Here are the latest developments in global markets:

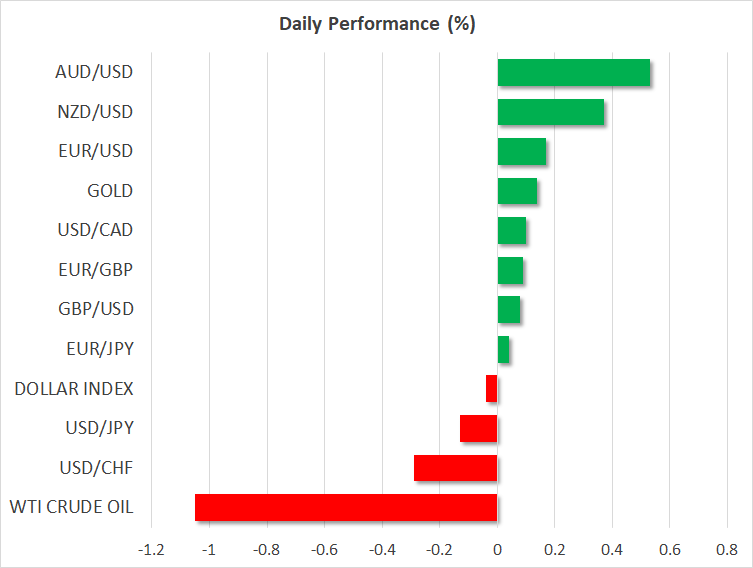

- FOREX: The US dollar ran to a new 1-week high against the Japanese yen earlier on Thursday after FOMC minutes from the September 24-25 policy meeting affirmed the prospect of additional rate hikes until the end of 2019. However, the pair eased by 0.18% soon after to trade at 112.47. The US dollar index reversed lower as well, last seen at 95.51 (-0.07%). British retail sales fell by 0.8% in September, posting a larger decline than the 0.4% drop forecasted. In August the measure increased by 0.3%. On a yearly basis, retail sales rose 3.0% from 3.3% in the preceding month, missing expectations for a 3.6% growth. The data however had little impact on the pound, with pound/dollar trading fractionally higher at 1.3125 (+0.10%) and pound/yen slighlty lower at 147.60 (-0.06%). It is worth mentioning, that sterling closed lower on Wednesday as the first day of the EU summit failed to bring a breakthrough on EU-UK divorce terms. Euro/dollar moved higher by 0.20%, jumping above 1.1500, while euro/yen gained by 0.08%. In the antipodean sphere, aussie/dollar edged higher by 0.52% as Australia’s unemployment rate unexpectedly dropped to 5% overnight, while kiwi/dollar advanced by 0.35%. Dollar/loonie climbed by 0.12% to 1.3032. The chinese offshore yuan was down by 0.20% at two-month lows ahead of the Chinese third quarter growth figures due on Friday and after the US Treasury avoided to call China a currency manipulator at its twice-yearly currency report, a move that could keep tensions from escalating further.

- STOCKS: European stock markets were mixed on Thursday at 1110 GMT. The pan-European STOXX 600 pared declines on the back of positive earnings, adding 0.18% to its performance, while the blue-chip Euro STOXX 50 was steady. The German DAX 30 was up by 0.14%, the French CAC 40 rose by 0.31%, while the Italian FTSE MIB slipped by 0.26%. The UK’s FTSE 100 pulled back by 0.20%. The worst performer today was the Spanish IBEX 35 sliding by 0.82% as financials dived (-2.89%) after the Supreme court charged Spanish banks with mortage taxes. In the US, futures tracking the S&P 500, Dow Jones, and Nasdaq 100 are pointing to a lower open today.

- COMMODITIES: Oil prices tumbled today as the EIA weekly report indicated a build up in US stockpiles for the fourth consecutive week, while a potential slowdown in the Chinese economy was also a concern. WTI crude plummeted by 1.12% to $68.98/barrel, near 1-month lows, while London-based Brent plunged by 1.26% to $79.04. In precious metals, gold traded marginally higher by 0.10% at $1,223.5/ounce.

