After a turbulent week for global stocks, attention should shift back to currency markets over the next seven days as a barrage of important economic data are on the agenda, along with more central bank meetings. The latest nonfarm payrolls report from the US and the first print of third quarter GDP growth for the Eurozone will be the biggest attractions. Other highly anticipated releases will include inflation numbers from Australia, the Eurozone and the United States, the Canadian employment report and UK and Chinese manufacturing PMIs. It’s not going to be quiet in the central bank world either as the Bank of Japan and Bank of England hold scheduled policy meetings.

Aussie in the spotlight as busy week ahead for Australian data

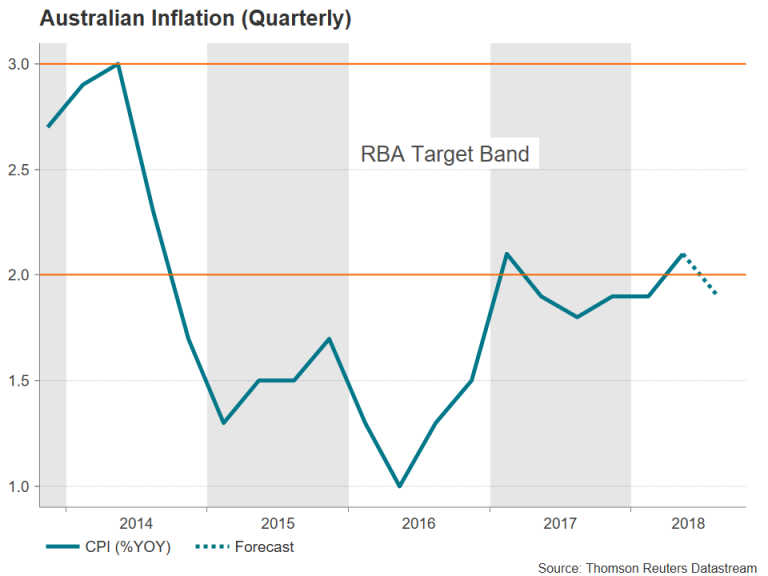

The Australian dollar was relatively resilient versus its US counterpart for much of the week despite the strong risk averse environment before finally giving way on Friday to fall to a new 32½-month low versus the greenback. The coming week could be more volatile for the aussie, however, with several key releases lined up. Starting first with September building approvals (a closely-watched barometer for construction activity) on Tuesday, to be followed by private sector lending figures and third quarter inflation figures on Wednesday. The annual rate of CPI is forecast to have moderated to 1.9% in the third quarter, to below the RBA’s lower target band, from 2.1% previously. An even weaker reading could further weigh on the aussie. On Thursday, the AIG manufacturing index for October and the September trade balance are due ahead of the latest retail sales numbers on Friday. Retail sales are expected to have maintained steady growth of 0.3% month-on-month in September.

Another focal point for aussie traders will be PMI data out of China. The official manufacturing and non-manufacturing PMIs are out on Wednesday, with the private Caixin manufacturing PMI coming up on Thursday. Both gauges of manufacturing activity are forecast to inch lower by 0.1 points in October.

Loonie looks to Canadian employment report to extend gains

The Canadian dollar got a major lift from a Bank of Canada rate hike this week, which was accompanied by a more hawkish tone. While weaker oil prices are capping the loonie’s gains, next week’s data may provide the extra boost needed for the currency to rise beyond this week’s one-week high of C$1.2965 per US dollar. First up are the monthly GDP estimates for August on Wednesday, together with September producer prices. On Friday, attention will turn to the October jobs report. Last month’s strong headline figure was misleading as all the gains were in part-time jobs, with full-time jobs declining in September. A rebound in new full-time positions in October would strengthen expectations that the BoC could soon be raising rates again. Also to watch on Friday are trade figures for September.

