the year at $1,238 earlier on Tuesday, before rebounding somewhat. The technical picture remains negative, though the area around $1,238 appears to be a strong support zone; it also halted the metal’s decline back in December.

Major movers: Euro steadies on German accord; aussie rebounds after RBA

The euro is a little higher on Tuesday, recovering some of its losses from the previous session, following positive headlines out of Germany. The political crisis that was seen as threatening the stability of Angela Merkel’s coalition government has reportedly passed, after she managed to strike a deal with the “rebels” in her cabinet on immigration.

In the UK, sterling failed to capitalize on news that the government has prepared a new plan for handling customs after Brexit; an issue that has been a thorn in negotiations so far. The proposal will be presented to UK ministers on Friday, and is expected to be followed by a White Paper outlining the UK’s preferred path. Judging by the subdued market reaction so far though, investors do not anticipate this to be the “smoking gun” that breaks the deadlock in the negotiations. With the political crisis in Germany now resolved, but Brexit uncertainties still riding high, the risks surrounding euro/sterling may be tilted to the upside over the coming days.

Overnight, the RBA kept its policy untouched and maintained a fairly neutral bias. It highlighted concerns around global trade, but also took note of the strength in the domestic economy. The key message was that while Australia is humming along nicely, many global uncertainties persist, and policy will stay unchanged for a while. Aussie/dollar is 0.45% higher today, but continues to trade close to 18-month lows. The pair will remain highly sensitive to trade issues; note the US and China will slap tariffs on each other on Friday, and further escalation should not be ruled out. Absent any improvement in trade tensions, the outlook for the aussie may remain negative.

The Chinese yuan continued to slide, touching an eleven-month low against the dollar. While the move appears market-driven, possibly on the back of trade worries, the fact that the Chinese authorities have not intervened to halt – or at least slow – the drop suggests they may be somewhat comfortable with a depreciating currency at this point.

Day ahead: Eurozone producer prices and retail sales due; US factory orders and UK construction PMI also out; Riksbank decides

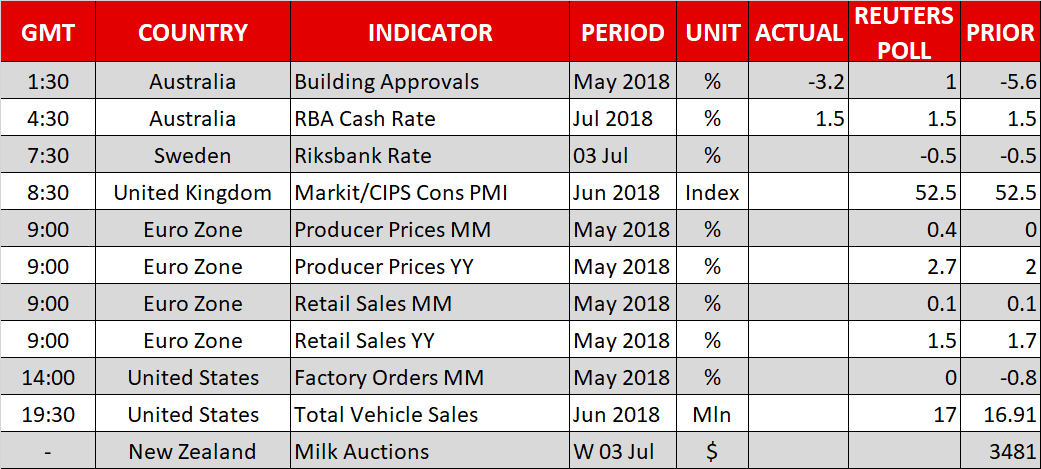

Tuesday’s calendar features a few releases of relative importance, including eurozone producer prices and retail sales, as well as factory orders out of the US.

At 0730 GMT, the Swedish central bank – the Riksbank – will be announcing its interest rate decision, with the monetary policy report being released at the same time. A press conference by the Bank’s governor will follow at 0900 GMT.

The UK will be seeing the release of construction PMI data for June at 0830 GMT. This comes one day ahead of the respective print for the all-important for the UK economy services sector.

Eurozone producer prices and retail sales for May are due at 0900 GMT. Producer prices are expected to accelerate on both a monthly and yearly basis. As regards retail sales, those are projected to grow by 0.1% m/m, the same as in April, while they’re anticipated to ease to 1.5% on an annual basis from 1.7% in the previously tracked month.

US factory orders are slated for release at 1400 GMT. No monthly growth in orders is expected during May, after April’s contraction by 0.8%. Meanwhile, data on total vehicle sales out of the world’s largest economy will be made public at 1930 GMT.

The outcome of the bi-weekly milk auction will be known later today, though there’s no specific time of release. Kiwi pairs will be generating attention as the data are made public; dairy products are New Zealand’s largest goods export earner, with higher prices seen as supporting the NZD.

