Here are the latest developments in global markets:

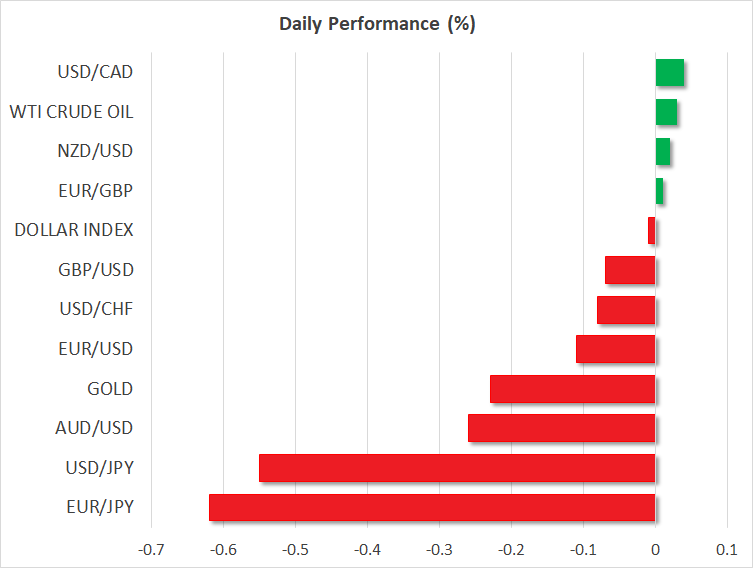

FOREX: The US dollar index is practically unchanged on Monday, after touching its highest level in more than a year on Friday. The haven-perceived yen is the strongest among its peers today, benefiting from concerns over the situation in Turkey and its potential repercussions. The euro and sterling, meanwhile, are both on the back foot. As for the Turkish lira, it touched a new all-time low of 7.21 per dollar earlier today.

STOCKS: US markets closed in the red on Friday, as fears that the crisis in Turkey could spill over into other economies led investors to decrease their exposure to equities. The Dow Jones (-0.77%), the S&P 500 (-0.71%), and the Nasdaq Composite (-0.67%) all came under pressure as market participants turned their sights to safer assets. The Dow, S&P, and Nasdaq 100 are all set to open notably lower today as well, futures suggest. Asia was a sea of red on Monday, with Japan’s Nikkei 225 (-1.98%) and Topix (-2.13%) suffering as a stronger yen cast a shadow on Japanese exporters. In Hong Kong, the Hang Seng dropped by 1.48% while in South Korea, the Kospi 200 fell 1.29%. Europe was a similar story, with all the major indices expected to open notably lower today, according to futures.

COMMODITIES: Oil prices were little changed on Monday, with WTI being marginally higher (+0.03%) but Brent being somewhat lower (-0.12%). Both benchmarks posted gains on Friday even despite a stronger US dollar, amid relief that crude oil will finally not be targeted in China’s retaliatory salvo of tariffs against the US. In precious metals, gold is down by 0.23% today at $1206 per troy ounce. This is a critical technical juncture for the yellow metal. A break below its 17-month lows of $1204 – and also beneath the psychological number of $1200 –, could signify that the negative trend is back in force. Conversely, an inability of the bears to pierce below the $1200 area could be a sign that the negative sentiment is losing steam.

Major movers: Yen, dollar advance amid Turkey jitters; euro and pound hammered

The situation in Turkey and the potential for spillover elsewhere remained the dominant theme in the FX market, with the yen advancing against all its major counterparts on Friday as investors rushed towards safety. The Japanese currency is higher across the board on Monday as well. The dollar benefited too, albeit to a lesser extent than the yen, with the US currency seemingly also attracting safe-haven flows on the rationale that the US economy is likely better prepared than most of its peers to weather a storm in the markets.

While the yen and dollar advanced, the euro and sterling retreated. The single currency was hit by contagion fears, with euro/dollar touching a fresh 13-month low of 1.1365 earlier today amid concerns that large European banks may be overly exposed to Turkey. From a market perspective, this is seen as yet another risk that may delay the ECB’s normalization efforts. Indeed, investors have pushed back the anticipated timing of the first 10bps ECB rate increase to December 2019, according to EONIA swaps.