No surprises anticipated from Bank of Japan meeting

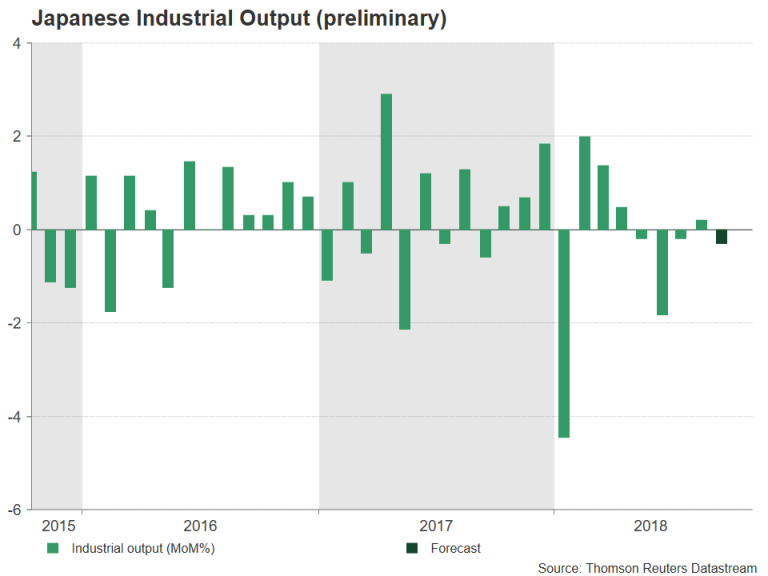

The Bank of Japan’s policy meeting on Wednesday will be the highlight of the Japanese calendar but before then, some economic releases will come into focus. Retail sales for September are due on Monday with the unemployment rate for the same month out on Tuesday. The preliminary reading on industrial output in September will follow on Wednesday. After eking out growth of just 0.2% in August, Japanese industrial production is forecast to have shrunk again in September, falling by 0.3% m/m.

Moving to Wednesday, the BoJ is widely expected to stand pat in October but its quarterly outlook report, which it will publish alongside its policy statement, will be analysed for any changes to its inflation and growth forecasts. The yen could weaken if the Bank lowers its inflation forecasts as this would signal continued quantitative easing and lower rates for longer.

Bank of England’s ‘Super Thursday’ unlikely to halt pound’s slide

The Bank of England will announce its latest monetary policy decision on Thursday and like the Bank of Japan, the UK’s central bank will also publish quarterly forecasts. With Brexit talks dragging on and the dimming outlook for world growth, the Bank could slightly nudge down its projections for GDP growth, and possibly inflation too. However, it’s less probable that the BoE will modify its guidance of 1-2 rate increases per year over the next few years. The pound could firm slightly if Governor Mark Carney stresses in his press conference that the risks to inflation remain to the upside. But any signs of increased caution over the outlook could pull sterling below this week’s 7-week trough below $1.28.

It will be somewhat quieter on the data front for pound traders, with the main releases being the manufacturing and construction PMIs on Thursday and Friday, respectively.

First glimpse at Eurozone Q3 growth

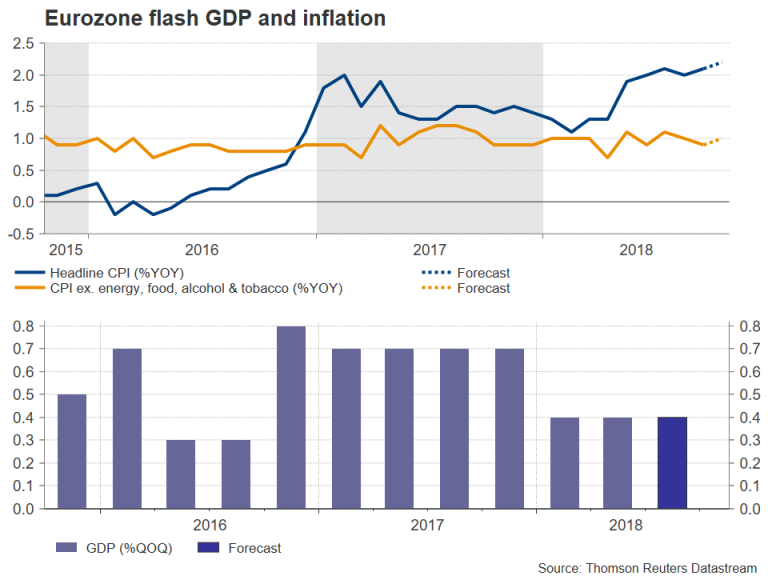

GDP numbers out of the Eurozone on Tuesday – the initial reading for the third quarter – will be eagerly awaited as all evidence points to a further slowdown in Eurozone growth in the second half of the year rather than the expected pick-up. Gross domestic product in the euro area is predicted to have expanded by 0.4% quarter-on-quarter in the three months to September, unchanged from the second quarter. Also out on Tuesday is the economic sentiment indicator from the European Commission for October. On Wednesday, the flash estimate of inflation in October will be monitored for any improvement in underlying inflation, which unlike headline inflation, has failed to move higher during 2018. The headline rate of CPI is expected to edge up to 2.2% year-on-year in October, while the figure that strips out all volatile items is expected at 1.0% versus 0.9% in the prior month.

