Here are the latest developments in global markets:

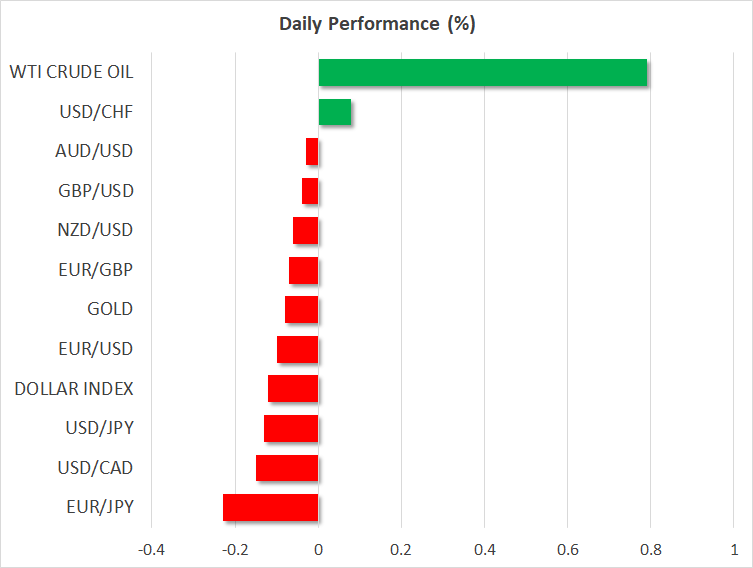

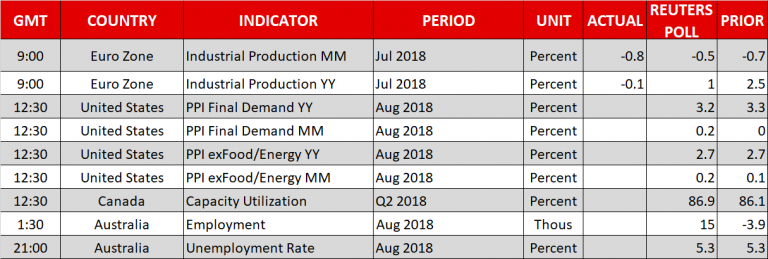

FOREX: During the early European session, the dollar was slightly weaker against the yen at 111.47 (-0.13%), while the dollar index also stood marginally lower at 95.16 (-0.09%) as investors were cautious about whether Washington will proceed with further import tariffs against China, potentially forcing Beijing to take countermeasures as well. In emerging markets, trade fears spurred a further sell-off, with the offshore Chinese yuan dropping to 2 ½ -week lows and the Indian rupee hitting fresh record troughs versus the greenback. The MSCI emerging currency index – which tracks the performance of 25 EM currencies relative to the dollar – fell to 16-month lows too. Dollar/loonie was close to 1-week lows after the Canadian Foreign Affairs Minister Chrystia Freeland said yesterday that talks with the US trade representative Robert Lighthizer, were productive and that both sides continued to have a goodwill for NAFTA progress. In the Eurozone, industrial production data for the month of July missed expectations, with the yearly gauge turning negative for the first time in two years. Specifically, industrial output declined by 0.1% compared to a plus 1.0% expected and a positive 2.5% growth seen in June. Yet, euro/dollar didn’t react much on the data, remaining around 1.1596 (-0.09%). In other news, sources familiar with ECB thinking, which starts its two-day monetary policy meeting today, said that the central bank is set to lower its growth projections. Meanwhile, pound/dollar was consolidating yesterday’s slight gains around 1.3028 (-0.04%) as the latest wave of Brexit headlines brought some confusion to investors. On the one hand, optimism for a Brexit deal before November – as was hinted by the European Brexit negotiator – became a tailwind to the pound with the President of the European Commision Jean-Claude Junker saying today that the UK Prime Minister’s proposals for a close partnership are welcome. Still, a BBC report stating that a group of Brexiteer lawmakers in the British Parliament gathered to discuss how to challenge the PM’s leadership, likely reminded markets that Theresa May has still to convince opposing members of her party about her Chequers Brexit plan. Pound/dollar changed hands lower at 1.3018 (-0.12%), while pound/yen eased to 145.14 (-0.23%). In antipodean currencies,aussie/dollar and kiwi/dollar were flat near 2 ½-year lows at 0.7122 and 0.6524 respectively, feeling the pressure from ongoing trade tensions.