The British pound was also hammered, posting a new one-year low against both the dollar and the yen, with investors remaining defensive amid a clouded UK political outlook and a cautious BoE. It’s going to be a big week for sterling, with several key UK data releases and the resumption of the Brexit talks likely to keep traders busy. While the currency could see a data-driven relief bounce should the figures be on the strong side, any such rebounds may remain relatively short-lived until some progress in the EU-UK negotiations is evident.

As for the main culprit, the Turkish lira, it continued to tumble into uncharted territories on Friday and extended its losses this week as well. Dollar/lira touched a new all-time high of 7.21 earlier today before retreating somewhat, with the pace of the currency’s freefall having accelerated significantly lately. The latest losses were fueled by a tweet from US President Trump on Friday that the US will double its steel tariffs on Turkey. On top, Turkish authorities have shown little willingness to arrest the lira’s collapse, with the central bank shying away from raising interest rates to slow capital outflows. At this point, though, it seems doubtful whether even a sizeable rate increase would be sufficient to halt the lira’s plunge, or whether it would only slow it temporarily.

Day ahead: US-Turkish political standoff under the spotlight; OPEC monthly report pending

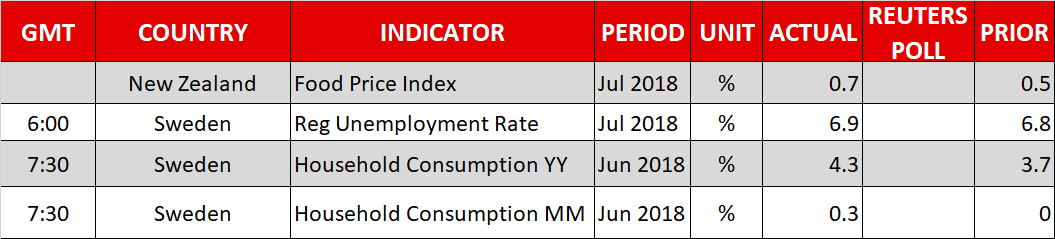

The economic calendar will be lacking key data releases on Monday, leaving political issues to potentially drive the FX and stock markets as the standoff between the US and Turkey as well as the US-Sino trade war continue to boil.

In Turkey, investors will be eagerly waiting for the Finance ministry to announce its action plans which aim to protect the economy from the lira’s plunge as the Turkish Treasury and Finance Minister, Berak Albayrat, promised on Sunday – the same day when Turkish President Tayyip Erdogan called the dispute with the US an economic war and turned down any agreement with the IMF. The euro came under pressure as Erdogan’s defensive stance escalated fears that the lira’s meltdown could leave European banks exposed to default loans from Turkish borrowers. Apart from the lira, other emergency currencies such as the South African rand and the Indian rupee felt the pain as well. Should Turkey give a relief to the markets today, the aforementioned currencies could rebound, pushing safe-haven assets such as the Japanese yen and the Swiss franc lower.

Any news on the trade front could also amplify volatility in the markets later in the day, after an exchange of additional tariff threats between the US and China last week raised speculation that the trade war is not near its end. However, with investors being significantly confident on the US economy after core CPI figures in the US picked up speed for the third consecutive month to reach 2.4% y/y, the highest level recorded since October 2008, the dollar could remain resilient in case tensions escalate even further. In other words, the greenback could face limited losses or even head higher, as it did in previous risk-off sessions.

Turning to oil markets, the OPEC is scheduled to release its monthly report today at a tentative time, giving a detailed analysis of factors affecting demand and supply. The report will also update OPEC’s outlook for crude oil developments in the coming year. Any bearish signals regarding the US-Iran sanction story and rising trade uncertainties could add further pressure to crude oil prices, and vice versa.

