Here are the latest developments in global markets:

FOREX: The dollar index was down on Friday, albeit by less than 0.1%, giving back some of the gains it posted in the previous session. Elsewhere, the Japanese yen advanced across the board on Thursday, as trade concerns led investors to increase their exposure to the safe-haven currency. Meanwhile, the euro and the loonie retreated, weighed on by concerns surrounding Italy and disappointing Canadian data respectively.

STOCKS: US equities fell for the first time in five days as trade worries came back to the surface, with the S&P 500 (-0.44%) and the Nasdaq Composite (-0.26%) pulling back from their all-time highs. The Dow Jones underperformed its US peers, edging lower by 0.53%. The S&P, Dow, and Nasdaq 100 are all expected to open practically flat today, futures suggest. The negative sentiment spilled over into Asia on Friday. Japan’s Nikkei 225 was little changed (-0.02%), while the Topix was down by 0.22%. In Hong Kong, the Hang Seng dropped 1.11%. Meanwhile in Europe, futures tracking all the major benchmarks were pointing to a notably lower open today.

COMMODITIES: Oil prices were steady on Friday, holding onto gains from the previous session. The precious liquid is caught between two conflicting narratives, with supply outages in Venezuela acting as a floor below prices, but signs of escalating trade tensions between the US and China capping any material gains. WTI and Brent crude were trading at $70.26 and $77.72 per barrel respectively, practically flat on the day. In precious metals, gold was up by 0.33% at $1,205 per troy ounce.

Major movers: Dollar & yen bounce amid renewed trade concerns and EM angst

The dollar rebounded on Thursday, snapping a four-day losing streak as risk appetite turned sour again, amid fresh signs of escalation in the US-China trade standoff and renewed concerns around emerging market economies. The Japanese yen and the Swiss franc – both of which are considered haven currencies –, also came under buying interest as investors sought shelter from growing risks, with the yen advancing against all its major peers.

The catalyst for these moves were comments by President Trump that he plans to proceed with new tariffs on $200bn of Chinese goods next week, something China previously threatened it would retaliate to. Furthermore, he rejected an “olive branch” proposal from the EU for both sides to completely eliminate tariffs on imported cars, noting that “it’s not good enough”. Both developments probably poured some cold water on recent hopes that with the NAFTA renegotiations likely drawing to an end, trade frictions with other economies could subside soon as well.

Fresh troubles in emerging markets likely amplified the cautious sentiment. The Argentinian peso’s collapse accelerated yesterday, falling by nearly 12% against the dollar. The plunge came despite the nation’s central bank raising interest rates to a global high of 60% – from 45% previously – in an attempt to inspire confidence, which was seemingly viewed more as a “panic move” and hence backfired. The angst spilled into other emerging currencies, most notably the Turkish lira and South African rand, with the former approaching its all-time lows again.

The euro, meanwhile, retreated across the board. Not only has the single currency been highly sensitive to worrisome trade news in recent months, but yesterday, it likely felt additional pressure by a spike higher in Italian bond yields – similar to what occurred in late May. The Italian budget, which is due at the end of September, is surrounded by concerns that the government and the EU may cross swords over fiscal rules. On this front, and in the more immediate term, it will be interesting to see whether Fitch downgrades Italy’s sovereign credit rating today. If so, that could add further pressure on the euro.

In Canada, the loonie dropped after GDP data for Q2 came a touch softer than anticipated, with growth clocking in at an annualized rate of 2.9% instead of the expected 3.0%. Market-implied odds for a BoC rate hike next week dropped to a mere 20% in the aftermath. On the NAFTA front, today is the unofficial deadline for Canada and the US to reach a deal. Hence, the loonie’s intraday direction may be decided by whether or not an accord is finalized.