The euro could come under additional selling pressure should the GDP and CPI numbers disappoint as it would raise the heat on the European Central Bank to slow down its policy normalization plans.

PCE inflation and wage growth to be main focus for US dollar

Despite the panic selling in equities markets, partly driven by concerns of a slowdown in US and global growth, US fundamentals so far continue to point to a solid economy. Investors could get a reminder of this from next week’s data, which will include the personal income and outlays report, productivity growth and the all-important nonfarm payrolls report.

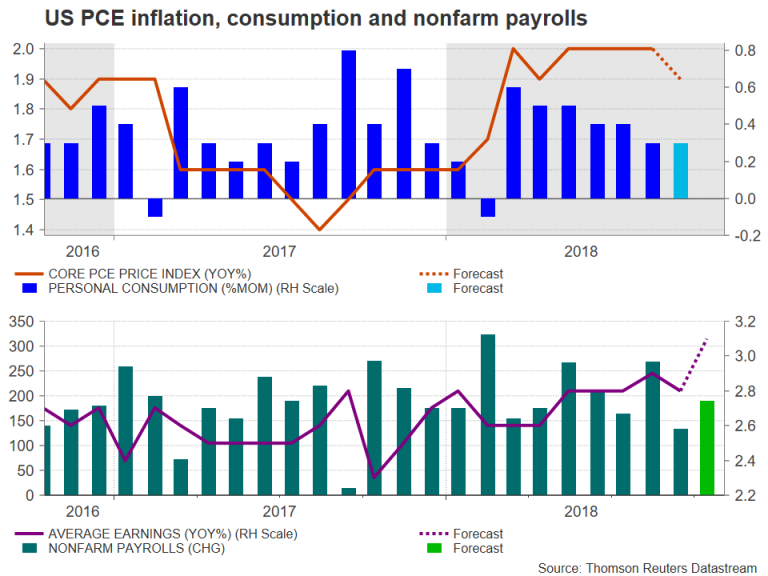

The personal income and spending numbers will start the week on Monday. Personal income growth is expected to have quickened slightly from 0.3% to 0.4% m/m in September, while personal consumption is forecast to have expanded by 0.3%, unchanged from the prior month. A key part of the personal income report is the personal consumption expenditures (PCE) price index, which the Fed looks at most closely when setting monetary policy. The core PCE price index is forecast to have dipped slightly to 1.9% y/y in September from 2%, suggesting inflationary pressures, although clearly present, remain under control.

On Tuesday, the Conference Board will publish its consumer confidence gauge for October, with the index expected to ease from 18-year highs. Other US surveys to keep an eye on next week are the Chicago PMI on Wednesday and the ISM manufacturing PMI on Thursday. Also due on Thursday are the preliminary prints on third quarter labour costs and productivity. Higher productivity growth is seen as key in boosting wages, though this doesn’t appear to have taken place yet as productivity growth likely slowed from 2.9% to 2.0% during the third quarter.

More data on wages will follow on Friday from the October jobs report. As investors increasingly question the Fed’s tightening policy, the latest assessment on the US labour market is unlikely to give the US central bank cause for a pause in hiking interest rates. Nonfarm payrolls are projected to have risen by 190k in October, improving on September’s 134k, which was negatively impacted by Hurricane Florence. The jobless rate is anticipated to remain at 3.7% in October, but average hourly earnings growth likely accelerated to above 3%, rising to a more than 9-year high of 3.1% y/y according to consensus forecasts. Friday’s other noteworthy releases from the US are September trade figures and factory orders.

With volatility on Wall Street affecting the dollar’s moves in the near term, the upcoming data may not stir much market reaction if they fall mostly in line with expectations and only big surprises in the numbers – particularly in core PCE inflation and wage growth – are likely to trigger large swings.

{kind=link}