STOCKS: Following a negative session in Asia, stocks opened higher in Europe on Wednesday led by gains mainly in the energy sector. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 rose by 0.46% and 0.41% respectively at 0830 GMT. The German DAX climbed 0.48% despite considerable losses in utilities (-2.75%), while financials held in positive territory, supported by news that the two German largest banks, Commerzbank and Deutsche Bank are considering a merger. Yet stocks of the aforementioned banks were under pressure at the time of writing. The French CAC 40 was up by 0.85%, the Italian FTSE MIB climbed by 0.40%, while the British FTSE 100 inched up by 0.14%. Futures tracking US indices suggest the S&P 500, Dow Jones, and Nasdaq 100 are poised for a modestly positive open today.

COMMODITIES: A larger drawdown in US oil stockpiles in the week ending September 7 according to the American Petroleum Institute and concerns that renewed US sanctions on Iran in November may pressure the availability of oil aided crude prices to extend gains today. Comments by the Russian Energy Minister on Wednesday expressing that the global oil market remains “fragile” on the back of geopolitics and production shortages in several regions such as Venezuela and Mexico, also gave a helping hand to crude prices. WTI crude and Brent were last seen at $69.75 (+0.75%) and at $79.26 (+0.25%) correspondingly. Gas prices were also rising as hurricane Florence – a category 4 storm – is expected to hit South Carolina, North Carolina, and Virginia later this week. In precious metals, gold weakened to $1,194.6/ounce (-0.26%).

Day Ahead: US delivers PPI; Australian employment report pending

Next on the day’s agenda, at 1230 GMT the US Bureau of Labor Statistics will release figures on producer prices, with analysts projecting the PPI to have edged down by 0.1 percentage points to 3.2% y/y in August. Month-on-month, though, the index is said to tick higher to 0.2% compared to 0.0% in July. The core measure of PPI that excludes volatile food and energy items is predicted to jump by 2.7% y/y, the same pace as before. Tomorrow, consumer prices are coming out of the US as well, so today’s releases may give an early indication of the inflation trend.

In energy markets, investors will look to the EIA report on US crude oil inventories at 1430 GMT. According to forecasts, crude inventories have dropped by 0.805 million barrels in the week ending September 7 after falling by 4.302mn barrels in the preceding week. On the other hand, gasoline inventories and distillate stocks are anticipated to increase, though not by much.

Investors could remain cautious during the day as the US may announce tariffs on $200 billion Chinese goods at any moment. Also, during next week, China will request the World Trade Organization (WTO) permission to impose sanctions on the US, due to the nation’s non-compliance with a ruling over US dumping duties.

Any news regarding NAFTA talks could add further volatility to the loonie, while the pound is expected to stay vulnerable to any potential Brexit headlines later this week.

In equities, European authorities are on track to impose fines to Google’s parent Alphabet, Facebook and Twitter in the accusation of a breach of antitrust or consumer-protection lows. Apple is expected to unveil a new version of the iPhone X as well as other products today.

In terms of public appearances, External Member of the Prudential Regulation Committee of the Bank of England, Jill May, and London School of Economics Professor Julia Black will have a pre-appointment hearing at 1315 GMT. Later, at 1340 GMT and at 1645 GMT, Federal Reserve Bank of St. Louis President Bullard and Federal Reserve Board Governor Lael Brainard respectively will speak on the US economy and monetary policy. Also, the Fed’s Beige Book of economic condition is due at 1800 GMT.

Overnight, the Australian unemployment rate is said to remain unchanged at 5.3%, the lowest jobless rate since November 2012, while the economy is expected to have added 18,400 jobs in August compared to a decrease of 3,900 in the preceding month.

{kind=link}