Day ahead: Eurozone flash inflation due; Brexit & trade developments eyed

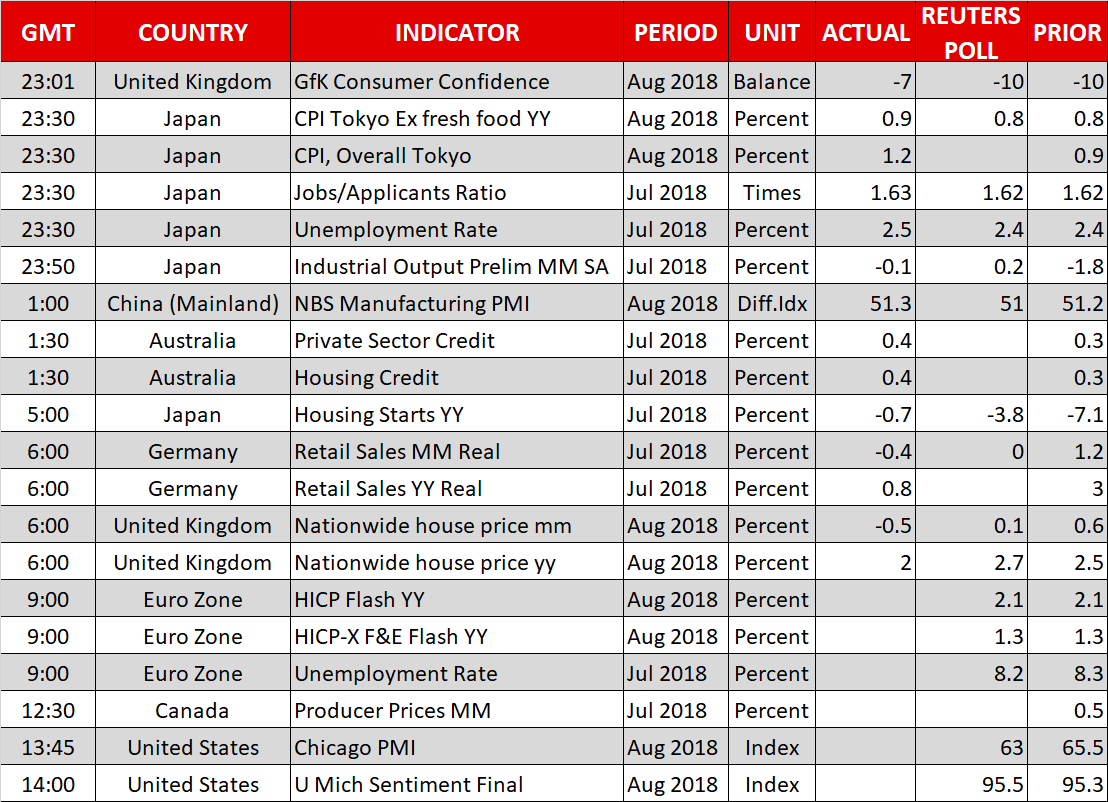

Eurozone flash inflation figures for August are the highlight out of Friday’s calendar. Beyond releases, other events will be attracting attention, including Brexit and trade.

The preliminary reading on August eurozone inflation is expected to show the Harmonised Index of Consumer Prices (HICP) growing by 2.1% y/y, the same as in July. This is above the ECB’s annual target for inflation of “below but close to 2%”. Still, the central bank’s policymakers may downplay the significance of the above-target rise when they next meet around mid-September, given that that is likely to be largely owed to elevated energy prices. Supporting this, the core measure of inflationary pressures that excludes food and energy is predicted to expand by 1.3% y/y, again matching July’s pace of growth. In the meantime, the eurozone’s unemployment rate due at the same time is projected to fall to 8.2% in July – its lowest in around a decade –, from June’s 8.3%.

Out of the US, the Chicago PMI and the University of Michigan’s final survey on August consumer sentiment are slated for release at 1345 GMT and 1400 GMT correspondingly. The former is forecast to ease a bit after touching its highest since January in July, while the U of M’s survey is anticipated to revise the final print of the relevant index gauging consumer morale slightly upwards to 95.5 from 95.3 – this would still be below July’s 97.1.

Canadian producer prices are due at 1230 GMT. However, of more significance for the loonie are ongoing efforts for a new North American trade deal; the parties involved indicated that they may come to an agreement as soon as later on Friday.

Remaining on trade, President Trump, in a Bloomberg interview yesterday, showed willingness to impose tariffs on an additional $200 billion in Chinese imports as soon as next week. The trade war saga thus appears to have much more room to run. Moreover, the US president rejected the EU’s offer for zero tariffs on autos, calling the block “almost as bad as China” on trade. He also threatened to withdraw from the WTO, unless the organization “shapes up”.

On the Brexit front, negotiations will be taking place today and there are growing expectations for a deal after Barnier’s recent comments.

Meanwhile, Italian budget angst remains in the background and could well weigh on the euro should debt sustainability concerns rise.

In EM space, currencies such as the Argentine peso continue to retreat sharply – the Turkish lira is higher today versus the greenback though overall it’s been losing considerable ground as well. The trajectory of these currencies will be monitored, as well as any spillover effects to other markets.

A public appearance by ECB Vice President Luis de Guindos is on the agenda at 1700 GMT.

In energy markets, the weekly Baker Hughes report on active US oil rigs is due at 1700 GMT.