Trade remains a dominant theme in markets only a few days before US tariffs on Chinese-imported goods become effective (July 6). In the meantime, volatility in the yuan is something that is being monitored by officials in the Chinese central bank (PBOC).

ECB Chief Economist Peter Praet will be giving a speech at 1400 GMT.

Technical Analysis: EURUSD neutral-to-bullish in the short-term

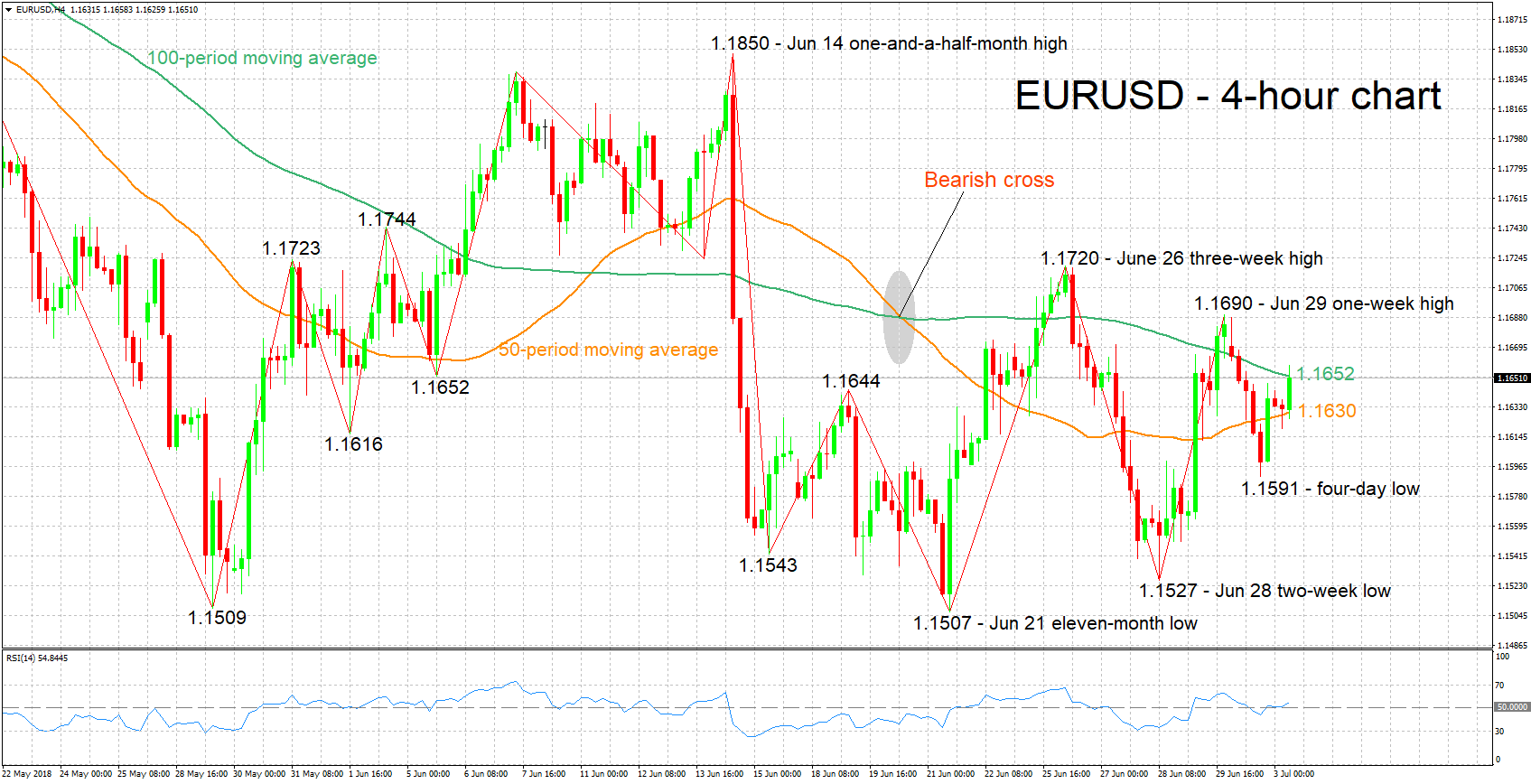

EURUSD has managed to climb after hitting a four-day low of 1.1591 on Monday and is currently challenging the current level of the 100-period moving average line (1.1652) on the 4-hour chart. The RSI has moved above the 50 neutral-perceived level and continues to rise. Notice though that the indicator is still close to neutral levels and does not maintain a steep positive slope, overall projecting a neutral-to-bullish picture in the short-term.

Upbeat data out of the eurozone are likely to boost the pair. Immediate resistance is taking place around the 100-period MA at 1.1652, with the attention falling to the one-week high of 1.1690 from late June in case of a break to the upside.

Disappointing figures on the other hand are expected to see EURUSD coming under selling pressure. Support could come around the 50-period MA at 1.1630 and then from the region around yesterday’s four-day low 0f 1.1591 (including the 1.16 handle).

{kind=link}