Day Ahead: All eyes on Chinese GDP growth; Philly Fed Business Index & Japanese inflation also in focus

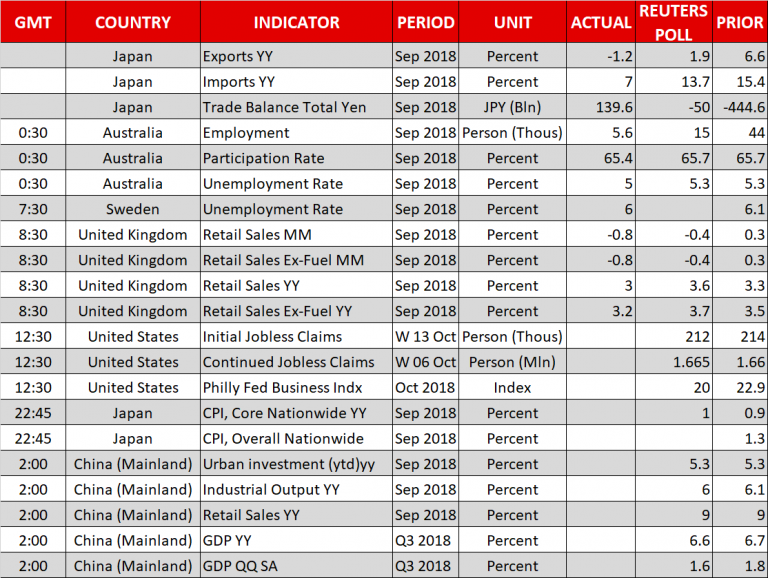

At 1230 GMT, Federal Reserve of Philadelphia is scheduled to publish its Business index for the month of October and the dollar could take the opportunity to make additional gains in case the numbers prove better than expected. Such a development would be another confirmation sign that the Fed will likely continue to raise rates in coming years or even adopt a stricter stance by driving rates above neutral levels as FOMC meeting minutes indicated. Looking at forecasts, the index is said to soften from 22.9 to 20.

At the same time, the US Department of Labor will be delivering initial jobless claims for the week ending October 13.

Chinese GDP growth figures, however, will be the most awaited release in coming sessions as projections suggest that the world’s second biggest economy expanded by 6.6% y/y in the third quarter, at the slowest pace since financial crisis. While this still above the government’s 6.5% growth target and marginally below the previous mark of 6.7%, investors could speculate that rising US trade protectionism against China has already started to bite at a time when the Chinese government makes efforts to put breaks to its mounting debt growth. Pessimism among manufacturers might have led industrial production lower as well, as analysts believe that factory output increased by 6.0% y/y in September compared to 6.1% in August, while in the January-September period,spending on infrastructure is said to have remained at a record low of 5.3% y/y. Retail sales delivered along the above data are also said to have stuck around multi-year lows, rising by 9.0% in September as in August. The data are due to hit markets at 0200 GMT on Friday.

Chinese stocks could rally in the wake of upbeat GDP growth figures and the Chinese yuan could recoup earlier losses against the greenback. The Australian currency is highly expected to move to the upside as well given that China is Australia’s major export partner.

Meanwhile in Japan, the Japanese core CPI is expected to inch up from 0.9% to 1.0% in September. Yet as the gauge shows no sustained moves towards the Bank of Japan’s 2.0% inflation target, the central bank is not likely to abandon its accommodative policy. The yen though could find some support if the numbers surprise to the upside.

In Europe, EU leaders will be discussing Brexit in the last day of the summit but hopes for an exit deal are very low, with the EU negotiator saying yesterday that more time is needed to deliver an orderly Brexit. The UK Prime Minister appeared positive to extend the transition period, though Barnier claimed that this would be acceptable if the British Prime Minister allowed a two-tier backstop in the Irish border. That is to maintain an open border between Northern Ireland and the Republic of Ireland, while applying alternative measures to a British-wide custom union. Besides Brexit, Italy’s budget plan is another headache for traders as recent comments from EU officials including the President of the European Commission, Jean-Claude Junker, were pointing that things could worsen before getting better.

In equity markets, the earnings season continues, with the American Express and Paypal Holdings delivering results for the third quarter after US markets close.

As for public speeches scheduled for today, ECB Executive Board Member Benoit Coeure and ECB President Mario Draghi will be participating in the Euro Summit. In the US Federal Reserve Bank of St. Louis President James Bullard will be giving a presentation on the U.S. economy and monetary policy before the Economic Club of Memphis at 1315 GMT. In New York, Fed Vice Chairman for Supervision Randal Quarles will be commenting before an Economic Club of New York luncheon at 1415 GMT.

{kind=link}