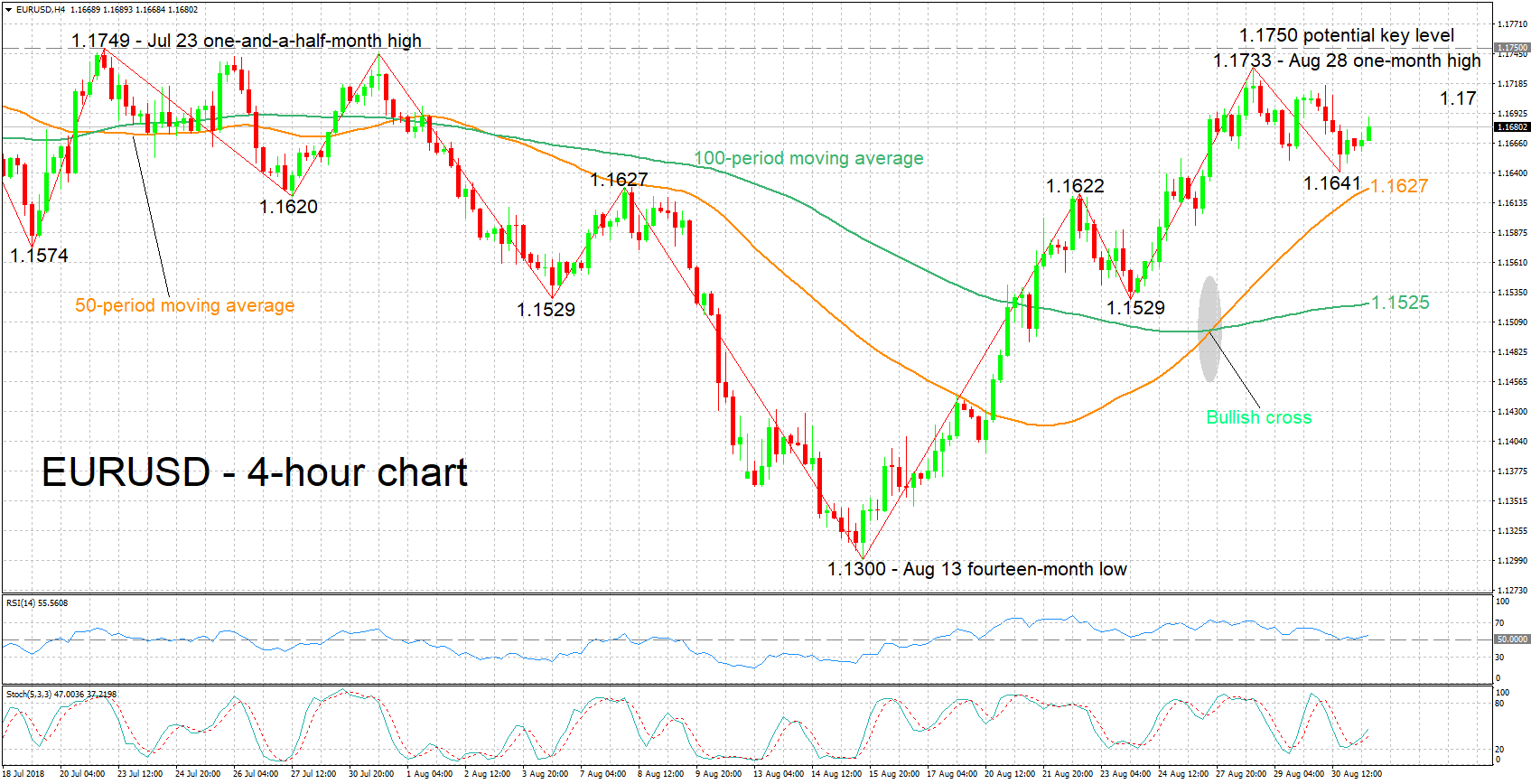

Technical Analysis: EURUSD looking mostly neutral in near-term; stochastics give bullish signal in very short-term

EURUSD is trading roughly 50 pips below the one-month high of 1.1733 hit on Tuesday. The RSI is in large part moving sideways, projecting a mostly neutral short-term picture. The stochastics however, are giving a bullish signal in the very short-term, as the %K line has moved above the slow %D one.

Stronger-than-anticipated eurozone inflation data later today may boost the pair. Given a move above the 1.17 round figure, resistance could come around the one-month peak of 1.1733 recorded earlier in the week. Notice that 1.1750 lies not far above; the zone around it encapsulates numerous tops from the recent past.

Conversely, weak eurozone numbers are likely to exert selling pressure on EURUSD. Support to declines may come around the current level of the 50-period moving average line at 1.1627; the area around this includes numerous tops and bottoms, while the 1.16 handle lies not far below. Steeper losses would bring the region around the 100-period MA at 1.1525 into scope.

Trade developments can also move the pair.

{kind=link}