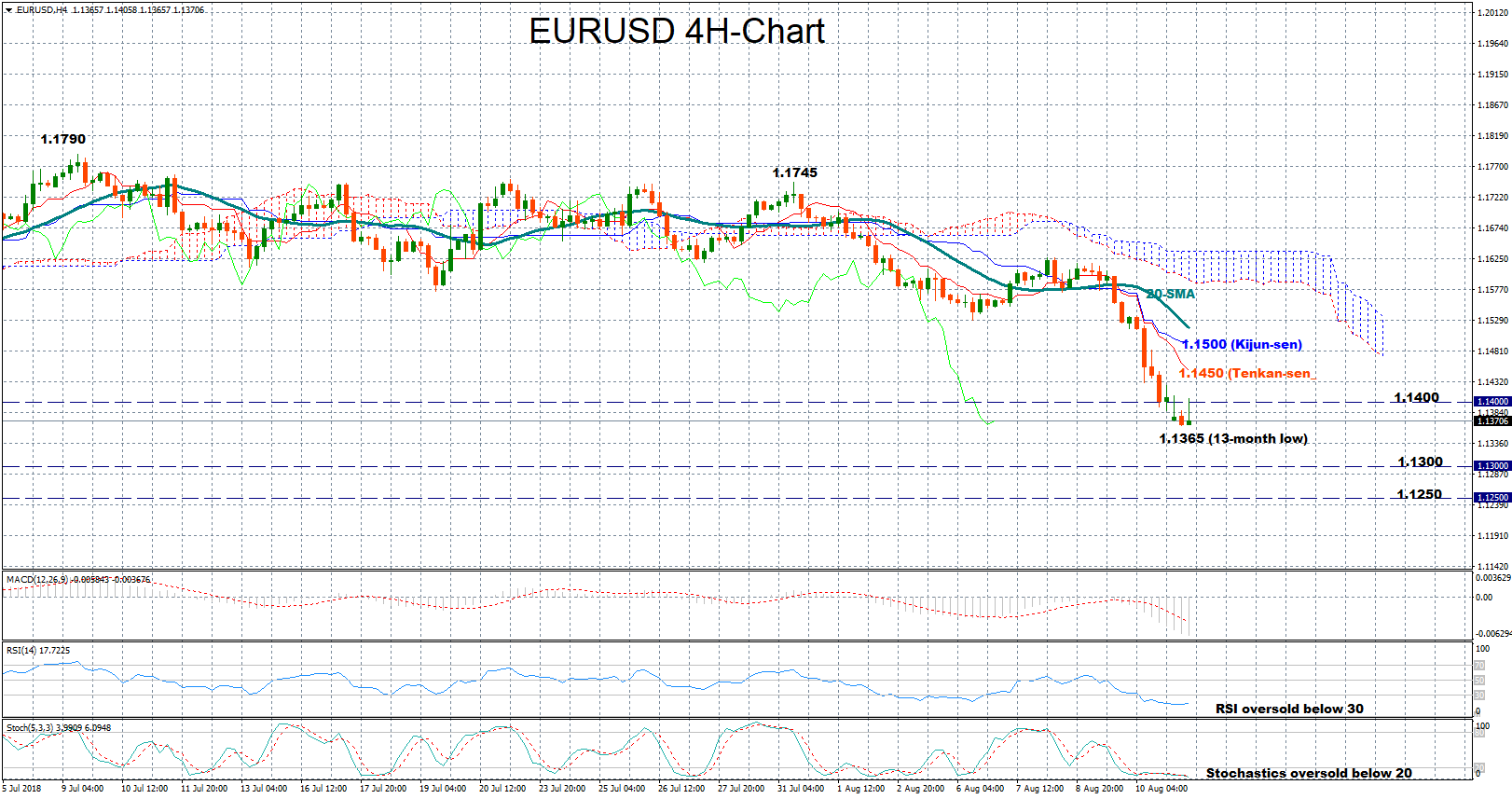

Technical analysis – EURUSD holds bearish and oversold below 1.1400

EURUSD turned increasingly bearish on Monday, extending losses below the 1.1400 round level to touch a 13-month low at 1.1364. While a rebound in the price is not unlikely given that the RSI and Stochastics continue to move in oversold territory for the second day in the four-hour chart, the MACD shows no sign of improvement, suggesting that bearish pressures could dominate. Besides, with prices well below the 20-period moving average and the Ichimoku cloud, the downtrend is expected to stay in place in the short-term.

Should the price stretch lower, the 1.1300 key level could be met first as the area around it was approached a number of times during 2016 and 2017. A close below that, may open the way for the 1.1250 mark.

Alternatively, a rebound could retest the 1.1400 level before resistance runs towards the area between 1.1450 and 1.1500, where the red Tenkan-sen and the blue-kijun sen lines are currently located.

{kind=link}